In early 2010, economists had been delivered a twin bill of economic accounts that seemed to confirm recovery. GDP for the fourth quarter of 2009 had been initially estimated at close to 6% and employment appeared to finally be bottoming out. The pace of GDP expansion even led to talk about that infamous V-shaped recovery of the plucking model. It did not matter that most of the “growth” had been due to inventories shrinking at the slowest pace of the contraction, all that was important was the number itself.

It did not last long, however, as both employment and GDP forecasts have been, shall we say, decimated. It took only a few months for such optimism to be drowned in the monetary brilliance of QE 2; which only led to the same process playing out the following year. Indeed, this now-annual ritual recurs in the mainstream as each disappointing calendar turns and the next has barely been unfurled. Each and every year begins with “this will finally be the year”, where the recovery at long last shows up and the corner is decisively turned.

Going back two years to early 2012, this annual ritual reminded me very much of Alexander Pope’s 1733 Essay on Man. Most people have a passing familiarity with its most famous phrase, “Hope springs eternal in the human breast.” The rest of the work was really a critique on the growing hubris of “science” to not only explain everything, but introduce a degree of control. As Pope’s satire makes clear, any assumed control is an illusion.

As we enter 2014, hope will spring eternal in the “science” of economics. The projections are already laid out, robust and convincing – just as they have been every year since the inaugural over-optimism of 2010. The problem, as I see it, is that 2014 bears into far more headwind than any so far.

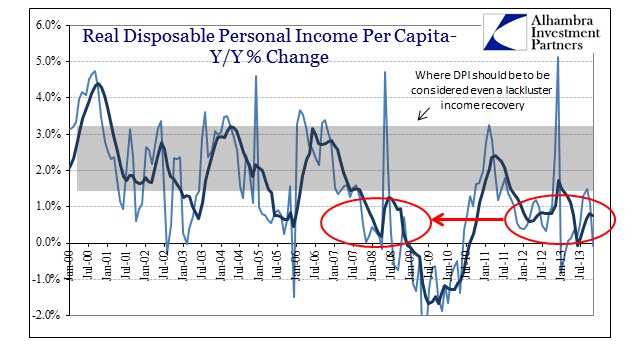

• The pace of income growth has been the worst of the “recovery” period. If there are jobs being created, and that is no sure thing given the persistence of statistical anomalies, it is not translating into income, earned or otherwise.

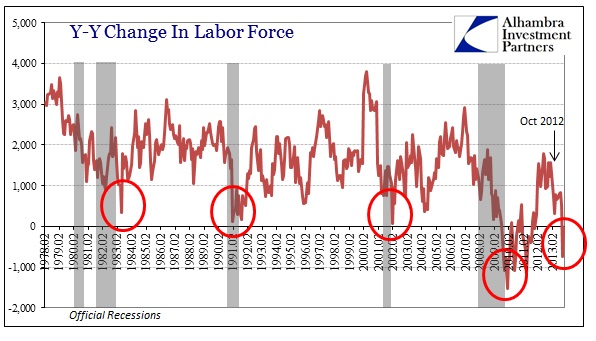

• The labor force is actively shrinking, as we have seen again measured Y/Y contraction in October and November. That typically indicates that workers have given up looking for work at precisely the time incomes are already substandard.

• As much as those actually and officially included in the labor force have grown wary, those not in the labor force are about to swell. Emergency unemployment runs out tomorrow, and about 1.4 million people are going to be left with no income of any kind. That is a triple blow to the vast majority of consumer spending power.

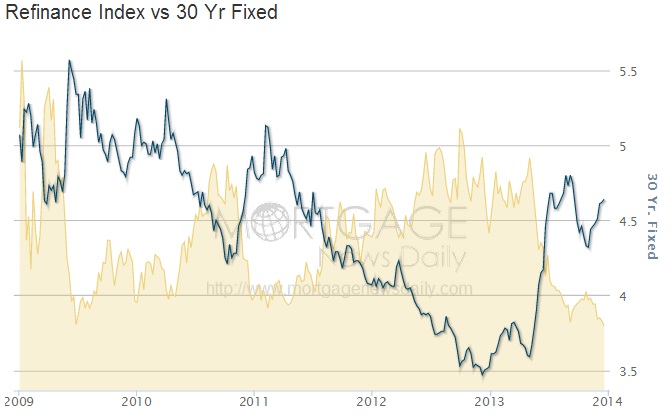

• The trickle of monetary dosage through mortgage refinancing appears to have conclusively ended. While it may not have had the massive effect intended by the FOMC, there was some “relief” provided by the opportunity to refinance, and some equity in homes available to be liquefied. Whatever minor tailwind that provided has been taper terminated; as the 70%+ collapse in refis demonstrates.

• Parallel to the collapse in refis, mortgage applications for purchases are decisively moving lower. Total purchase activity is down about 15% from 2012. And with mortgage rates again rising, it is more than reasonable to expect further erosion. As the National Association of Realtors data showed, home sales fell 4.3% in November from October, meaning the first Y/Y decline (-1.2%) since the mini-bubble began (29 months).

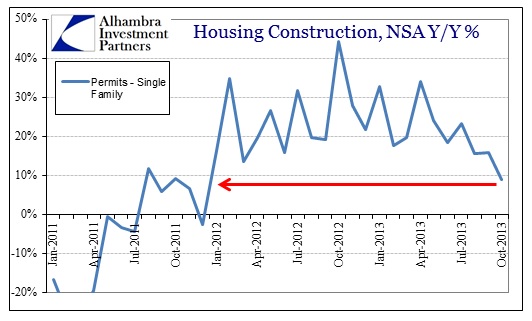

The effect has started to run through home construction, another of the expected tailwinds in 2014. If this continues, it may stretch into home prices and the nefarious “wealth effect.”

• Just in time for the mortgage market to deteriorate, the FOMC again showed how much they desire to command rather than listen. The December taper was supposed to be nothing, a non-event since forward guidance is “all that matters.” Funding markets have reacted as they did in the summer, by tightening anyway. That has led to a small but still-growing backup in interest rates as the 10-year peaked above 3% again. Tightening dollars and higher interest rates would certainly be classified as an “unexpected” headwind.

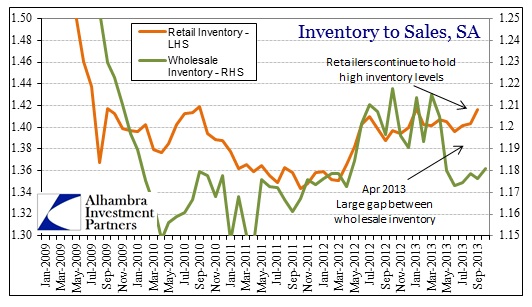

• In the goods economy, against a far less stable backdrop, retailers have accumulated far more inventory than at any point since 2009. Sales have not materialized on any level that would justify such optimism, only that last year’s hope was particularly addictive. The hangover now has a lot of negative potential.

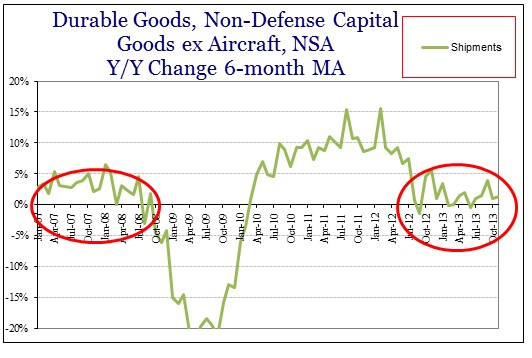

• Business “investment” has been about as tepid as actual retail sales. Like the overall economy, economists yearly predict an investment renaissance as business dishoard their purported massive cash holdings. With overall domestic revenue running at worse than 2008 levels, there is no explanation as to why businesses would suddenly gain interest in expanding production into shrinking demand.

And let’s not forget that taxes and fees are going to change in numerous jurisdictions, including any eventual (if they ever figure it out) rollout of Obamacare.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@4kb.d43.myftpupload.com

Stay In Touch