We spend a lot of time and effort decrying the state of conventional wisdom around here, but for good reason. For gold, convention posits a store of value that is demanded greatly in times of inflation, and as such is a reliable alternate measure of it. In terms of exchange, that would mean investors increase their preference for “moneylike” assets other than devaluing dollars.

I don’t think that is quite right, and, more importantly, completely wrong at exactly the wrong times (or right times, depending on perspective). There is good evidence that this “store of value” property was a driving factor in gold’s rise off the 1999 lows, but this is far too simplistic to provide a more complete explanatory understanding. A full part of that has been the disastrous relegation of gold to just another “investment.” Gold proponents (and I count myself among them) hate to hear it, but in reality gold is no longer money in the most relevant sense. That is an important distinction, one in which the Federal Reserve and modern central banks created with a purpose.

That does not mean, however, that gold is “worthless” in certain monetary situations. Chief among them is “deflation.” Again, I think convention has it wrong here, in that gold can become a money-like substitute in certain situations, a crisis period fraught with conventional “deflation” being one. Liquidity events are essentially currency shortages, and as such it appears on the surface as if dollars and currency are the preferred “flight to safety” (or other risk-free money-like assets, such as t-bills). But these “tail” events are very curious constructions, in that “normal” assumptions are often tested and fail.

It is not atypical to see cash and money-like assets turn to negative yields in crisis. In 2008, that was everpresent for not only cash but also t-bills. Where collateral drainage caused an abundance of demand for government debt, beyond the simplistic description of “flight to safety”, there were episodes of banks charging fees for deposit balances. That negative return on cash provides a window into this “tail risk” insurance of gold. In other words, gold provides not only shelter from debasement but also shelter from the opposite monetary imbalance.

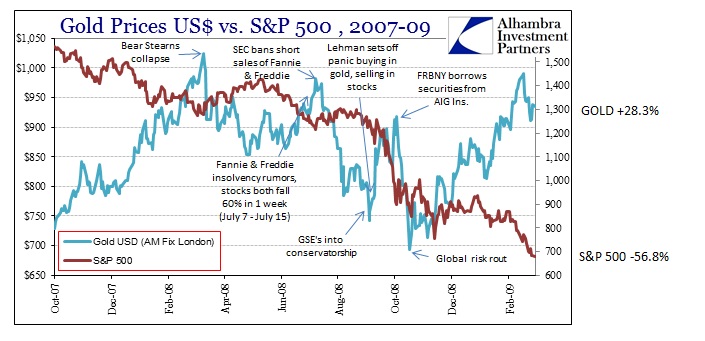

So the primary convention is thrown out the window in the extreme case – during an episode of dramatic “deflation” gold did extremely well in both absolute and relative terms. From the stock market high in October 2007 through the absolute bottom in early March 2009, this outperformance was both obvious and massive.

Gold was up by 28% over that period, while stocks slid close to 60%. That dramatic divergence did not come without a great deal of variance and volatility, of course. The collateral consequences of gold in repo-like markets of leasing are obvious in this wider context (contrast the inverse reactions of gold and stocks around the Bear Stearns collapse; gold tanked as leasing was desperate, while stocks were “enthused” that the Fed would “step up” so dramatically as to provide conditions for an “orderly” transition, but both were only temporary).

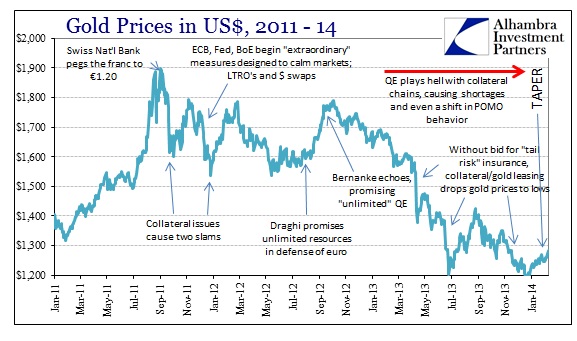

Despite every discrete collateral process in 2008 whereby gold prices were drubbed lower, there was a constant and sharp bid each and every time as overall markets deteriorated. That continued well past the panic period, all the way to September 2011, as the overall financial crisis (still in Europe) now focused on collateral chains of European sovereigns. The extraordinary measures of central banks, even beyond what took place in 2008, began to slowly erode that bid for “tail risk” insurance – regardless of inflation perceptions.

By the end of 2012, central banks in the US and Europe had created enough “credible” space that markets reconfigured their elements of risk capturing. I think that is why credit and stock markets became so complacent (eurodollar volatility was essentially nothing; stocks spiked upward on multiple expansion alone), and gold was so susceptible to leasing.

As discussed many times during 2013, it was the stress of collateral that began these gold cascades. Unlike 2008, however, there was no sharp rejoinder of “tail risk” bids to drive gold back up to the previous level. Instead, 2013 proved a series of waterfalls that ended with everyone burying gold as just the latest bubble (just as central banks hoped). Such commentary fit well within the conventional inflation narrative as well, providing the full package of central bank heroics.

Taper has changed that significantly, yet because most attention is focused on stock prices it gets lost. Credit markets have undergone significant transformation, as most big bank earnings reports are attesting to now, as well as emerging markets, as the paradigm has shifted dramatically as it relates to risk perceptions. The Fed and FOMC voters continue to try the line that taper is not tightening, and it seems they don’t understand the implications of volatility on balance sheet expansion and construction for dollar producers.

The introduction of the taper concept removes one of the primary pillars underpinning the no “tail risk” thesis (the other being a strong recovery, or at least persistent and thus far unrequited pining for one). That requires a change in character and stance throughout the global dollar system.

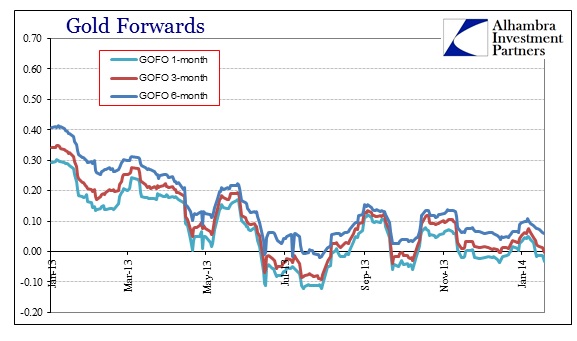

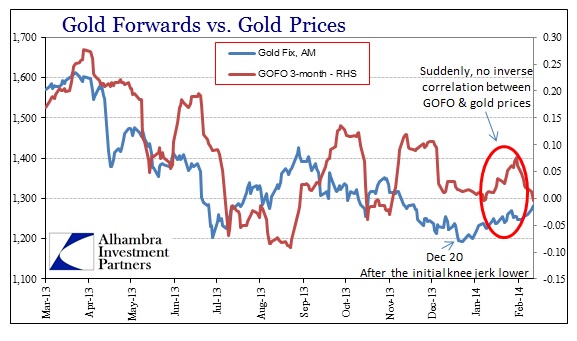

We know that stresses in the physical gold market have become much more evident, as gold forward rates have been near zero and negative pretty consistently since mid-year. Yet, the effect on gold prices has been negligible, especially when compared to these spikes in forward rates that coincide with the gold waterfalls or slams. That seems disproportionate, to say the least, and maybe even counterintuitive on its face, but that is the reality of the gold market that is both money-like and just an “investment.”

However, that seems to have shifted right around the December taper decision. After initially selling off, in what would conform to convention, gold has been moving almost steadily upward ever since. Inflation rates continue to fall, and taper has been increased, but gold prices seem to have caught their bid (finally).

That is confirmed, at least partially for now, by another collateral/leasing episode toward the end of January. Unlike previous patterns, there was no real imprint on the gold price trend. That would suggest, to me strongly, that gold has moved out of the shadow of GOFO depressions. The reason for that gets back to perceptions of “tail risk” as it relates to taper. The world is perceived, by market participants conditioned on omniscience of central bankers, to be a much riskier place with central banks on the withdrawal than inside the umbrella of “unlimited” promises. Thus gold catches its bid, minor as it is now.

If we are indeed heading toward a much “riskier” marketplace, at least with less complacency and much more anxiety (eurodollars and EM’s), then I suspect gold as a “store of value” maintains such a bid without any real or direct relation to “inflation” expectations. After all, taper is supposed to be consistent with lower expectations of inflation, and yet gold has driven higher since the first actual taper. This is not to say anyone should expect a straight line, as 2008’s history amply shows, only that central bank withdrawal is consistent with gold’s post-2007 pattern. It is not inflation; it is pure “tail risk.”

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@4kb.d43.myftpupload.com

Stay In Touch