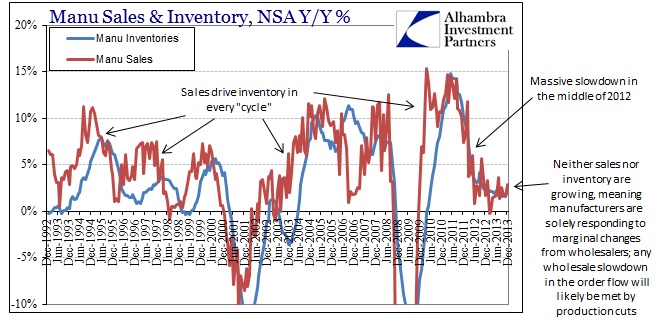

Outside of household income, the main marginal economic factor has been inventory changes. Manufacturers since the obvious 2012 slowdown have been extremely reticent to hold inventory, and certainly at a rate well-below the pre-crisis period. That has made the past two years very unique in that respect, as manufacturing sales and inventory have closely tracked each other.

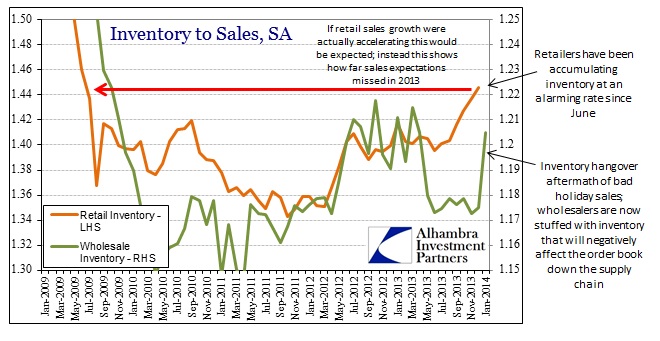

Where it gets really interesting is in the wholesale segment. Retailers responded in 2013 by embracing QE-logic, even after tracking higher inventories after the 2012 holiday shopping season. Wholesalers took the opposite track, having drawn down aggregate inventory levels into 2013. That appears to be a conscious choice on their part, amounting to a “wait and see” approach to the vital second half sales environment.

That has meant marginal wholesale sales have been driven by retailer orders ending up not as customer sales, but flowing directly to rising inventory. The entire supply chain has become “lean” in the sense that marginal changes are solely due to retailer preferences to hold that inventory. With retailer inventory pushing still further to “cycle” highs, coupled with noticeable sales deceleration, it stands to reason that there should be an adjustment process coming soon.

Inventory is usually a shock absorber of sorts as it allows, normally, various pieces of the supply chain to maintain production and activity levels in response to short-term declines in orders. In other words, manufacturers can keep production up despite a drop in orders from wholesalers by simply taking on more finished goods in their own inventory.

But that is not what we see currently, as neither manufacturers nor wholesalers are showing the slightest inclination toward incremental inventory levels. With the “disappointing” holiday sales season boosting retailer inventory levels to a high not seen since the Great Recession, the potential for an “order shock” reverberating throughout the production system rises in each month. Given that wholesalers also saw a rapid rise in relative inventory levels in January (as wholesale sales fell 1.9% M/M, seasonally adjusted) we can see the start of this inventory-led contraction in the supply chain.

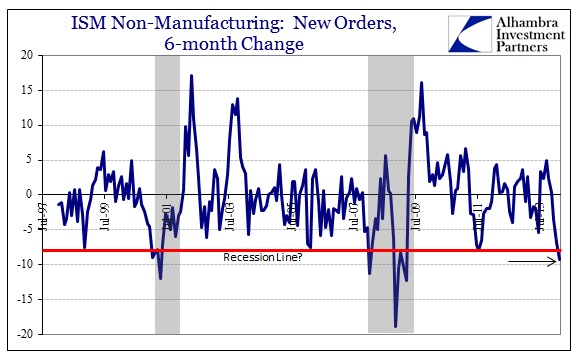

If both wholesalers and retailers are now inventory averse (and we can make that assumption of retailers based on January’s wholesale sales drop) the only place left to absorb the declines is, again, across production. That would certainly conform to what we have seen of the recent ISM estimates, for example. It would also offer a potent and fitting explanation for February’s huge decline in Chinese exports to the US.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@4kb.d43.myftpupload.com

Stay In Touch