The problem with talking about inflation, and there is a lot of it recently, is conflation. Modern measures and concepts about pricing mash together every kind and form to create something that doesn’t really mean what was intended. On the “up” side we have monetary debasement coupling with orthodox concepts of “pricing power” and thrown together with supply shortages and the like. On the “down” side, which is somehow used to offset the “up”, there is the conflation of monetary-driven factors with natural productivity growth that benefits society and drives living standards. Furiously, those “down” factors are both called “deflation” even though they have nothing to do with each other, and one is actually desirable while the other indicates desperate financial difficulty.

The CPI itself began as a means to measure the cost of living, but has been changed over and over to include various adjustments and processes, especially hedonics and imputations. But the macro element that I think is most important is even more basic than arguments about the best way to synthesize all these factors together.

No matter how you compute it, the basic framework of inflation compares prices to previous prices. All the study and focus is on that process, figuring which prices to start with and then how to measure price change from period 1 to period 2 and beyond. In real economic terms, that doesn’t really get to the heart of “inflation”, that being redistribution.

As even an academic concept, redistribution is exceedingly difficult to define let alone measure. That is the primary reason it is never attempted. Basic intuition, however, helps solve the conundrum, particularly in that rudimentary foundation of the entire affair. What we really want to get at is price changes in relation to income changes.

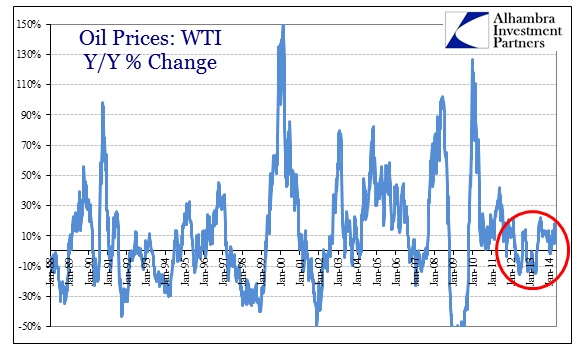

The current period is described as “disinflationary” as various and sundry official figures show “inflation” low and getting lower, particularly as they remain below the FOMC’s target of 2%. The primary expression of price changes is incurred from energy, as oil prices more than anything are systemic and endemic during inflationary episodes.

Despite more recent increases in oil prices, the rate of change is relatively benign by comparison to previous periods (particularly the housing bubble and the early Great Recession). That would seem to concur with the orthodox interpretation of disinflation or low inflation that is being used as “cover” for justifying monetarism.

Using oil prices as a proxy, recent history shows exactly that. But there is a significant problem here, particularly going back to the housing bubble period. We don’t get any sense of systemic redistribution by counting current prices compared to previous prices.

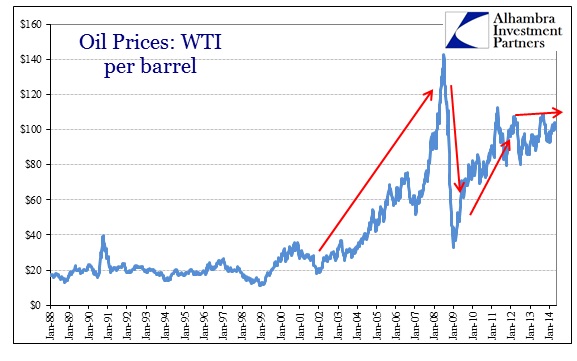

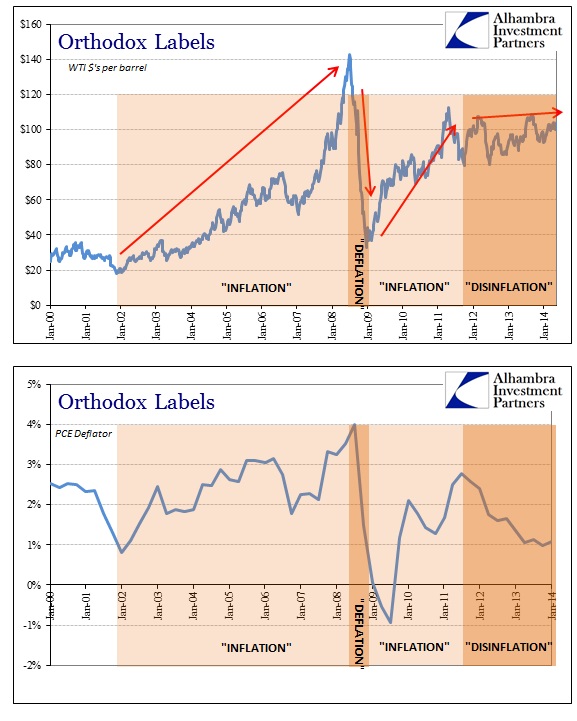

While oil prices and the PCE deflator (the Fed’s preferred inflation gauge) mostly agree with the orthodox labeling that I have inserted above, the absence of redistribution more than clouds interpretations and analysis. Not only are we comparing current prices to former prices to arrive at inflation, the measure itself is a second derivative of that process.

West Texas Intermediate (WTI) oil prices jumped back above $100 per barrel in early 2011 on its way to about $113. Since then, WTI has largely been up and down around that same baseline more or less. So if we go back to the orthodox textbook and compare current prices to previous prices, measuring only the rate of change (second derivative), it nets out at about 0%. Under these terms inflation looks to be non-existent (roughly).

The problem, however, is that income growth has also been non-existent (roughly). Had incomes been growing moderately while price changes were benign, disinflation might make sense as a label. That becomes clear when you compare periods where prices and incomes are changing at different rates.

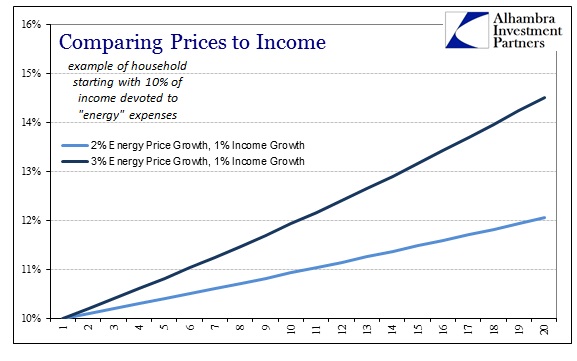

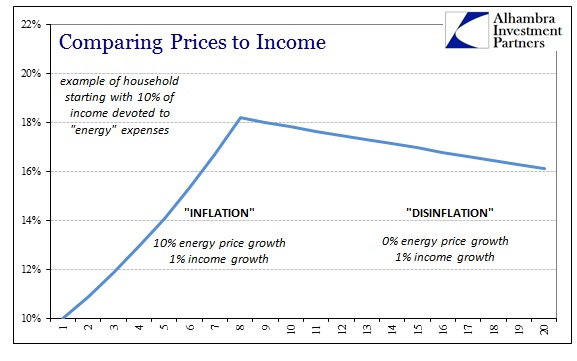

If you start with a hypothetical and highly stylized example of a household that devotes 10% of income to a generic “energy” good, after 20 compounded periods where “energy” prices grow moderately at 2% but income grows at only 1%, by the end of the study period the amount of income devoted to energy has risen to 12% of total income. Change the terms to a 3% price change for that same income stream, and by the end proportionality has grown now to 14.5%. That illustrates as much how compounding is an extremely important factor in all of this and thus the more time this imbalance persists means huge opportunity costs are being incurred.

Such price erosion for given income also means forgoing spending in other areas or searching for substitutes. Both are downstream impacts of redistribution and almost never lead to positive economic outcomes in the aggregate.

Where prices are changing consistently at a higher rate than income (redistribution), the words “inflation”, “deflation” or “disinflation” become almost meaningless.

That is especially true once you begin to piece together a fuller reconstruction. If income grows only modestly throughout and inflation starts out “hot” but is only transitory, to borrow Chairman Bernanke’s 2011 wording, the net effect across both periods is an obviously diminished situation for our hypothetical household. Because income never materialized to a significant degree, the offset of benign inflation in the second period is nowhere near enough to overcome the impoverishment of the first.

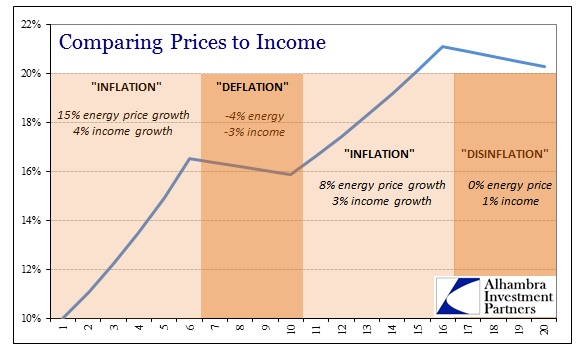

Further, if we actually create a four stage model like that of the housing bubble, Great Recession and “recovery”, the impact of this disparity is clearly immense.

Neither of the deflation or disinflation periods in my example do much toward restitution of purchasing power or whatever semantics you might use to describe redistribution. As long as a negative differential exists between incomes and raw prices, the net effect will be impoverishment. That only gets worse once debt is factored as one of the means of redistribution.

NOTE: the examples shown above are not meant as “scientific” reconstructions of actual conditions or even simulations as such. These are included only as illustrations about the potential downside of redistribution.

The simplest way to think about all of this is gas prices. It doesn’t matter that gasoline hasn’t much changed in the last several years as incomes have never had the chance to adjust upward to that level – even going all the way back to 2008. So where inflation looks to be absent now, gasoline is still just as relatively expensive now as it was in 2011 or 2008 to the household with no experience of asset inflation. If the economy had actually and sustainably recovered even modestly, the relative calculation between income and prices would be totally different and then the term disinflation might hold some relevant meaning.

To get households, particularly those at the “bottom” ends (which captures the great majority in simple numbers of people), back to where they were would require “deflation”, and a lot of it. By keeping prices high relative to income levels that have made so little progress after the decimation during the Great Recession, an enormous drag on the economy remains firmly in place. Even though inflation looks to be low in official figures, denoting nothing more than that nominal growth in the economy remains almost nonexistent, the cumulative effect over time has been heartbreaking.

This powerfully negative factor in choosing a debasement path for economic control is never acknowledged, but that doesn’t mean it doesn’t exist. Some persistent headwinds aren’t so mysterious under light of common sense.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@4kb.d43.myftpupload.com

Stay In Touch