There is so much about the repo market that gets lost in the minute details that are more often than not counterintuitive. It can sometimes be confusing as to why counterparties might be willing to pay you to borrow their cash, which is what a negative repo rate actually indicates. In that situation, which is what we are talking about of highly “special” securities, it is the actual security that is in demand far more than the cash. It is basic supply and demand dynamics just flipped over to the other side.

On that “other” side are those that are persistently “lent” out credit securities. In the “old” days before repo went ballistic (the 1990’s) those that would pay you to borrow their cash did so because they needed a particular security to close a short position. Shorting is essentially borrowing a security and selling it with the very real need to replace it in the future – and in a lot of instances at a time not of your choosing. So in that position, the need for a security is far greater than any need to generate a return on cash you are “lending”, to the point that you actually pay a negative interest rate.

That situation got far more complicated in the 2000’s as rehypothecation became far more prevalent. A very large part of that process was driven by monetary policy and rate suppression, as low interest rates “forced” participants into new means and measures for creating returns. In some cases, insurance companies and other large institutions that had large stores of largely inert bond positions, including a “wealth” of UST and MBS, began to run large securities lending operations to generate an additional spread. Enhancing that further meant lending a single security in more than one instance, sometimes over and over and over, etc.

A further complication arose as dealers began to participate on both sides, borrowing repo to fund balance sheet positions while also lending out securities in their warehouse inventory – all designed to reduce borrowing costs as close to nothing as possible while at the same time picking up as many basis points of return as humanly possible (with regressions and Greeks). As the bubble progressed in scope and intensity, proportionality was sacrificed under the “cover” of faith in the Fed and the sweet allure of proprietary trading profits (which is where all this “hedging” gets placed).

You would think, intuitively, that in such a situation of persistently negative repo rates there would be a rush to borrow the case and close the gap; indeed there typically is as that represents the “market” arbitration of imbalances. But where “specials” get deeply negative, which means, again, getting paid to borrow cash, you have to conclude that there simply is not enough bond inventory of a particular security or maturity (or even class) to satiate the need. There is opportunity but no takers, or at least not enough.

The problem, in more simplistic terms, is that credit securities are not always “available” for market needs. If they reside in close “silos”, again such as insurance companies or dealer warehouses, they can be activated once the spread reaches some mathematically defined risk calculation threshold. That has been complicated very much in the post-crisis age, as securities lending businesses were a great source of pain and problem; many have been pared or shut down. Even dealers have been squeezed by capital concerns like leverage ratios in Basel 3 and, as I tried to explain yesterday, profit considerations for holding inventory ready for market conditions. It seems as if balance sheet costs for holding market-available inventory now far outweigh any spread that might be picked up for doing so. That is saying something given that negative repo rates have become, apparently, far more frequent and deeper.

The less credit securities are in this “ready” position, the greater the problem with respect to acute outbursts of demand (either for a particular security or for repo in general). That is why the Fed’s reverse repo program is such a disappointment, as QE was up to the point of the program’s initiation a process of (potentially) taking collateral away from “ready” status. The Fed presumed that reverse repo access to the vast and still growing SOMA holdings “silo” would act as large additional shock absorber for repo demand – it hasn’t at all.

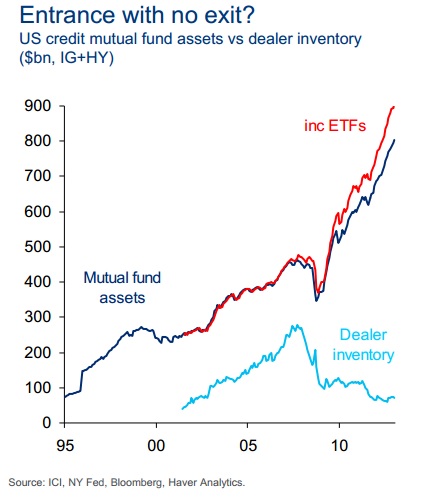

What we are really talking about here, in big picture terms, is the size of the exit. In all honesty, for all the endless talk about liquidity, what it really represents is the ability to take on a significant and determined selling pressure without courting major disruption and disorder. What all this repo fail and specials are saying, in generalized terms, is that the size of the exit has grown significantly smaller just in the past year or so (probably since QE3 started its disruptions), after having already done so consistently since 2007.

But that is actually worse than it sounds. While the exits have grown narrower and flimsier, the actual size of holdings that someday might be in serious need of exits has grown massively at the same time. Again, going back to last July’s TBAC report, the situation they presented in corporate debt applies far more broadly now:

As I have noted many times in the past, we saw this in action last May and June in MBS trading, and it was ugly. For what occurred, that is incongruent to the largely benign conditions elsewhere, including the corporate market that so spooked TBAC a few months later.

The larger focus here needs to be in that direction, as it is now well-beyond just corporate debt and dealer capacity to handle potential disorder in that narrow circumstance. That has been echoed and replicated under real, but relatively calm conditions, in MBS and now UST repo. Everywhere you look in credit “liquidity” there is a diminished feel. That is not good.

As I said yesterday, “Liquidity is the one element that is so very difficult to understand and measure, and it is never about what you see today, it is more about when you need it.” That is what should be most concerning as liquidity under stress is always less than you think heading in, but what does that say when capacity is so eroded long before you ever get there. Very narrow doors and huge and growing crowds (all on the same side) is an unnecessary risk, and far more than a “tradeoff” as Janet Yellen alluded in April.

It should not be lost on anyone that this is not ideal, owing totally to the FOMC’s own process of trying to create the “aggregate demand” the Fed so much sought over the past few decades. The entire repo system was an integral part of building up the credit production that now gets lumped into the Great “Moderation.” Structural problems indeed.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, contact us at: jhudak@4kb.d43.myftpupload.com

Stay In Touch