More bad news for the rest of the world, or at least the world’s economists, that has been anticipating the US economy as a means by which to expel negative economic forces. The idea of decoupling is not just something that suggests the US economy is moving contrary to all the rest, but also the sole source of hope for anything but a dramatic decline once again. Outside of the Establishment Survey and the unemployment rate, there has been nothing to suggest that any such divergence has existed. The most pertinent data, especially trade data, has been unambiguous in actually pegging the world’s declining fortunes to the lack of actual growth of the US economy.

While that was “good” enough to describe the rut that had befallen in 2012, most recent months, especially the dismal nature of January’s updates across a broad cross-section, increasingly suggest an end to even that nearly three-year furrow – but not in the direction that payrolls anticipate.

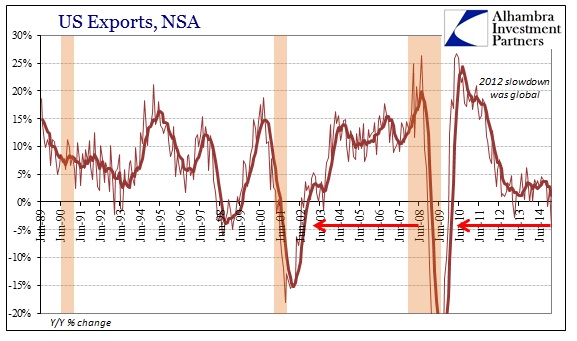

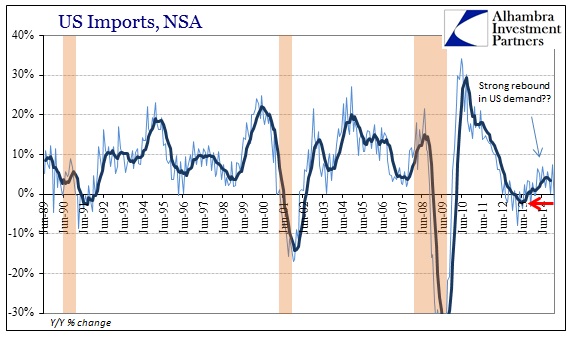

The latest trade data from the Census Bureau surpasses the ugliness we have come to expect of the elongated cycle. Both imports and exports fell year-over-year in January, as weakness, contraction even, is now universal in terms of US demand for foreign goods and foreign demand for US goods. Trade has ground to a startling halt.

On the export side, the drop was by far the worst since 2009. That may suggest another reason for the Chicago PMI’s dramatic collapse of its own, which would be very concerning since it would mean that far more than just the energy sector is contracting under the weight of lack of “demand.”

This steep (and steepening) decline began somewhere around August, which completely fits within the timeframe of the “dollar” and the view of the global economy provided by related “dollar” liquidity and commodity prices, especially oil. In terms of US GDP, this is a negative factor as exports fell much faster than imports.

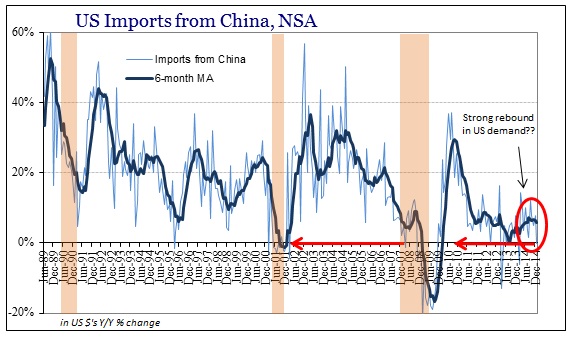

For the rest of the world, they care little about US GDP as the decline in imports means less business overall (doesn’t matter the “dollar” exchange rate). Our biggest trade partners, especially China, are already under economic pressure from the lack of any true recovery after the Great Recession, but are now coping with the potential for even worse trade levels.

Using a closed system approach, as most economists do, you can actually expect that exports and imports would diverge and the US could “decouple” and lead a global resurgence. Realistically that was never an option as the relation of global trade, linked by the “dollar”, has continually suggested since 2012 an eventual dislocation that applies universally. The slowdown in China is directly related to the slowing levels of US “demand”, which in turn is transmitted to other nations that would import US goods. The system is wholly contained of all trade, and thus global trade itself is perhaps the key barometer of the global economy.

That offers one reason why “competitive devaluation” doesn’t actually work, as it is not a zero sum game (one country gaining at the expense of another) but rather currency “wars” subtract from the whole altogether (both countries lose). The entire point of currency destabilization is exactly that, and business transpires less and less under more extreme versions of instability – intentional or not.

No matter how you want to view all this, January was perhaps the worst month for US trade since the Great Recession. For domestic production, which will matter at some point for even the payroll reports, the serious decline in exports is a most distressing development. For the rest of the world, as if it weren’t clear enough already, the US is not coming to save the day – US consumers have never fully rebounded and are now growing even more cautious (savings rate) or have even less to spend (“disinflation” or not).

Stay In Touch