Let’s start by stipulating that the ECB’s operations are far more complex. This is the case both in terms of actual operations but also in trying to figure out what goes where and why. That is at the start unsurprising given the European monetary framework; even though the euro as a denomination is continental there are still national fissures in the monetary processes. The ECB sits at what is thought the head of it all, but each national central bank (NCB) still holds a far more than symbolic place within the system.

Take the recent QE, for example. If looking for QE’s liquidity effect in 2015 you will be hard pressed to find it; and once you do it doesn’t look like what you would think of it given the American version’s dance upon preconceptions. While the ECB holds veto authority and direct policy creation about where QE is to be directed (including proportional allocation by sovereign issue), it is left to each NCB to actually do the buying from local banks or the “market.”

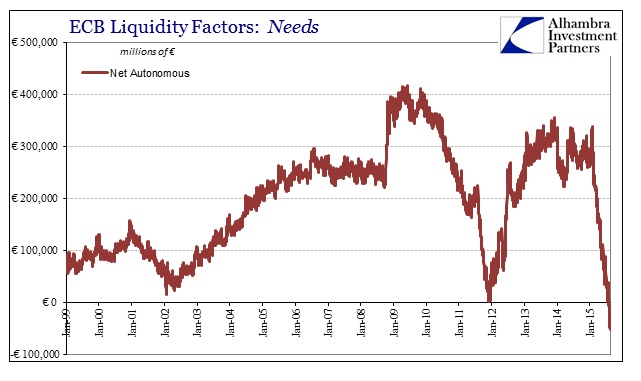

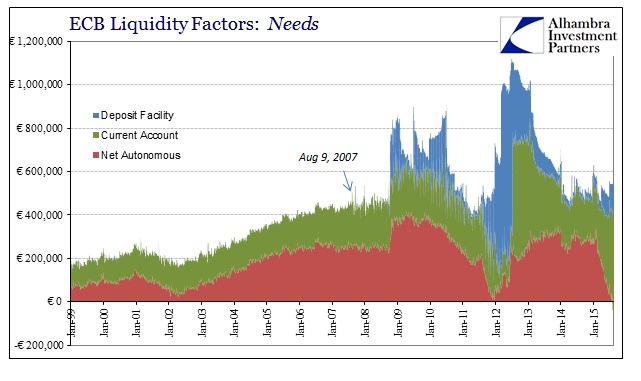

Total liquidity “needs” (not really “needs” but what banks do with all this monetarism at the end of it) then don’t show any QE effect. On this side of the ECB Liquidity Analysis, there are three components: the current account, the deposit facility and net “autonomous factors.” That last part is where QE shows up directly, but counterintuitively as a deduction. Net autonomous factors, as the name implies, are those thought beyond the ECB’s discretion and which include demand for banknotes and coin, government deposits in the Eurosystem, and the investment portfolio of the NCB’s.

The investment portfolios of the NCB’s are actually complicated, as it includes assets such as foreign reserves both long and short (netted) but also direct securities held, thus those from the PSPP (QE). In sum, what is thought to be a direct increase in “reserves” or liquidity from it at least starts out as a deduction:

Since the PSPP began on March 13, the liquidity “needs” of the autonomous segment have declined from €203 billion to -€51 billion; total PSPP “purchases” directed to the NCB’s has totaled €269 billion to the latest update (August 17). The PSPP is not the only re-arrangement of NCB assets, however, as we also have to factor the Greek ELA usage for this year (since the ELA is also structured similarly; ECB policy decision but NCB portfolio).

We don’t know the exact figures for the ELA as the ECB reports those balances combined within its “Other Claims on Euro Area Credit Institutions”, but that ECB line item was €58.7 billion on January 23 just prior to the Greek election rising to a peak of just about €140 billion in late July (and €133 billion most recently). Going back that far, net autonomous “needs” have thus declined from €321 billion to -€51 billion for a net change of -€372 billion – give or take €40 billion or so depending on the actual start (or maintenance period) of the comparison.

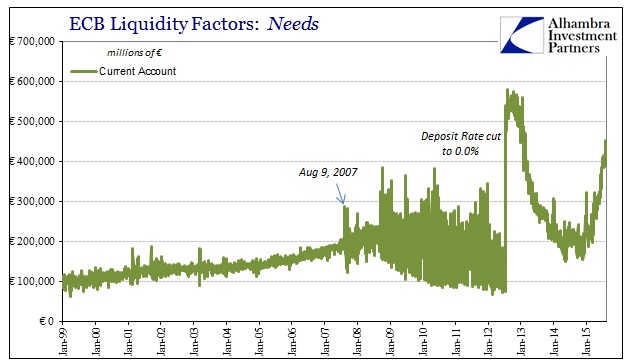

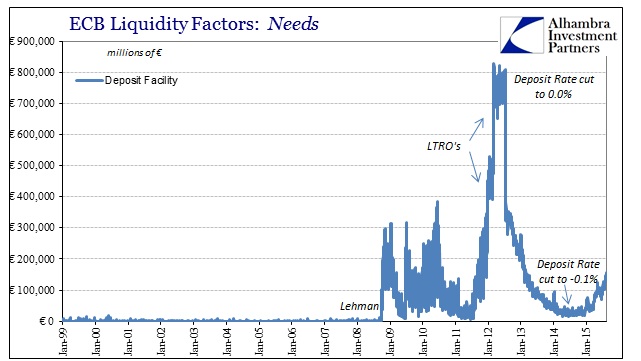

Once PSPP activity, as well as that from the ELA, is conducted by the NCB’s, it is all re-routed back to one of the other accounts. The current account has increased by about €227 billion in that same time, while the deposit account balance expanded by €108 billion. The difference, about -€37 billion, works out from the liquidity “supply” side with reduced Open Market Operations (OMO’s) from maturing LTRO’s (2011 version) and new T-LTRO’s of reduced take-ups.

That surge in the deposit account is more than a little curious. The rate “paid” on those balances, held by euro banks, is currently -20 bps and has been since September 2014, having been cut from the -10 bps set last June. The intent was obviously to try to get banks to do something with those “reserves” of euros, but instead during the QE period it has managed to find another €108 billion at a seriously negative nominal rate. That more than suggests something amiss where banks are content, apparently, to be penalized on more than €154 billion in total.

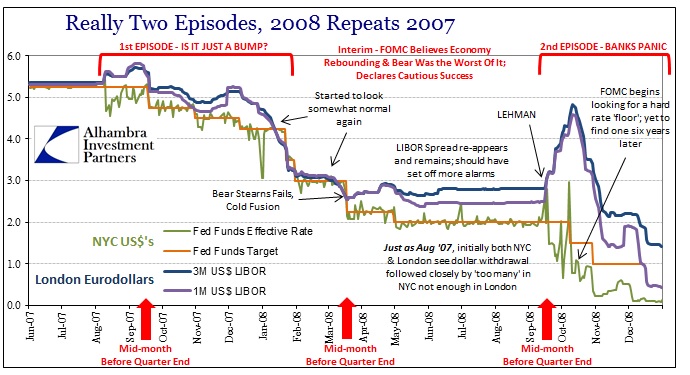

The net of all this is simply that the ECB has been quite busy, even if it is at times somewhat difficult to describe just how busy. In fact, the ECB’s entertainment of its own accounting is visible dating back to August 9, 2007, no matter what form that has taken in the now eight plus years since.

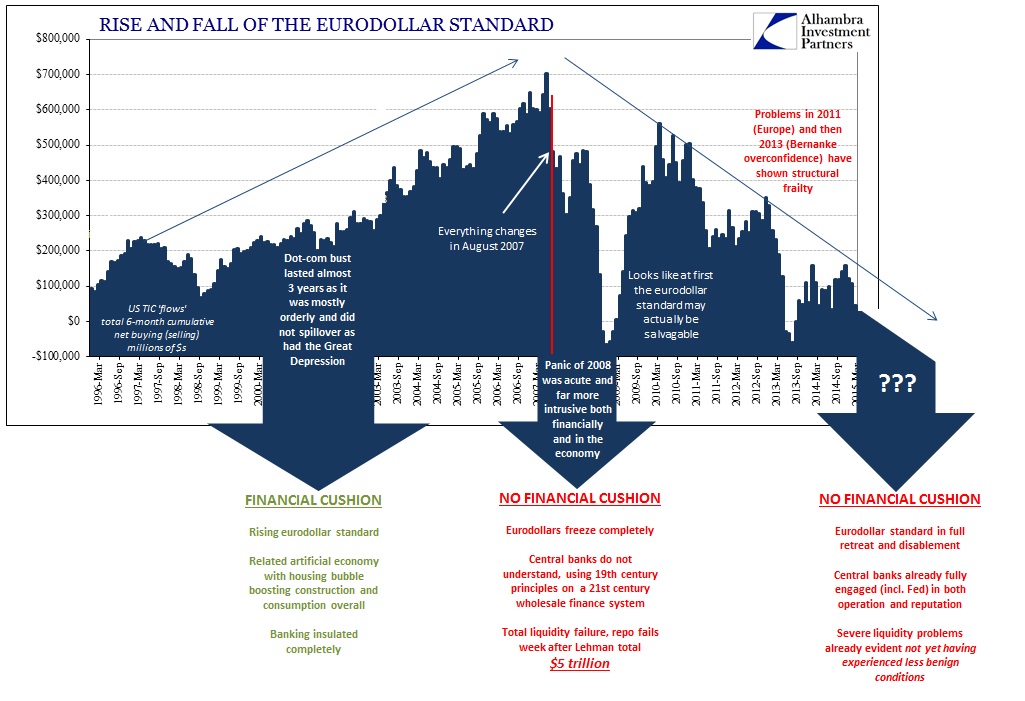

As I mentioned above, this simplified balance sheet view is not a comprehensive statement about just how much the ECB is doing at any given time with or without its NCB counterparts, but is instead remarkable for the clarity upon the systemic break in the summer 2007. The distinction from the pre-crisis to the post-crisis is paramount, and its continuation no matter what the ECB handles or how it is handled is highly significant.

In sum, what is classified as liquidity “needs” is really just the leftovers after all is said and done. In that regard, the European monetarism of the past almost decade is the same as the American version. The Federal Reserve’s operation is far more simple and clear, but the result is the same – the leftover from the four QE’s show up as “reserves” which are in concept the same thing as Europe’s liquidity “needs.”

In terms of direct action, the Fed was even further behind-the-curve than the ECB because of how it thought banking worked in terms of its interest rate target; misunderstanding not just wholesale operation but the even more basic geographic split between “dollars” in NYC and eurodollars in operation. It was a liquidity premium that suggested a fragmented liquidity operation, belying the very concepts underpinning basic monetary assumptions about monetary transmission. That is, of course, what all this is about – transmission of liquidity, through credit creation, into the economy. The theory was set by Friedman and Schwartz in 1963, and each central bank has been carrying that out in their own way.

There are a few takeaways from this cross-Atlantic examination, but primarily there are two. In various ways and means, neither central bank knows very much about what they are doing. Sure, they have a good and tight grasp on arcana and accounting for it, especially on the European side, but so what? And that is the second, related and most important conclusion from all this, namely that it hasn’t mattered whether central bank “liquidity” operations are utterly complex or expressively simple; the results have been shockingly correlative. Neither the American economy has recovered, nor its European counterpart.

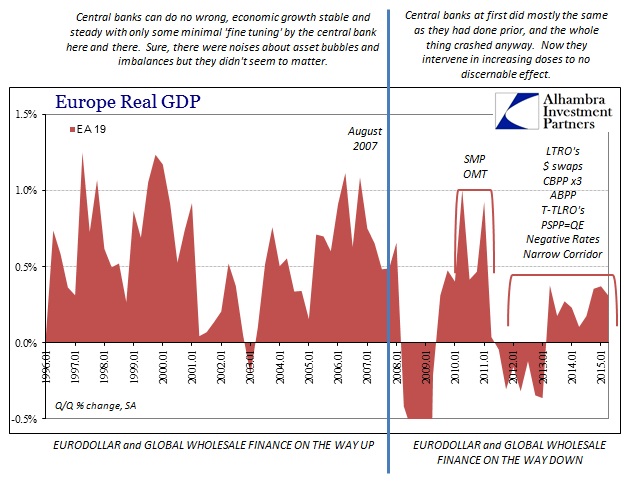

Instead, both economies have exhibited far too much closeness, both before the collapse into 2009 and thereafter; the 2012 slowdown in the US, just now being more properly surveyed, and the re-recession at the same time in Europe; the trajectory of “inflation” in both America and Europe is exactly the same downward slide, with variations here and there, of course, pointing to the same “deflationary” collapse at the same time no matter what either central bank system does or does not do.

What matters, apparently and intuitively, is not the manner of carrying out all this monetarism but the reasons for it in the first place. Friedman might have been correct about the 1930’s, and even that is arguable, but that is no direct suggestion to the 21st century wholesale system. In the farce that is these monetary operations, in light of the results especially into 2015, it’s almost as if they were either completely helpless under the duress of a greater governing dynamic or set out to totally disprove monetary theory from the ground up as at least inappropriate to modern “money” if not completely wrong to begin with. That is where this is heading, as anyone not ideologically committed to monetarism should observe and conclude as much. You have every form and manner of central bank “liquidity” being conducted to the same scary results, covering almost a decade so far.

Stay In Touch