There is always some chicken and egg to any financial irregularity; as in does a crisis cause a panic or is it the panic that causes the crisis? Though the evidence of the past eight years is decidedly on the side of the irregularity, central banks continue to press as if that were not so. In no uncertain terms, central bankers persist in expressing their own confidence and, if you read or listen closely enough, great disdain for free markets they deem unworthy as if nothing more than unchained emotion. In the context of 2008, as the current FOMC tells it, the markets got all worked up over nothing much and should have instead simply enjoyed the blind faith in the Fed to have fixed it all without the fuss and bother.

As offensive as that sounds, that is exactly what is being preached. Janet Yellen in April 2014:

Fundamental to modern thinking on central banking is the idea that monetary policy is more effective when the public better understands and anticipates how the central bank will respond to evolving economic conditions. Specifically, it is important for the central bank to make clear how it will adjust its policy stance in response to unforeseen economic developments in a manner that reduces or blunts potentially harmful consequences. If the public understands and expects policymakers to behave in this systematically stabilizing manner, it will tend to respond less to such developments.

There is a fatal fallacy at the heart of this philosophy, one in which has blinded these economists as they marvel at their own assumed powers. Yellen suggests that markets should stop worrying so much about liquidity and other perhaps tangential, but no less meaningful, factors and instead only ignore them in the comfort that Yellen has those all under control. It is no less destructive conceit, one which was revealed to all amply this past decade – starting with the housing bubble itself.

In reality, investors and market agents have good reason to concern about both markets and central banks. Yellen says that they are in perfect position to handle whatever may come, but that clearly hasn’t been the case. Instead, central banks all over the world have been forced into one ad hoc program after another, which by itself refutes Yellen’s assertiveness. Rather than instill great confidence to do as the Fed Chair demands, central banks have only proved themselves far too in love with themselves. In order for this end of the Yellen Doctrine to work, central bankers need to stop thinking that everything they do is magic and saying so.

We can see that problem in ways both great and small, as “managing” Bear Stearns’ collapse in March 2008 didn’t round out the bottom but rather only instilled unearned confidence in the Fed that, again, their efforts would work. Bear was a great warning to be prepared about truly dire consequences, but somehow the FOMC was wholly unprepared for Lehman, AIG and the rest (including the GSE’s), leaving them scrambling and again pulling together various spontaneous programs from nowhere – and to no avail. Bernanke says that central banks can mitigate recession, so how come the Great Recession? This scenario was repeated (repeatedly) in 2011 and in smaller ways since.

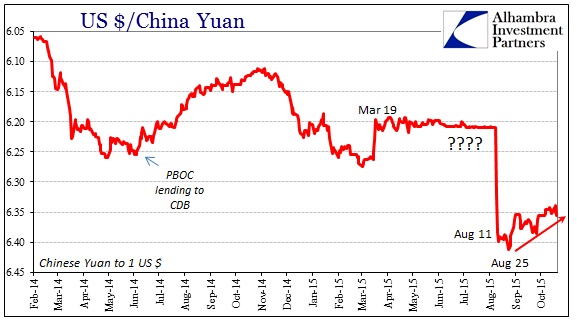

I believe, in large part, that August 2015 represents just the latest in that gap between how markets do and should work and the ideal utopian scenario central banks plan for. The PBOC, far more so than the Fed, has enjoyed a reputation for control and management that seems to closely align with Yellen’s doctrine (totalitarian envy, the true financial law of central planning hard and soft). The events of August showed once again that there is no true control, only the illusion. The PBOC had clearly “engineered” a RMB/US$ cross without any volatility or variation whatsoever. Rather than view that as Yellen wishes, it was another ad hoc attempt to control and manage a far greater force – a force that none of the central banks wish to appreciate.

In order to contain yuan trading meant any number of growing intrusiveness, none of which we will ever likely know for sure. We can infer from various market components and then make reasonable judgments and extrapolations, but what is hidden and opaque will remain so until revealed by time. The PBOC and Chinese government have, in the past, used that to their advantage, cultivating the legend of near-omniscience for the PBOC, but since August what seemed to be beneficial in screening the true nature of market conditions might now turn in the other direction.

The narrative about China’s “dollar” efforts has been entirely focused on “selling UST’s” when that is only the gloss. As I noted a few weeks ago, the record of US t-bills more than suggests a deeper financial invective against “dollar” irregularity. It would be preposterous to think that the PBOC would be limiting itself to such an unsuitable arrangement; that the Chinese central bank would not be undertaking much deeper and intentionally muddy measures to at least run down and transform the immediate problem.

That would mean “reserve” mobilization would have been much more comprehensive and far deeper and multi-dimensional than simply “selling UST” of whatever class. In other words, if the PBOC was altering its bill strategy and engaging outright selling of UST securities, it was surely engaging repos and likely swaps of all flavors. After all, collateral in any of the derivative “reserve” activities is usually UST’s anyway.

It would also suggest transactions in forward contracts, a type of instrument the PBOC is intimately familiar with through its yuan management methodology. Thus, looking at the China’s “dollar” problem through the lens of wholesale finance opens up greater possibilities as far as what China has done (and is doing) about it.

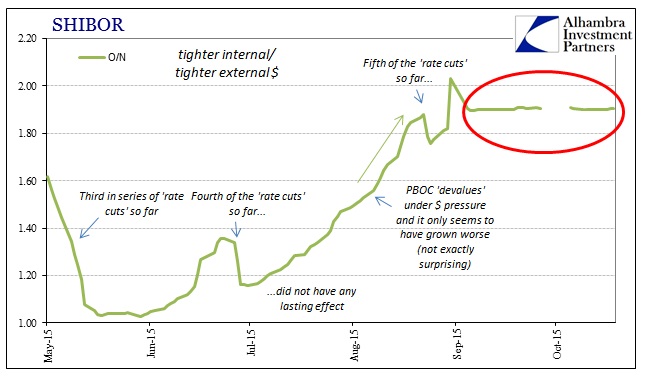

To this point, it has worked on two fronts. Liquidity volatility has been somewhat improved (though, it has to be pointed out, the boot of PBOC yuan measures remains on SHIBOR which while providing immediate cover only increases the cost down the road) and, more importantly from the Yellen Doctrine standpoint, the “capital” flow numbers for September fooled any number of economists and commentators into issuing their verdict of an end to the emergency. That, of course, was nonsense as any deeper, wholesale appreciation for the PBOC’s tools and likelihoods suggests the opposite; namely that China has indeed followed Brazil. This was no end to the problem, but merely the end of Chapter 1 (if you wish to start the ordinal order at August rather than related prior “dollar” issues).

As Brazil, the PBOC is proving far against any omniscience, instead it, too, is Fed-like mortal in being forced to inefficient and belatedly improvised emergency stirring. The use of forwards as a liquidity tool against a “dollar” run is as dangerous as the run itself because it moves the strain only in maturity (from immediate to more intermediate) but with a geometrically progressing “cost” and potential disorder for doing so.

Which brings us all back to the question about what, exactly, is an “outflow.” If a flood of PBOC-generated swaps and forwards sets up only a maturity transformation moving the “dollar” pressure from August or September to October and November, then being effective means being able to either deliver “dollars” then (instead of September) without an October disruption, or going deeper into maturity transformations (a form of, as noted above, high cost future indebtedness) in order to continue fooling “markets” into thinking there is nothing going on at all by maintaining this same outward appearance of resumed stability. That latter is surely the motivation behind O/N SHIBOR’s sudden meaninglessness.

In my view, and this is speculative on my part but I don’t think unreasonably so, the October 15 reserve mandate seems to be a hedge on the PBOC’s “dollar” intentions as far as taking the first option so as to keep the process to as much of a minimum as possible. The second option, which is what Brazil opted for (as does every other central bank when forced by sustained “dollar” turmoil), is too asymmetric – you gain more maturity transformation, kicking the can further, but the cost to do so increases more geometrically than linear.

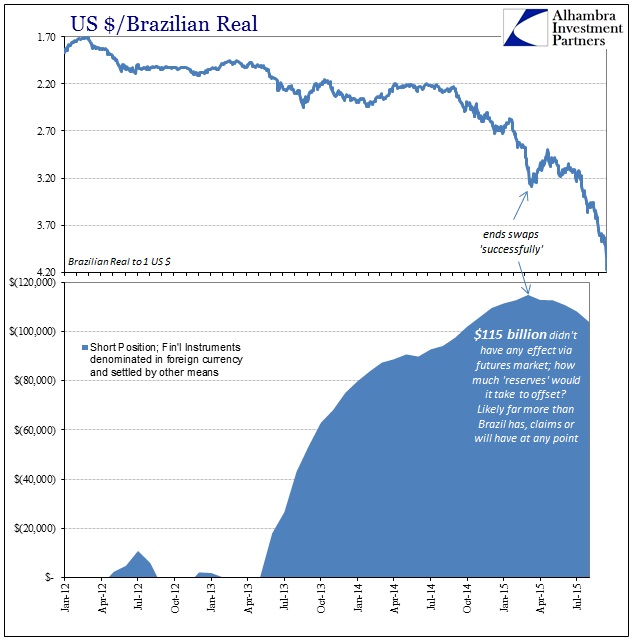

The Brazil case is not exactly analogous given its unique financial connection to the eurodollar system and how its central bank attempts to manage it, but the situations are in general terms identical. Brazil found itself in “dollar” trouble in the middle of 2013, instituted swaps and forwards and “bought” only a few months peace and the appearance of calm. Once the maturity transformation took its place, starting September 2014, the real has been obliterated an order of magnitude worse than imaginable at the start of the program in 2013.

In my analysis, Brazil had no plausible escape from the “dollar” and thus the central bank’s efforts only amplified greatly the inevitable. From what I have seen of China, especially the first crack at the “dollar” run through July and August, I can’t fathom why they would find themselves any different. That point is bolstered by the belated recognition, in the mainstream no less, the wholesale inner workings that have, to this point, masked the continued difficulties:

The People’s Bank of China and local lenders increased their holdings in onshore forwards to $67.9 billion in August, positions that would boost China’s currency against the dollar. The amount is five times more than the average in the first seven months, PBOC data show. The positions are part of a three-stage process to support the currency without immediately draining reserves, according to China Merchants Bank Co. and Goldman Sachs Group Inc.

Standard central-bank intervention to support a currency generally involves selling dollars and buying the home tender. In this case, China’s large state banks borrowed dollars in the swap market, sold the U.S. currency in the cash spot market and used forward contracts with the central bank to hedge those positions.

In the parlance of what I have used to describe for Brazil, the PBOC like Banco do Brasil enticed Chinese banks already short (synthetically) the “dollar” to become more so – all because they are coaxed into believing, as Yellen, that the central bank will have it covered on the other end. The PBOC’s motivation is only immediate, just hoping that the unwind into the future can be more manageable. What Brazilian banks found was quite the opposite, and Brazil is now suffering greatly for it.

That last is the central issue here, namely that doing as Yellen and her counterparts demand is the biggest risk of all. The Yellen Doctrine requires that central banks be both correct and able, abilities that have been (and can only be) in utter short supply. Her view would show more proactive and effective central bank management where only reactive and impromptu, last minute white-knuckling has abounded. Central banks have been in the past year only holding on for dear life, which is where obscurity has been their benefit. In the end, however, I think it their own downfall as it only serves to make matters worse. Yellen wants the central bank to be viewed as almost godlike, but they continually reveal themselves weak, deceptive and ineffectual; eschewing all long run sustainability in order to just make it through one day at a time.

They really don’t know what they are doing and China’s forwards put yet another exclamation on that point. That is why I have claimed these past few months that the central bank’s worst nightmare will be when wholesale exposure is revealed and appreciated as exactly the problem rather than the solution. Making Chinese banks “more short” the “dollar” is like giving a morphine addict keys to the medical locker and expecting the printed warning labels as enough to deter overdose.

Stay In Touch