Once more we find no end in sight to the Chinese slowdown. To complete the weekly sweep of highly negative Chinese accounts, the major three released today were unfortunately complimentary to those already publicized. Only retail sales accelerated and by the smallest increment; in context, however, at 11% retail sales are still lower than the worst month of the China’s end of the Great Recession. Industrial production fell back to 5.6%, matching March (no more “transitory”) for the worst growth rate of this “cycle.” Perhaps most meaningfully, fixed asset investment (which is presented as an accumulated YTD growth rate, leaving indirect inference for individual months as they come out) was only 10.2% and the lowest levels since December 2000.

Private FAI, a relatively new addition from the National Bureau of Statistics China, was only 10.4% in September, having been 18.1% at the end of 2014 and 23.1% at the end of 2013. By all counts, the economic climate in China in 2015 is substantially worse than the rather steady slowing that has been at work since 2012. Despite the obviousness of that baseline, each positive monthly variation has been taken as if “stimulus” was working, only to be dependably tossed aside as long-forgotten, inappropriate memories. It is, instead, becoming increasingly clear the PBOC has no real power or effort by which to arrest the trend should it actually attempt to.

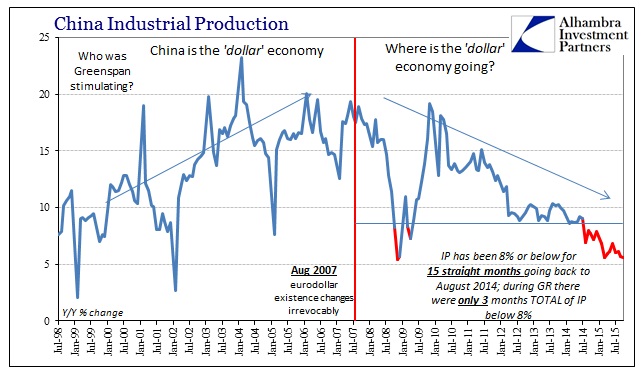

By far, the worst element of China’s recent experience is the torture of extension. In other words, quite unlike even the worst of the Great Recession, this slowing is unending; grinding lower month after month after month (seeing past, of course, those monthly variations). It is almost too unrealistic to contemplate, but industrial production had been 8% or below in China for only three months during the Great Recession; it has been 8% or below in every month dating back to last July, for a total of 15 months and counting. That turn, while still conforming to the 2012 trend, represented a new amplification that dates exactly to when the “dollar” found new “tightening.”

Industrial production in this direction had been assigned to China’s internal bubble dynamics exclusively, but the account of other economic data more than suggests otherwise. Again, retail sales have been steadier of late certainly in comparison to China’s marginal industry setting, but fixed asset investment truly produces the comprehensive notation. Consisting of fiscal “stimulus” effects as well as, again, private investment in productive capacity, China’s FAI is showing up as both the Chinese view of the “dollar” as well as where all this really starts – the end of the US recovery, particularly the final strangling of the US consumer in 2015.

As noted yesterday with China’s PPI release, the sharp and really amazing slowing in investment capacity has failed to quiet producer price discounting, a quite steady if ominous signal about global “demand.” We don’t know what the private sector level of investment was prior to 2012, but we can reasonably assume it significantly more robust even than the full measure the NBS has constructed throughout (private FAI at its inception in March 2012 was 28.6% vs. 20.9% in full FAI). To go from whatever “normal” private level, at least in terms of China’s past experience with eurodollar operation, to just 10% now and still have producer prices falling steadily at nearly 6% suggests not just overcapacity but a change toward extreme overcapacity in just 2015.

While economists continue to search the now-warmed October skies for temperature and atmospheric conditions, the Chinese are already pointing to the primary discrepancy. If Chinese capacity investment so sharply slows because of the massive and systemic discounting that is necessary to clear sharply slower production growth as exports continue to contract (that’s four layers of deceleration), then the consistent interpretation is not one that keeps the US on a positive economic track. In fact, that view would also more closely align the US consumer with its global cousins that are certainly strained and battered under the “dollar’s” tremendous weight. A financialized global economy will not long survive a full retreat in its basic finance. That was the signal the “dollar” began to send last summer and it has only been validated continually and globally since then.

Stay In Touch