For everything that has gone wrong over the past year or so, there was and is a benign interpretation to accompany each negative factor. Oil prices were “transitory”, longer run inflation expectations didn’t matter because “professional forecasters” remained steadfastly devoted, and no matter which market has gone highly askew it’s just “normal” worry. All of these nonthreatening rationalizations trace back to the backward nature of economics; getting more so the louder these current contradictions. Because Janet Yellen assures us that tomorrow will be her tomorrow, nothing you see around you now to the contrary can actually matter.

Commentary is thus adjusted by that so current observations are skewed under that perception – a perception that dominates not on merit but credentials alone. This answers a lot of our current woes.

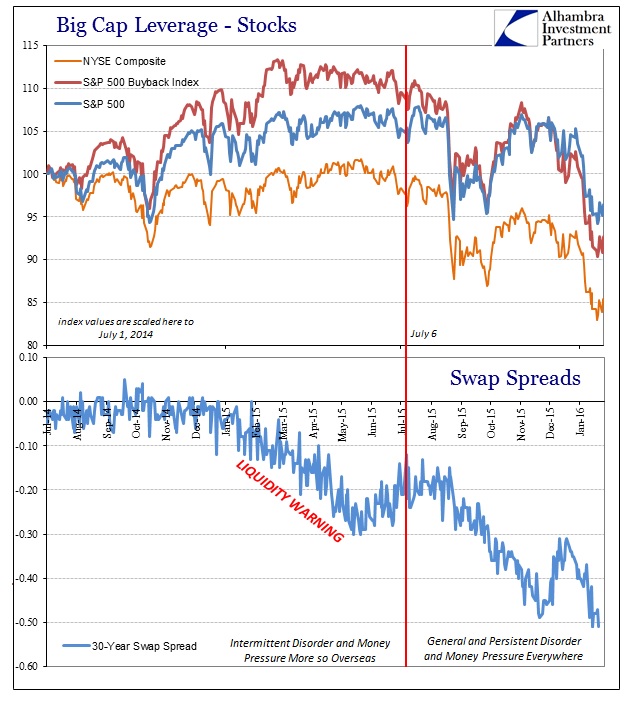

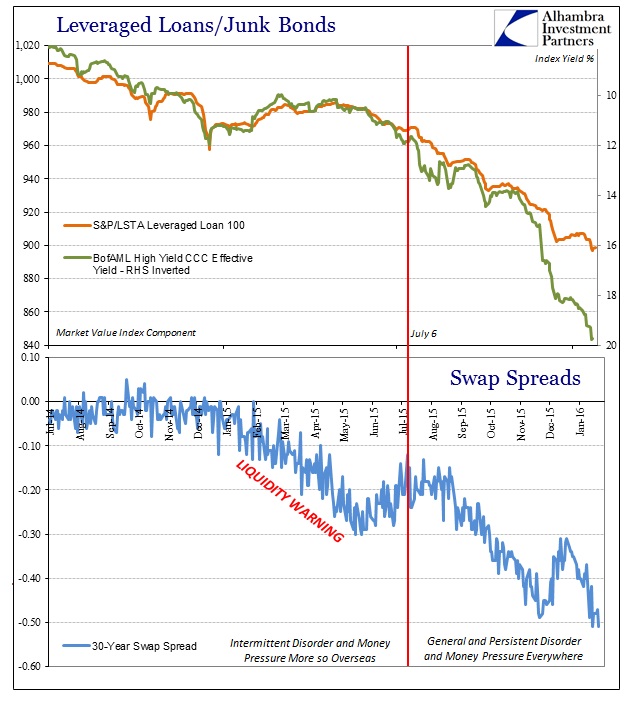

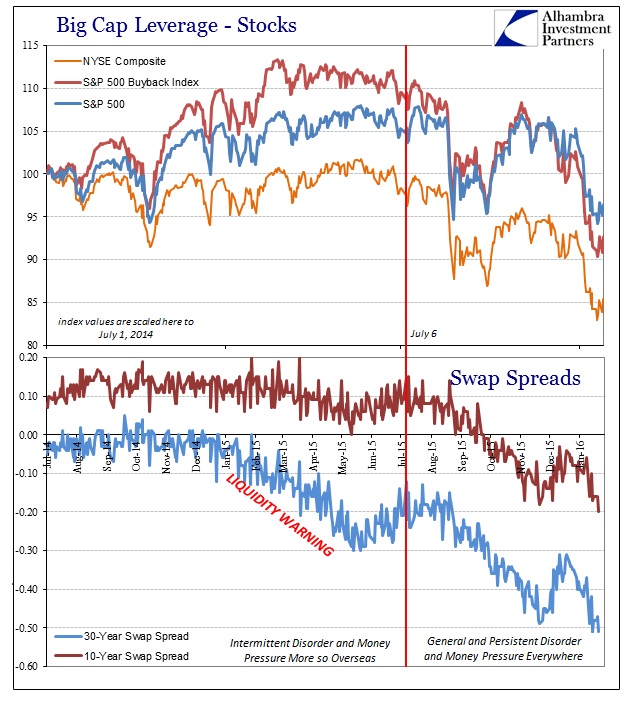

One of those negative factors, increasingly so, was and is swap spreads. As spreads have decompressed all across maturities, itself highly unusual, more and more they turned negative in 2015. A negative swap spread is meaningless in a vitally important market where prices are supposed to hold relevant significance. On its face, a negative swap spread suggests that the market is pricing more risk in UST’s than private derivative counterparties. That is, of course, not what is happening; instead, a negative swap spread only denotes great financial imbalance within the deeper bowels of bank balance sheet construction.

Even recognizing such imbalance, there were no end to the similarly benign excuses as to why swap spreads would signal such grand disarray, but yet still not spoil Yellen’s victory parade. Repeatedly negative spreads were deduced to nothing more than corporate bond issuance and, what would really make Yellen’s version, “selling” of UST’s everywhere:

“There is a rebalancing of holdings by central banks and there is still a massive supply of Treasuries that has no end in sight,” said Ralph Axel, an analyst in New York at Bank of America Corp. “We see recent signs that China is selling and overall all central banks, including the Fed, are no longer the big supporters of Treasuries as they had been in recent years. This is narrowing spreads as it cheapens Treasuries.”

There’s a third component to the negative spreads: Companies are piling into the debt market to lock in low borrowing costs. They frequently swap the issuance from fixed to floating payments, which causes swap spreads to tighten.

As late as November 2015, the Financial Times was still trying to suggest nothing too much amiss about negative spreads:

Analysts at Deutsche Bank say the recent swap spread tightening reflects “tighter macro prudential regulation, higher capital requirements and reduced dealer balance sheet capacity”.

Also playing a role is swapping activity from companies selling debt.

Companies and institutional investors exchange floating rates of interest for fixed rates via a swap contract. When a company sells fixed-rate debt, it can use a swap to offset the payment of a bond coupon and pay a much lower floating rate — three-month Libor.

Interest rates in the UST market are lower, not higher; and corporate issuance has come to a screeching halt. Swap spreads, however, remain negative and compressed, so clearly “something” else is taking place. Removing the bias of the mainstream recovery narrative has the effect of rendering the obvious again obvious.

As is plain on the chart above, stock prices were even biased slightly higher on the left side (much less in the broader NYSE) but as the 30-year spread indicated deepening balance sheet imbalance across the eurodollar system (FICC, which includes banks’ derivative books and dealer activities, are the eurodollar in its last format) even stocks could no longer stand up. Correlation does not prove causation, but simple logic will take care of that: bank balance sheet factors determine liquidity; liquidity determines the foundation for asset markets; the weaker that foundation, the more likely asset prices will falter and further falter in a self-reinforcing manner (through volatility projections).

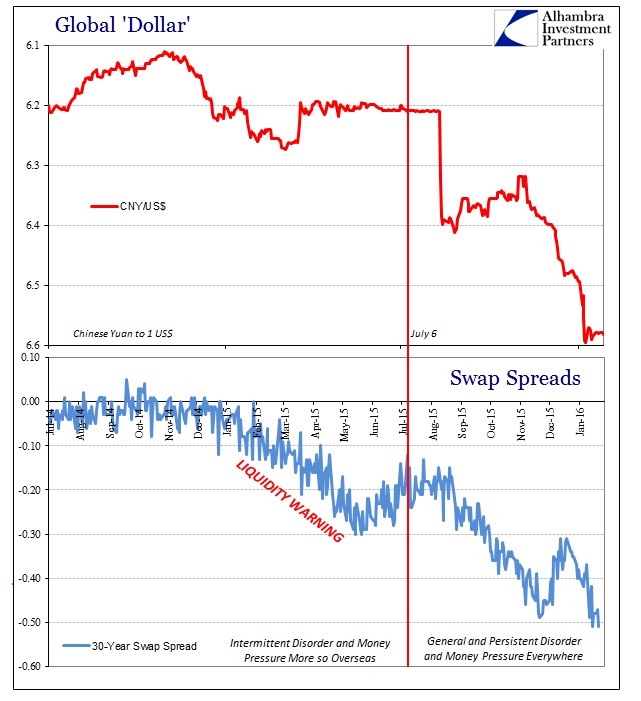

It’s not just stocks, either, which is really the point. Stocks may be the last in the line as other asset classes more directly related to the “dollar” reacted first.

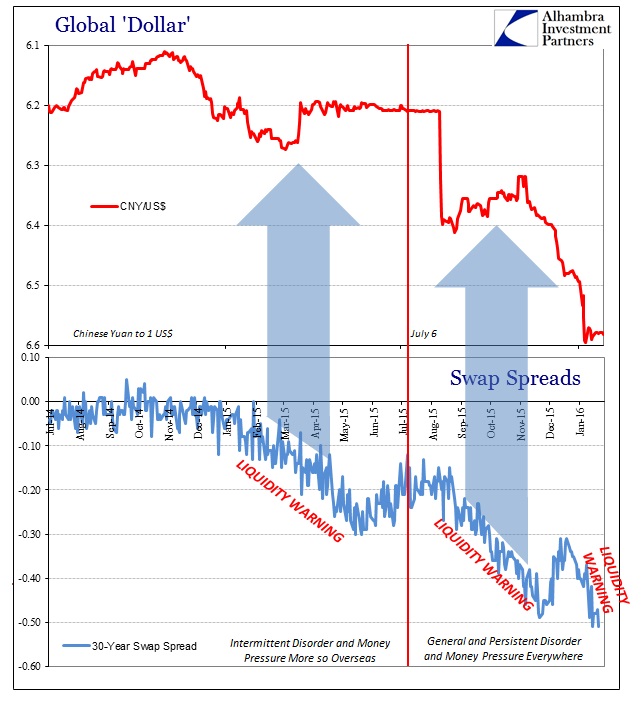

Even the visible pain in China also falls directly in line.

Furthermore, you can actually see the outlines of PBOC effort and desperation in each of the discrete “waves” of balance sheet incapacity suggested by negative swap spreads.

Going back to late April last year, I was searching for the possibility of a second “dollar” wave erupting after the first having been broken up (in some appearances) at the March FOMC meeting. Other markets had become far more optimistic especially as all that might have actually suggested “transitory” would be correct, including inflation expectations in TIPS and 5-year forward rates. But there was growing caution developing elsewhere – particularly swaps markets. Writing then:

Going back to early January, however, as you can see plainly above, disorder has crept back in more durably; the 10-year swap spread has dropped somewhat while the 5-year spread has increased somewhat. That they have remained in this disorderly shape is what is concerning far more than the actual degree to it. Indeed, the “dollar” behavior in 2014-15 is far more asymmetric than during 2007-08, which means that more minor disturbances are producing much fuller and disruptive tendencies across the board.

The direction of the spread collapse is obvious, and thus suggests…that very much contrary to “inflation” breakevens there is and remains dysfunction and illiquidity – there is imbalance somewhere and it is not relenting, a fact that is replicated across credit and funding markets. More troubling, however, is that the shift on March 18 in accepted policy expectations has absolutely no imprint here, which means that this decay is not strictly a matter of what the FOMC might or might not do.

At that point there was a stark choice; accept that there might be growing illiquidity in the most crucial regions of global “dollar” finance or ignore it because the recovery might actually show up when the FOMC says it will. The swap market was in process of rejecting the false dawn of spring 2015, right when everyone was convinced that last year would turn out like 2014 in terms of what would happen past still another overly snowy winter. Further, swap spreads were in no way out of line with other “dollar” indications, including the sudden and suspicious pegging of CNY.

In other words, swap spread irregularity was not an isolated nonconformity as corporate issuance flavor might suggest, but worse than that the increasingly negative and compressing spreads meant suspicious disorder even at that point was hardening and deepening into all the wrong sorts of places – exactly why, by September, I implored not to ignore swap spreads as a warning. That trend, alarmingly, has not changed even as it creeps toward a year later. The results we are just starting to see in more universal fashion around us, and still in money markets (subscription required), are the artifacts of that serious deficiency. They have nothing at all to do with Yellen’s economic outlook except that they reinforce why no one should have bought it in the first place. Only the backward nature of orthodox economics would force such harmful priorities.

Stay In Touch