It wasn’t in any way magnanimous for the FOMC to state clearly what everyone already knew without any need for aid of GDP calculations. The policy statement for its January 2016 meeting included language that mitigated, if not fully than significantly, the continued reliance on labor indications alone. The Fed says the labor market continues to point in the right direction, even if the economy in all the wrong places slowed just as it judged recovery conditions met.

Information received since the Federal Open Market Committee met in December suggests that labor market conditions improved further even as economic growth slowed late last year. Household spending and business fixed investment have been increasing at moderate rates in recent months, and the housing sector has improved further; however, net exports have been soft and inventory investment slowed.

As for inflation, the Committee still will not specify “partly.”

Inflation has continued to run below the Committee’s 2 percent longer-run objective, partly reflecting declines in energy prices and in prices of non-energy imports. Market-based measures of inflation compensation declined further; survey-based measures of longer-term inflation expectations are little changed, on balance, in recent months. [emphasis added]

Yellen’s “professional forecasters” are mostly unwavering, not surprising since they are the same sort of economists that stand upon the BLS’s straight line of a payroll report, but credit market indications of such things are equally if not more so but in the worst way. Inflation forwards and breakevens improved a little since this statement, but remain far too near the worst levels of 2009.

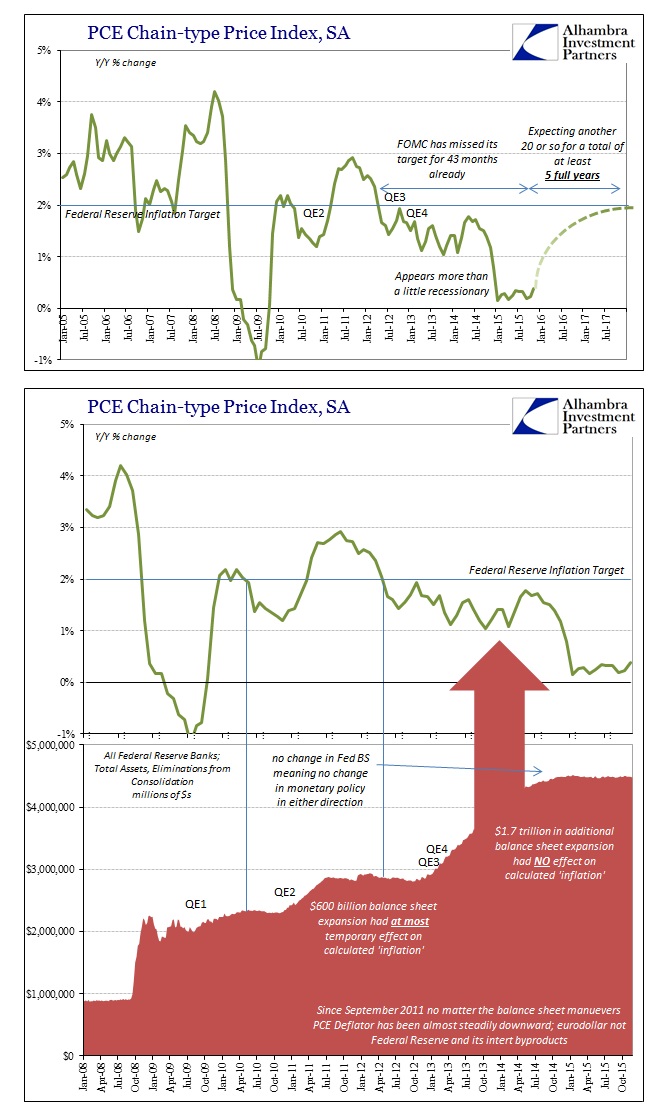

As noted about Japan earlier today, inflation is the whole thing. You don’t have to take my word for it; the FOMC amended its 2012 Statement on Longer-Run Goals and Monetary Policy Strategy in the most curious way.

The inflation rate over the longer run is primarily determined by monetary policy, and hence the Committee has the ability to specify a longer-run goal for inflation. The Committee reaffirms its judgment that inflation at the rate of 2 percent, as measured by the annual change in the price index for personal consumption expenditures, is most consistent over the longer run with the Federal Reserve’s statutory mandate. The Committee would be concerned if inflation were running persistently above or below this objective. [emphasis added]

The highlighted portion above is what the FOMC amended, adding that sentence where it did not appear before. The timing of the amendment and its notation and implication is strange for a monetary policy stance that only a month ago was saying there were no more impediments left to fulfilling both mandates. As should be well-known, inflation in the US has been running far below the 2% objective for over a year, and has remained under the monetary policy target for almost four years running. As the language makes plain at the outset of the quoted paragraph, the FOMC believes monetary policy the major variable in long run inflation.

Is that the coming of negative rates in the US? It is hard to read it any other way which aligns with reality. If inflation, in the sense of the calculated PCE deflator rate, has truly been nonconforming for nearly four years, that easily qualifies easily for the long run. That would mean, in the FOMC’s formulation, that past monetary policy had indeed failed – specifically the QE’s.

I have for a long time believed that Janet Yellen was far less enthusiastic about QE than Ben Bernanke was, particularly the last two in 2012 (I reckon there were four of them, not three). To be consistent with just that statement’s language and intent, then, we have to read it as: the long run inflation target has not been met; monetary policy is responsible for long run inflation, mostly; therefore past monetary policy has failed; the inflation target still must be met to fulfill the mandate; therefore monetary policy is necessary in some different manner.

To be clear, I don’t believe any of that; the FOMC does wholeheartedly. As I wrote today, I think the descent into deeper monetary depravity the countenance of insanity and madness. It doesn’t really matter if there is internal consistency in the seeming logic of it, the whole thing is wrong and disproven outwardly in persistent observation – not the least of which is inflation setting closer to zero than 2% month after month, quarter after quarter, year after year. An unbiased observer might view that as the fact that monetary policy doesn’t really work at all, but the FOMC declares (potentially) yet more necessary as if negative nominal rates are any different than negative real rates (the ephemeral byproducts of QE which aren’t all that different than the inert and idle bank reserves, which are the tangible byproducts of QE).

What we can’t possibly know is whether the FOMC actually means to do it; in other words, is this another “threat” by which rational expectations is meant to kick in and markets are to take this language as if the Committee is serious again? That is the usual pattern by which monetary policy seeks to have its effects; to get markets to do the dirty work without ever having to actually engage in that manner. The problem with that interpretation is that markets already question the Fed’s monetary policy abilities to begin with. That is why inflation expectations are at Great Recession lows rather than QE-inspired obedience.

The fact that the language was inserted at all is, I believe, instructive that there are enormous doubts about the US economy internally that will never be expressed externally. Why else make such a change? If the FOMC simply wished to recognize the obvious, they would not use language that precluded (“persistently below”) any other interpretation but past failure. If they were indeed unconcerned, as they claim to be, certainly that was the message from December’s rate hike RHINO (subscription required), they would have just clarified what “long run” or “persistently” actually meant in that context (though, that would have required the absurdity of claiming 3.75 years was “transitory”); or that they viewed inflation “symmetry”, the term of monetary philosophy they used that supposedly guided this debate, as not completely relating to the PCE deflator and that “professional forecasters” were an important context in their considerations.

The did something of that sort with labor statistics after Bernanke’s “forward guidance” fiasco. When the unemployment rate fell faster than they anticipated (didn’t matter it was the denominator), they changed their criteria to a “broader” set of labor indicators that allowed for QE to not upset QE’s contradictions. Given the similar nature of what is being proposed, clarifying “long run” or broadening their criteria of “inflation” or “inflation expectations” would have been a much, much less intensive change in language at least as far was what it might be signaling.

It isn’t all that shocking that the Fed may be already thinking greater monetary absurdity since that has really been the strategy all along. If monetary policy determines long run inflation, then greater absurdity would seem to be demanded by long run inflation rejecting “less” absurd monetary policy. Yet, the problem is easily absorbed and explained when faced at a slightly different angle; if monetary absurdity is proposed to get at stubborn long run inflation, and monetary absurdity is itself greater and greater manipulation of money, killing it, essentially, it seems we have an easy answer. You don’t get inflation by killing money; you get the opposite. The same set of circumstances are true where central banks don’t really have much impact at all, and instead the monetary system itself apart from central banks is imploding on its own.

That last explanation would even conform to the long run strategy statement of the FOMC; inflation is the result of monetary policy, but monetary policy determined not by the Fed or other central banks rather the banking system itself as expressed by the eurodollar. Economists don’t accept those terms, still believing the central bank is the “printing press” (despite a $4 trillion balance sheet that did nothing) meaning that we can expect only more absurdity and insanity until they are stopped. This policy statement and its amendment leave no doubt on the count. What is left to question is how and when. What is increasingly plain, however, is that the recovery didn’t last but one FOMC meeting.

Stay In Touch