Everyone knows the Titanic sank in April 1912, and if they didn’t they were reminded only a few years ago at its centennial. Less well known, for good reason, is the novel Futility, written by Morgan Robertson in 1898 years before Titanic had even been conceived. Robertson’s book includes the largest vessel ever constructed and he even offered it the name “Titan.” And much like the real Titanic, Titan carries only about half the lifeboats necessary for all the souls onboard and even strikes an iceberg in the Atlantic closing in on Newfoundland.

The physical descriptions of the ship in the novel were eerily close to what Titanic would eventually become; including a capacity for 3,000 passengers and crew, the configuration of the masts and even the propellers. To some, Robertson was a visionary if not a prophet. The legend survives to this day because of those similarities.

It is not well-known beyond the committed because the similarities end there. And even the seeming connections are not all that fantastic to begin with; in 1898 large ships were attaining that configuration and size, Robertson merely imagined what the next steps might be. Further, the route through the North Atlantic was just common and icebergs a quite familiar hazard especially at night (both Titan and Titanic met their fate around midnight).

Thinking the novel some kind of wizardry on the part of Morgan Robertson is an example of the Texas Sharpshooter fallacy. In this specific case, observation has proved that view correct as Robertson does not ever again appear in the same visionary capacity.

The name of the fallacy is reportedly traced to epidemiologist Dr. Seymour Grufferman in debunking cancer clusters. There are various versions of the story, but one of the earliest appeared in a newspaper in Arizona in October 1982:

I once read a story of an army sharpshooter who visited a small town. He was amazed to find targets drawn on trees, walls, fences and barns. Even more fascinating was the fact that each target had a bullet hole in the exact center of its bull’s eye.

Inquiring about this, he had the honor of meeting the remarkable marksman. “I’ve never seen anything like this in my entire career,” said the Army man. “It’s incredible!

How did you do it?”

“Easy as pie,” replied the local rifleman. “I shoot first and draw the circles afterwards.”

Other versions, applied with Texas as the location, tell of some unknown gunman spraying the side of a barn with shotgun blasts and then drawing a bull’s eye around the greatest cluster, declaring himself a sharpshooter. In terms of statistics or even just scientific observation, the idea is the observer only taking account those data points that “fit” a predetermined narrative while ignoring or discarding all the misses (usually as “random”).

Janet Yellen this morning testified before Congress with her best shotgun:

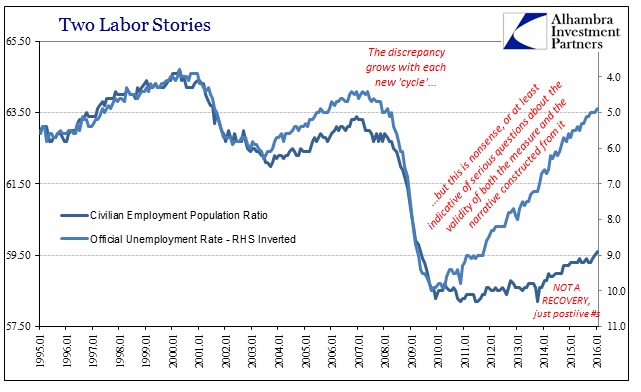

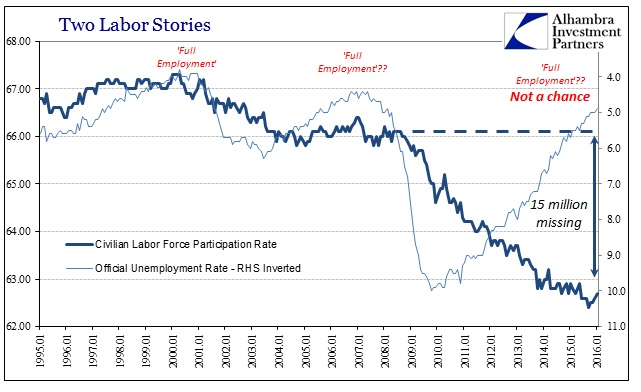

Still, Yellen underscored strength in other sectors of the economy. The job market has made substantial gains since unemployment peaked at 10 percent in 2010. The jobless rate is now just 4.9 percent, in line with what many economists believe is its lowest sustainable level. The number of discouraged workers and those in part-time jobs who want more hours have dropped, though Yellen said there is room for more improvement.

Here is her shotgun in February 2015 in the same setting:

The unemployment rate now stands at 5.7 percent, down from just over 6 percent last summer and from 10 percent at its peak in late 2009. The average pace of monthly job gains picked up from about 240,000 per month during the first half of last year to 280,000 per month during the second half, and employment rose 260,000 in January. In addition, long-term unemployment has declined substantially, fewer workers are reporting that they can find only part-time work when they would prefer full-time employment, and the pace of quits–often regarded as a barometer of worker confidence in labor market opportunities–has recovered nearly to its pre-recession level.

Commentary surrounding Yellen’s testimony only further confirms the fallacy. From UniCredit economist Harm Bandholz:

In a nutshell: Chair Yellen has, correctly in our view, highlighted the solid fundamentals of the US economy. Accordingly, her baseline outlook for both the economy and monetary policy have [sic] not changed. That said, recent developments in financial markets as well as in the global economy have clouded the picture. In this environment, Fed officials prefer to take a step back and wait. Once the clouds have lifted, the gradual normalization of interest rates will continue.

That was, tellingly, exactly the same view that the FOMC and economists took after the September non-decision – that once the August strains in financial markets abated, the “clouds lifted”, they could get back to the work of normalization. Yet, they have persisted again as has the increasingly recessionary circumstances despite the continued drive of the BLS’s statistics toward and into “full employment.” Unlike the labor statistics, however, the cluster of market data and recessionary indications in other economic accounts is much larger and more internally consistent.

As if to further reinforce that point, exit polls from yesterday’s New Hampshire vote underscored the obvious lack of appreciation for the economy that Yellen keeps talking about; as if the jobs and labor progress in her numbers doesn’t match the popular view of labor out in the real world.

Republican voters expressed deep worries about both the economy (three-quarters were very worried) and the threat of terrorism (6-in-10 very worried)…

Though Democrats voting on Tuesday were less apt to say they felt betrayed by their party or to express anger with the federal government, about three-quarters said they were worried about the economy.

It was the same in Iowa, where jobs were a prevalent concern even though the unemployment rate there (and in New Hampshire) is officially calculated below 4%.

In a parallel poll of Democrats, 35 percent said that jobs and the economy were paramount. Those issues ranked second among Republicans, 27 percent of whom named jobs and the economy as the most important.

It’s a rather curious and curiously bipartisan agreement coming during the “best jobs market in decades.” Further, it isn’t any different than the New Hampshire/Iowa concerns from the last Presidential cycle in 2012, meaning that despite the unemployment rate, jobs and the economy remain entrenched in voters’ minds.

Nearly seven in 10 New Hampshire voters say they were “very worried” about the national economy, almost three times the number saying so four years ago before the financial crisis that tanked the economy. Barely more than one in six say their families are “getting ahead” financially, a slide from 2008.

The comparison to 2008 is devastating to Yellen’s fantasy. In early 2008, only two (and a half) in ten were worried about jobs and the economy – early 2008. That seems to offer yet more evidence that the economy shrunk during the Great Recession leaving the positive numbers in employment statistics just that by comparison. And it further isolates Yellen’s sharpshooting in economic prediction and commentary.

It could very well be that the main body of the public has been altered in their perceptions of the economy and even their behavior in it due to the devastating effects of the Great Recession; not unlike what occurred during and after the Great Depression. Either way, however, that still doesn’t add up to what Yellen believes about the economy as presented by the payroll data (and only the surface or headlines of that report). It certainly hasn’t counted for much if anything over the past year and a half. Economists keep claiming economic recovery fulfilled, and yet it is found nowhere other than the BLS.

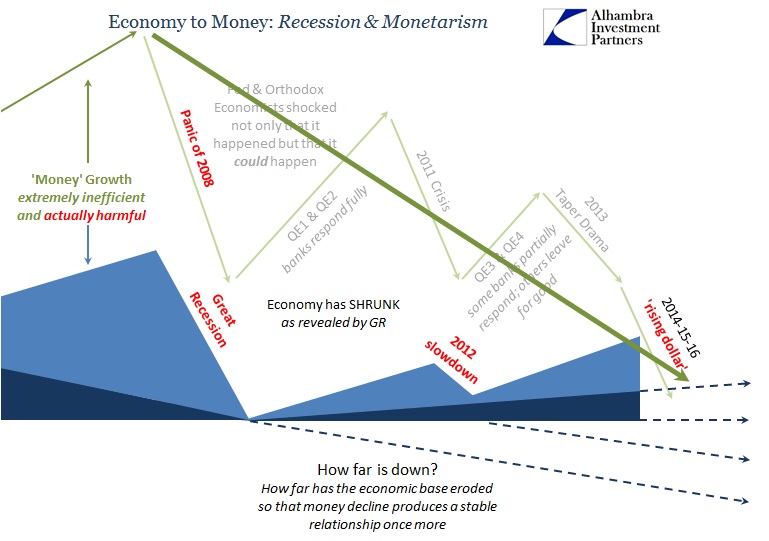

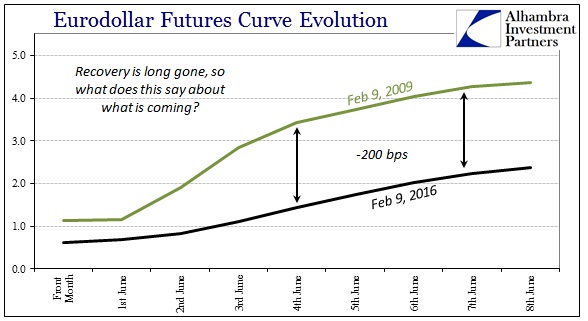

As noted above, it is certainly not the view of funding and credit markets. RHINO has only further raged through credit and money curves. In some respects, the levels of depression in funding (“dollar”) prices and indications are beyond description (below). Worse, the implications (subscription required) are the exact opposite of Yellen’s quarantined labor cheer.

We don’t have to go far for motivation, either. In answering why economists and policymakers would throw out the vast and growing volume of especially market-based contradictions to their preferred labor view, we only have to note that this is an existential question for them. In other words, if the market view prevails, as it has already to a great degree, then that means not only are the economic models all wrong (again) they are wrong for the basic reason that monetary policy just doesn’t work. Not that QE and ZIRP don’t work well, as Bernanke himself has been forced to scale back toward, but that it is then exposed that they don’t work at all.

It’s an issue of somewhat clouded nature in the US for specific reasons of the US. In other places, the imprint of QE is far less debatable. From that perspective the observational determination of the QE experiment is not only that QE doesn’t work at all, QE is actually harmful (redistribution) in a way that helps explain why the US would be heading toward recession without a major “shock.” Monetary interference may produce some jobs, but far less than estimated, leaving the redistribution to only bifurcate into further disastrous attrition.

Voters in Iowa and New Hampshire seem to be motivated by that presence. Worse, for Yellen and monetarism in politics, they are inspired in an increasingly determined backlash against the “Establishment” which includes, on both sides, perceptions of monetary policy as at least unhelpful. Bernie Sanders young voters in particular, see socialism as the acceptable solution to the “best jobs market in decades” fallacy because they have been taught Alan Greenspan, Ben Bernanke and now Janet Yellen, even with her own socialist tendencies, are all part of the failure of capitalism. Even if the young don’t know exactly what it is, the fact they see it as failure is what counts at this point.

It isn’t capitalism, of course, as central bank interference destroys capitalism. That is the point about oil prices. Monetarism is simply another form of statism and soft central planning – and it works in exactly the same depressive tendencies as everywhere else it has been tried. When everyone else starts to see that more clearly as time drags on (and on), then monetary practitioners are forced into smaller and smaller clusters of what might even slightly suggest that there is success in their life’s work. If necessity the mother of invention, desperation might be the father of fallacy.

That leaves media commentary exposed to at least two logical fallacies, one heaped upon the next. Janet Yellen nor the FOMC has particularly distinguished themselves in just these terms for more than a decade, as even Yellen’s own Vice Chairmen once conceded. Yet, they are still given primary consideration for what passes as mainstream commentary because of instead their credentials alone, despite all the circular reasoning that is offered to maintain them. That is the logical fallacy “appeal to authority”; a very human tendency that the Fed and central banks actively seek to cultivate (more actively in just these kinds of conflicting circumstances). But it only leaves the sharpshooter fallacy and appeal to authority, distinct logical breakdowns, as the picture of the recovery and the supposed defense against onrushing recession.

Stay In Touch