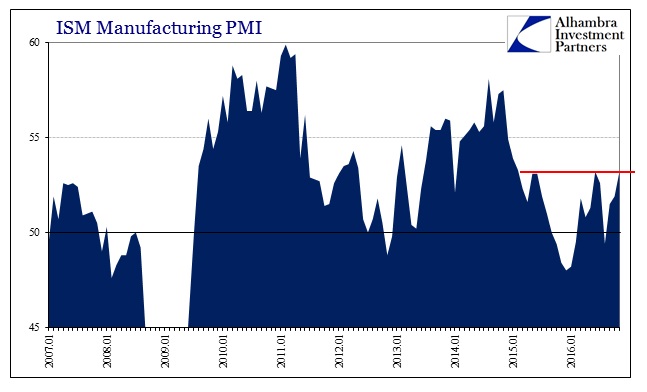

After two months of “unexpected” weakness, the ISM Manufacturing Index rebounded in November. With both September and October below 52, after August’s reading was less than 50, the increase to 53.2 is being welcomed as another sign of distance from the start of the year, if not reflation and growth itself. That belief, however, is and has been misplaced throughout the past few years, as ISM’s PMI has rebounded above 53 on two separate occasions before. In both May and June 2015, the index reached 53.1, only to fall back again as conditions deteriorated into “global turmoil.”

The last headline value at 53.2 was earlier this year in June, as seasonal factors pushed up sentiment as well as economic accounts through spring after an atrocious start to the year. But, as noted above, that springtime optimism did not lead to robust growth as once summer hit the index was back down below 50 again.

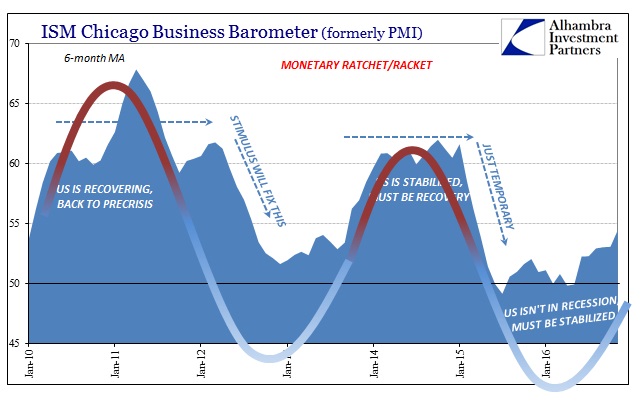

It is this volatility and unevenness that has marked the lack of actual economic progress the past few years. Part of that relates to misconceptions about what is going on, a factor with which the media and the mainstream have been little help, often adding greatly to the confusion. I believe that is what we are observing in these PMI’s even among the purchasing managers who make up the sentiment indicators, as they are or have been very positive one month only to take it back the very next.

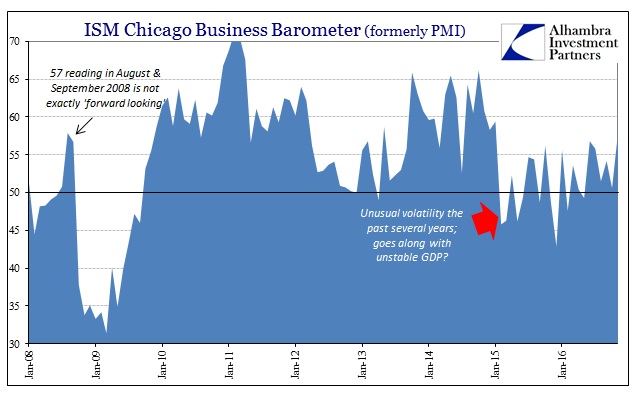

The best example of this volatility of confusion is the ISM’s Chicago Business Barometer. Like the national manufacturing PMI, the Chicago BB rebounded “sharply” in November, up 7 points just last month to rise from 50.6, uncomfortably close to the 50 line again, to 57.6. Since last December, that is the fourth time the index has surged by at least 6 points in a single month; January 2016 +12.7; March 2016 +6; June 2016 +7.5; November 2016 +7.

If you were to view the Chicago BB by just those big jumps, you might begin to suspect remarkable and significant improvement for the manufacturing sector in and around Chicago. But those big positives have been undone by almost perfectly proportional negative months. The result has been a confusing gyration back and forth where overall the progress has been rather minimal.

Both of these ISM PMI’s seem to be estimating the same economy playing out as it has twice before. However you want to describe them, on average the volatile month-to-month changes don’t add up to much more than relief about the possibility of the worst cases being put behind. In 2016, the further the distance from the start of the year, the more relief expressed about weakness not getting weaker. This process is playing out in mini-cycles, or what I think are cycles within what is not a cycle, the depression.

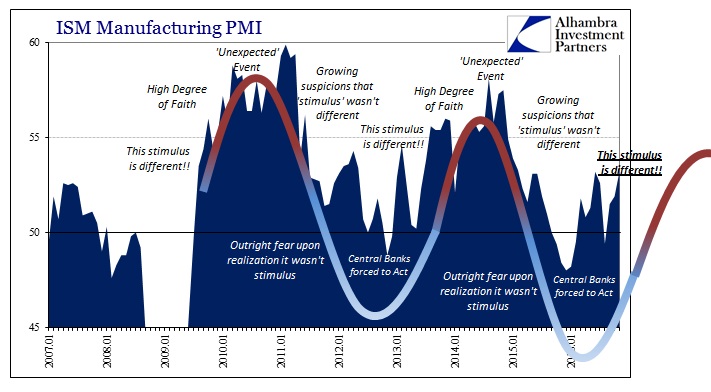

A lot of the positive sentiment in between these monetary events is generated by hopes that central banks will do something different and therefore produce different results. In the first upswing to 2011, it was the introduction and then repeat of QE in the US (as well as other “stimulus” overseas). When that didn’t work, in late 2012 QE3 was introduced as different from either of the first two as being a faster rate of balance sheet expansion as well as one that was supposed to be open-ended.

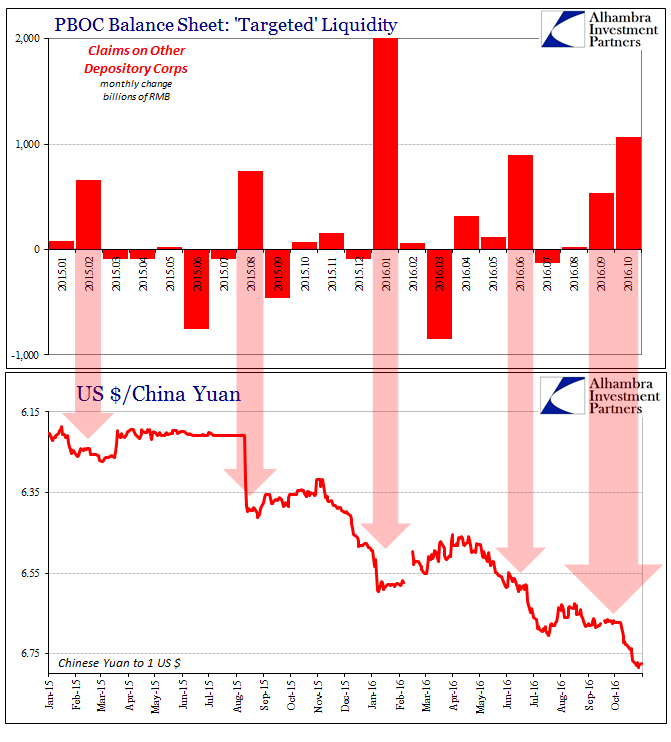

In 2016, what is “different” this time is much less clear, though there have already been some actions already taken elsewhere around the world that could be taken as different. Though the Fed in the US remains convinced that there is nothing for it to do, the Japanese have already experimented with other means, and, as noted yesterday, the Chinese have been more proactive (where they can) about managing their own monetary conditions as they relate to the “dollar.” I have little doubt that is why industrial commodities, in particular, have rebounded this year vs. their pounding last year, and that has certainly contributed to relatively better sentiment and sentiment indices since this year’s start.

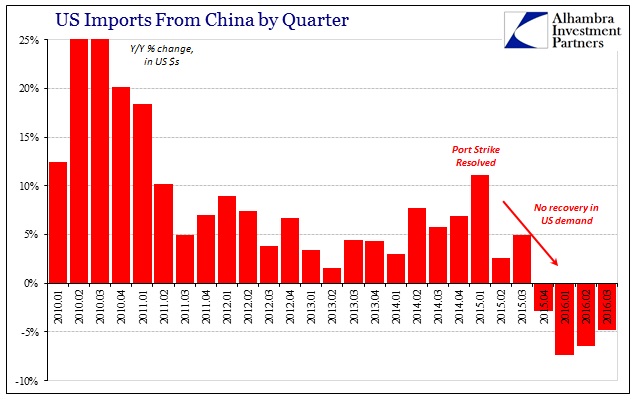

But, as discussed yesterday, nothing the Chinese or Japanese have done is actually different nor have they produced meaningfully different results in terms of economic conditions as well as monetary. Perhaps nothing illustrates that point better than US imports from China, or US imports overall, where, despite a lot more positive feeling about US “demand”, it remains a big problem for China and the global economy.

This is the same economy as the past two years of the “rising dollar”, one that at best isn’t at this moment getting worse. But it surely isn’t, on the other hand, actually getting better, either…

To certain markets, none of this will matter because it’s the old way and the old failed economy that not so long ago most people were extremely reluctant to call it failed. There are, many believe, new things coming that will make all of this go away, just don’t ask anyone for specifics about how that might be.

Despite somewhat better sentiment numbers overall, the volatility that they have taken to achieve such small progress is more significant as it shows the old, weak, troublesome economy remains. Hope springs eternal; actual growth is another matter.

Stay In Touch