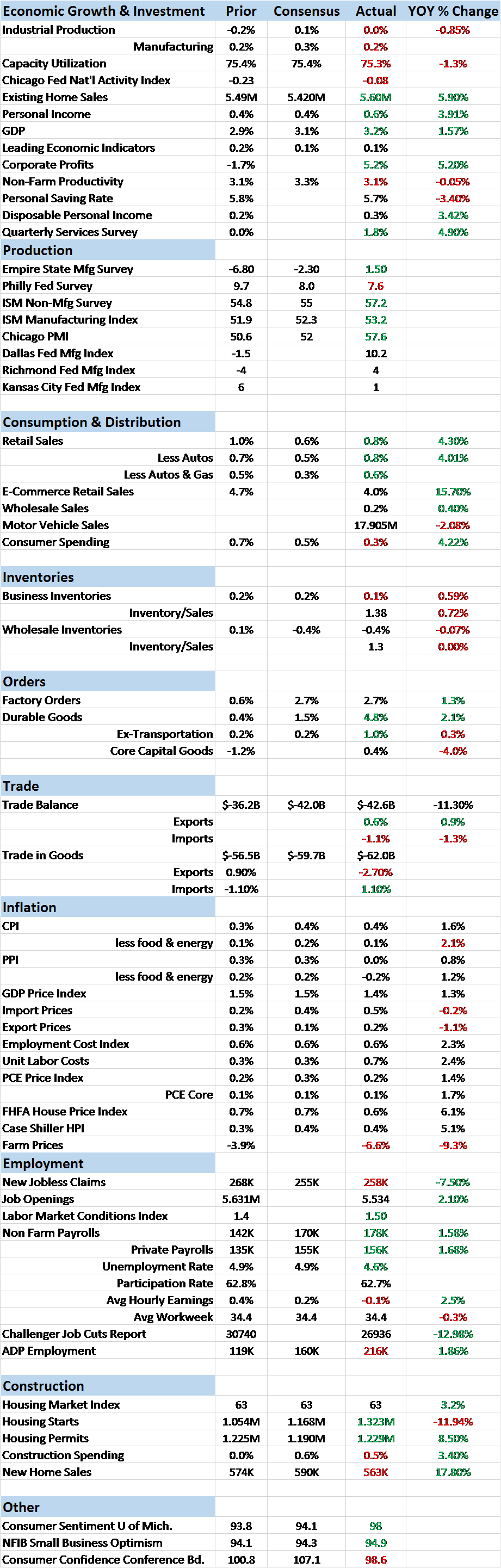

Economic Reports Scorecard

The incoming economic data has improved since the last update with a plethora of reports coming in better than expected. This is the longest run of better than expected data we’ve had in some time and encompasses a wide variety of indicators. Most surprising I think is that we are seeing a bit of an upturn in manufacturing activity. It isn’t much and much of it is anecdotal but there has been a definite improvement. All the regional Fed manufacturing surveys are positive, the ISM report was better than expected and factory orders improved. Wholesale sales also rose more than expected while inventories fell reducing the inventory/sales ratio – although that metric is still quite high compared to recent history.

Employment continues to be a bright spot with jobless claims still tracking at 1970s levels, JOLTS showing a rise in job openings and the Labor Market Conditions Index back in positive territory. But let’s not get too exuberant; there are still big problems with this labor market. The drop in the unemployment rate was – again – a result of a falling participation rate. The JOLTS report did see a rise in openings but the year over year hiring rate is down. Manufacturing employment was down again in the official employment report along with average hourly earnings while the average work week is stuck at 34.4 hours. Headline jobs are still positive but the rate of improvement, which was already pretty anemic, is slowing. The unemployment rate, at 4.6%, doesn’t even come close to providing a complete picture.

The short term upturn in the economic data is just that so far – a short term improvement. The changes we’ve seen in our market indicators, as I said in the last update right after the election, are pretty mild so far. The biggest changes have been in consumer attitudes as both consumer confidence and sentiment have improved pretty dramatically. I would caution though that those metrics are mere wind vanes and can change rapidly – they are always best right before recession and so offer little guidance as to the future.

That rise in consumer sentiment isn’t translating much – yet – to real world consumption. Auto sales are certainly good at a 17 million SAAR but the fact is that auto sales appear to have peaked for this cycle, actually down about 2% year over year. Personal consumption was also among the few disappointing reports, although still a positive number. We’re entering the biggest consumption period of the year though so we’ll see how Christmas spending goes and whether inventories continue to correct.

For now, the US economy is still growing at the anemic pace of the last few years. The third quarter was better than the early part of the year but that is consistent with the pattern we’ve seen the last few years. It hasn’t led to anything more sustainable in prior years and I see no reason right now to believe that is about to change. Year over year growth is still around 1.5% and this little burst of better than expected data isn’t going to change that much. I am encouraged by some of the potential changes to economic policy under the new administration but it is a long way from campaign rhetoric to actual legislation. And there are plenty of areas where I disagree with the new administration, especially when it comes to trade. For now the stock market seems to be assuming that that tough trade rhetoric is just a negotiating tactic. Maybe it is – I hope it is – but for it to be effective the other side has to take your threats seriously. What will the Trump administration do if their bluff is called?

While one shouldn’t get overly excited by the recent uptick in growth expectations one has to acknowledge the change too. The change in sentiment is palpable and combined with the nascent uptick in growth could produce something more sustainable than the minor cyclical moves we’ve seen the past few years. It is also important I think to consider the degree to which changes in the market have an impact on the real economy rather than the other way around. A steeper yield curve has a real world impact no matter the cause. Narrower credit spreads can induce activity that wouldn’t happen at a wider spread. Higher real interest rates have an impact on savings and investment. So, these initial market moves, that are being credited to anticipation of new economic policies, may influence the effectiveness – or perceived effectiveness – of those policies. In other words, the fact that the market thinks these new policies will be effective has an impact on whether they actually are.

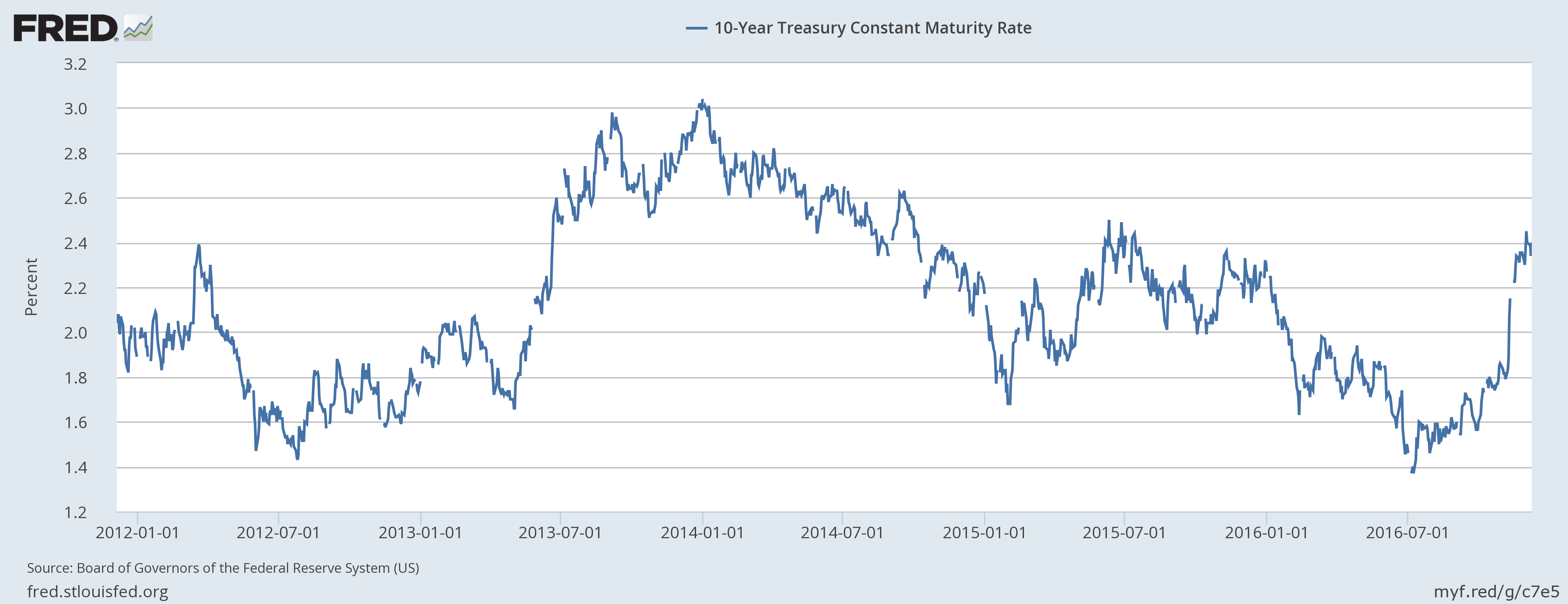

But, again, let’s not get carried away just yet. The changes in the market are so far rather minor even if they seem dramatic. Yes, bonds have sold off but calling the end of the long bond bull market is probably premature. 10 year yields are all the way back to where they were…..at the beginning of the year:

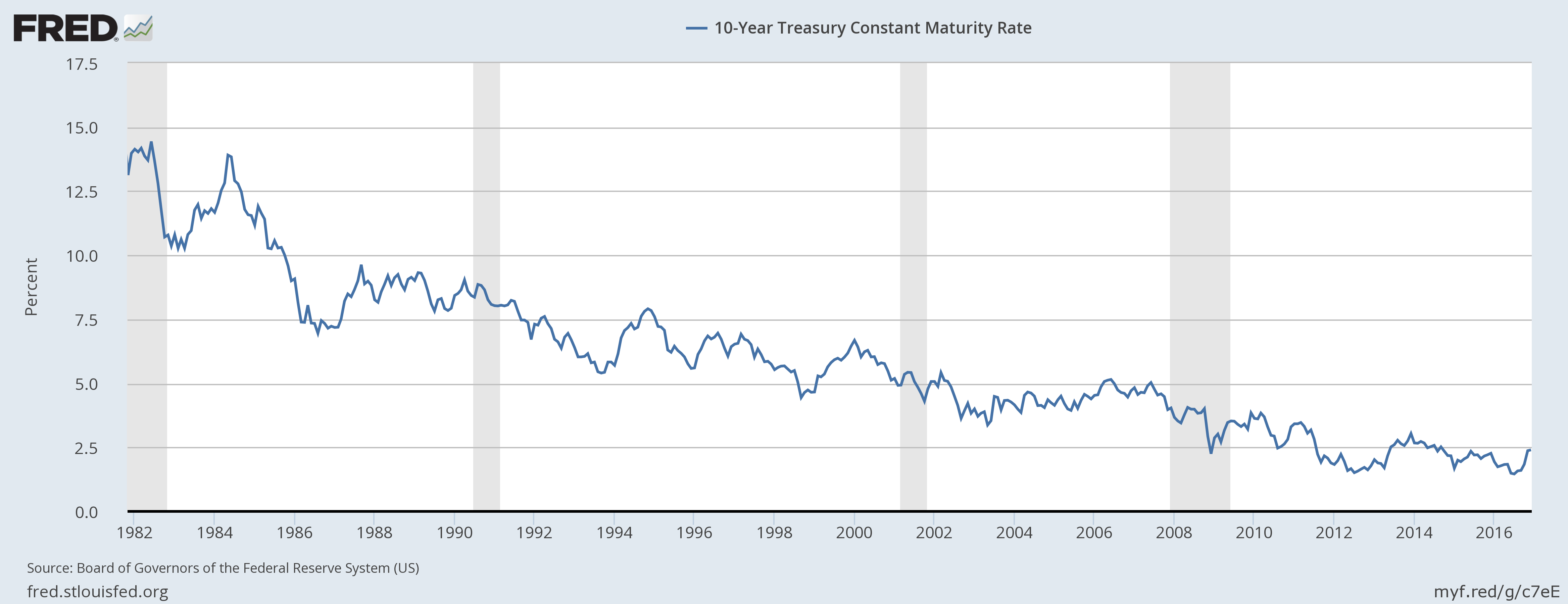

The long term downtrend in yields is intact:

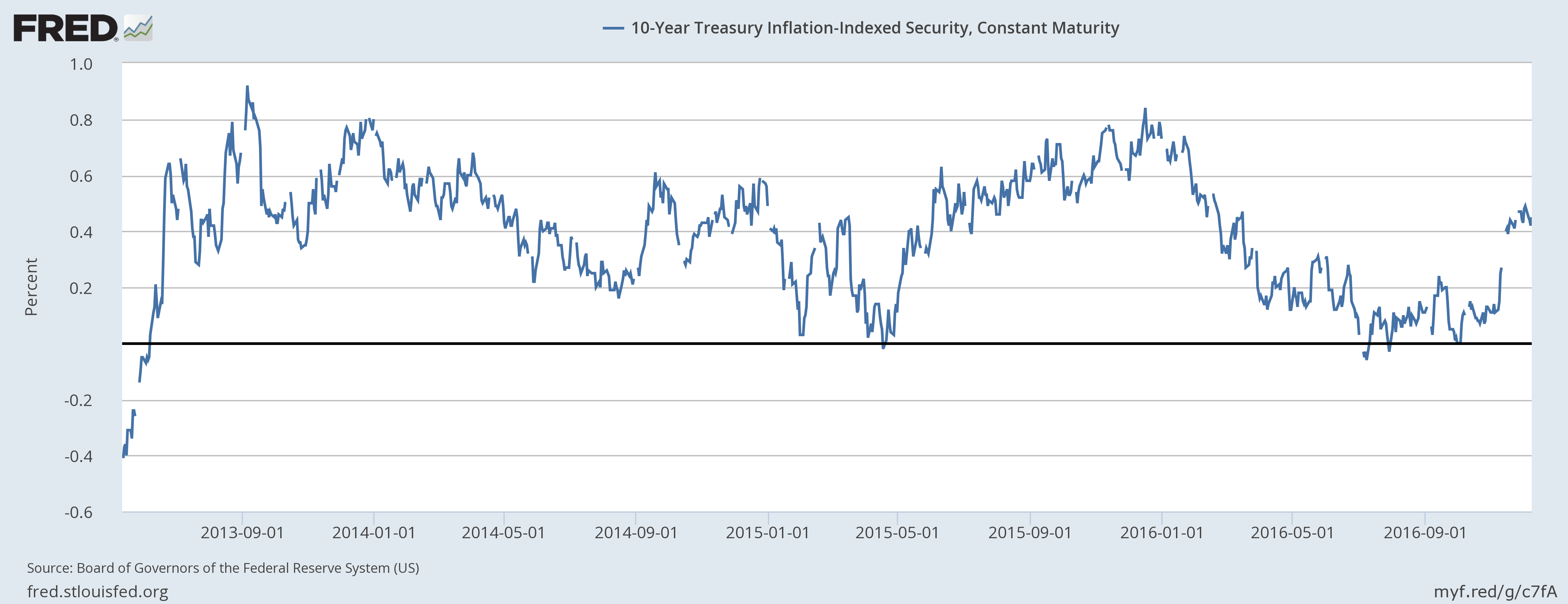

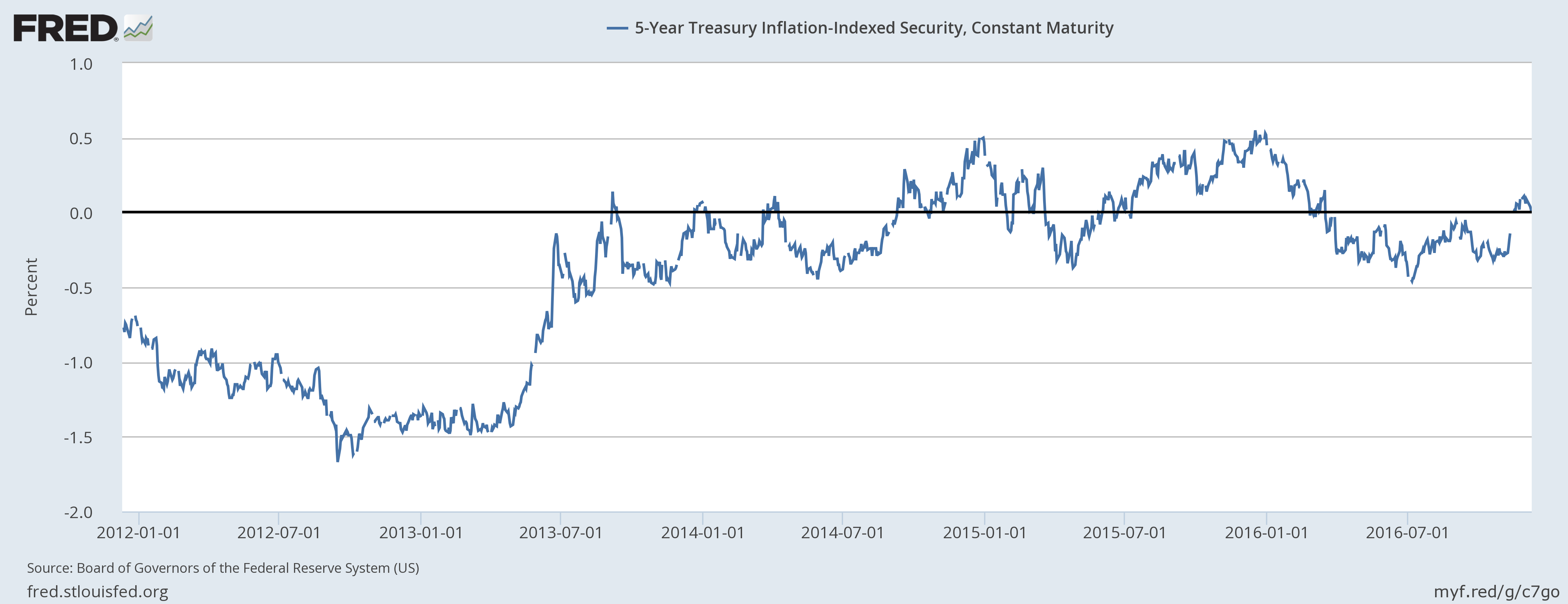

And 10 year TIPS rates – real interest rates – are still down on the year. Real growth expectations are still pretty anemic with the 5 year TIPS yield back to zero:

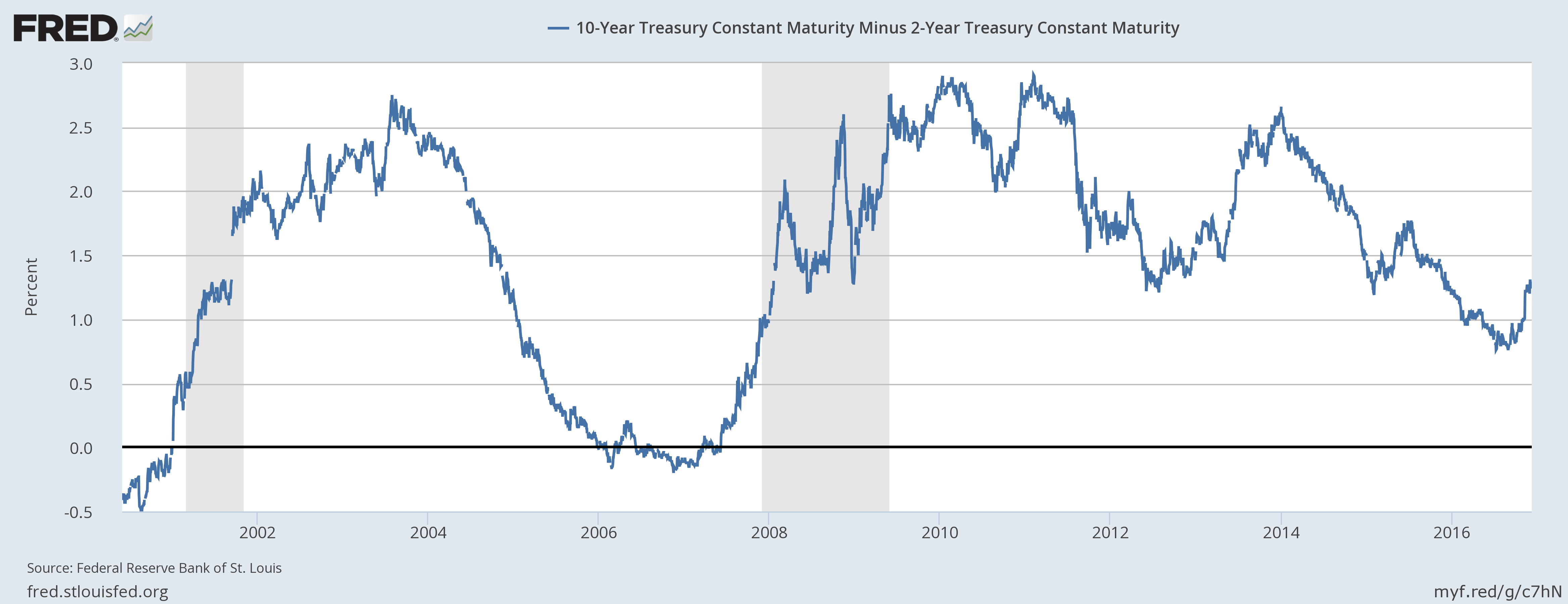

The yield curve has steepened by 27 basis points since the election with long rates rising faster than short rates. That isn’t called a bear steepener because it is a good thing.

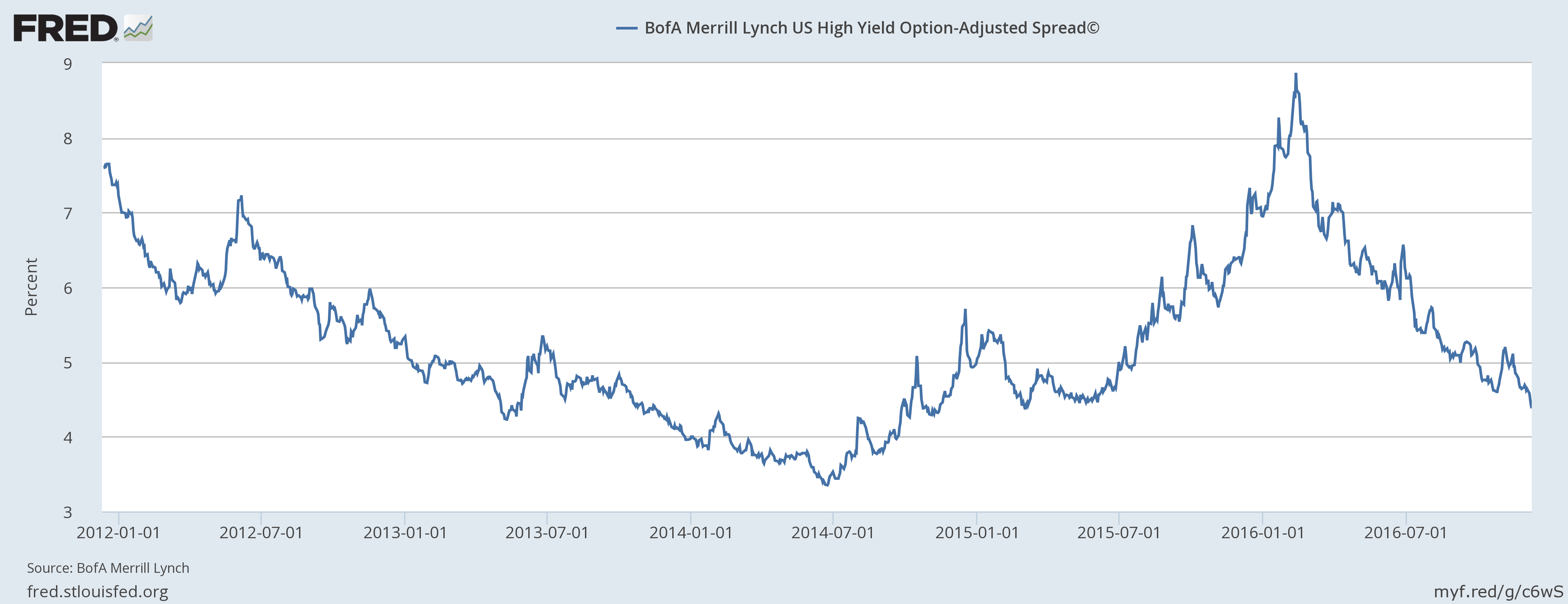

Credit spreads continue to narrow as energy credits continue to improve. I do wonder how far this can go if oil prices don’t keep rising but for now it seems obvious that investors are willing to take that risk.

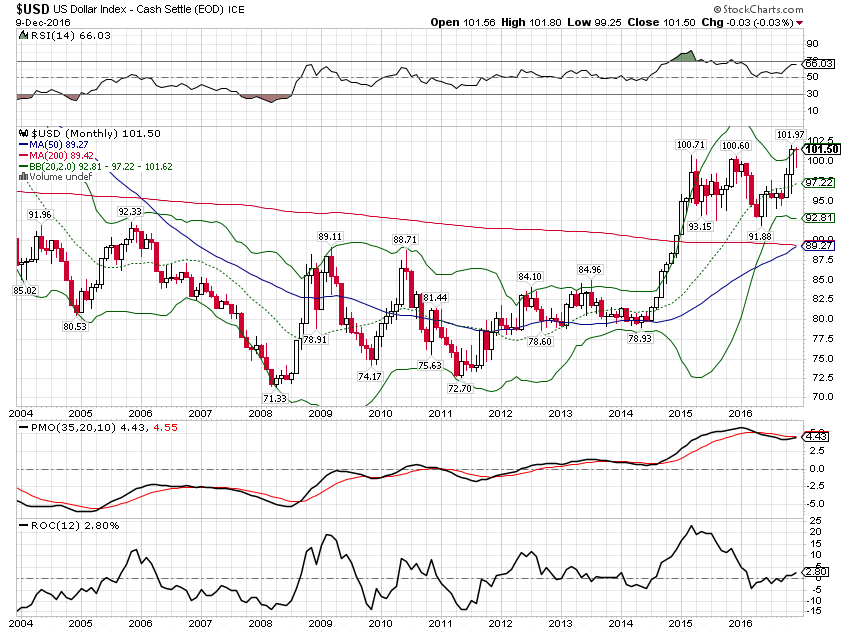

The dollar index is near its recent highs but seems to be having trouble building on the breakout. That might be because everyone and his brother is already bullish. The futures market shows a wide disparity between speculators – who are overwhelmingly long – and commercial hedgers – who are overwhelmingly short. History says follow the commercials so it won’t be surprising if the dollar backs off here.

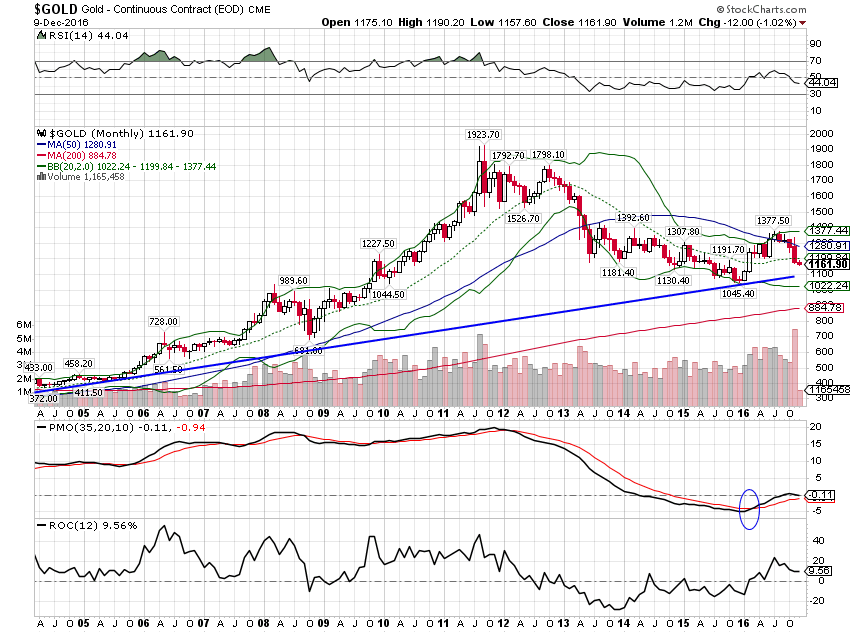

Gold has fallen slightly since the last update but long term momentum is still positive. When the dollar peaks, gold will bottom. Maybe soon but for now weak gold is a positive indication for growth.

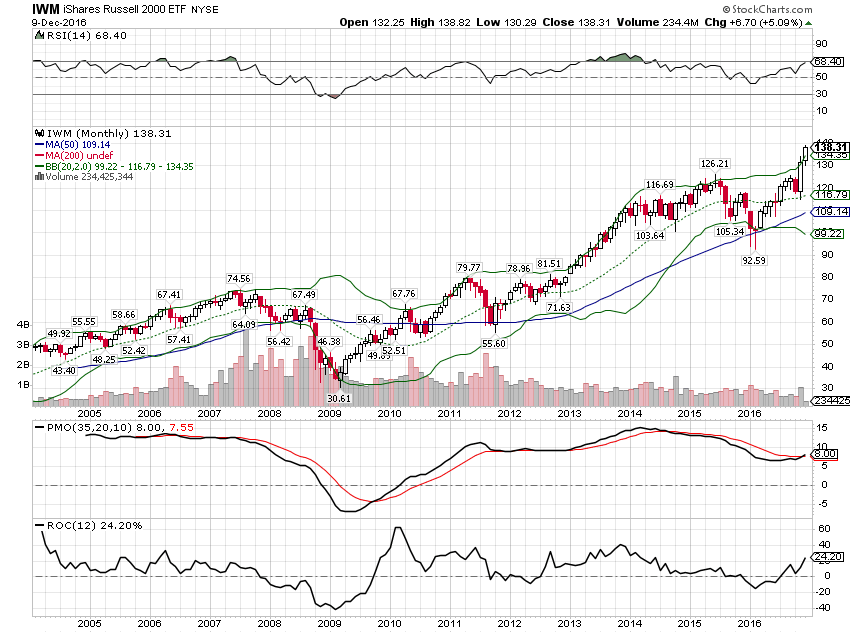

Stocks are where the action is though, especially domestically oriented small caps. The Russell 2000 is making new highs and long term momentum has turned positive intra-month. That may or may not hold until the end of the month but I wanted to point this out because it seems the only place the market is acknowledging Trump’s anti-trade rhetoric. Is it possible that the new administration could restrict trade in such a way that smaller companies are not affected or are affected only positively? The answer to that question, despite the big move in small caps, is an emphatic NO.

Immediately after the election and again in the last Bi-Weekly Economic Review, I warned that we needed more information to make informed judgments about the economic policies of the Trump administration. That still hasn’t changed despite the announcement of a few cabinet members. Growth and inflation expectations have risen since the election but they were already rising. We’re in the midst of a growth rate upturn and there is the added dose of optimism about the change in economic policy. That could – and I really must emphasize COULD – create an environment that raises growth more sustainably. But that optimism could also be misplaced; again, we don’t know what policy will be. And the growth rate upturn could be just as ephemeral as the others in this cycle. We just don’t know yet. For now, what seems obvious is that most markets have raised growth expectations by a modest amount. Stock markets, on the other hand, seem to be discounting a level of certainty that just doesn’t exist. Trump may have caught an economic tailwind but it isn’t the jetstream.

Click here to sign up for our free weekly e-newsletter.

“Wealth preservation and accumulation through thoughtful investing.”

For information on Alhambra Investment Partners’ money management services and global portfolio approach to capital preservation, Joe Calhoun can be reached at: jyc3@4kb.d43.myftpupload.com or 786-249-3773. You can also book an appointment using our contact form.

This material has been distributed for informational purposes only. It is the opinion of the author and should not be considered as investment advice or a recommendation of any particular security, strategy, or investment product. Investments involve risk and you can lose money. Past investing and economic performance is not indicative of future performance. Alhambra Investment Partners, LLC expressly disclaims all liability in respect to actions taken based on all of the information in this writing. If an investor does not understand the risks associated with certain securities, he/she should seek the advice of an independent adviser.

Stay In Touch