November 2008 was an extremely busy month for authorities in the US. The financial markets had just undergone panic the month before, but rather than dissipate there were lingering indications that all was not yet over. On November 23, 2008, the Treasury Department, the FDIC, and the Federal Reserve issued a joint statement on Citigroup. The first two had agreed to issue protection against losses on $306 billion of various MBS and mortgage loans structures, with the Fed agreeing to a liquidity backstop of “residual risk”, all in exchange for an “investment” in the struggling bank.

Just eleven days before that bailout, Treasury Secretary Hank Paulson had announced that TARP would be repurposed to a general bailout fund rather than the “bad bank” model many in Congress and the public envisioned during the process of its passage. Six days after the highly controversial decision, the Secretary, along with FDIC Chairman Sheila Bair and Federal Reserve Chairman Ben Bernanke, faced Congressional ire expressed in the charge of “bait and switch.” Paulson told angry Members:

When the facts changed and the circumstances changed, we changed the strategy. We didn’t implement a flawed strategy. We implemented a strategy that worked.

Five days later Citi received its salvation. No more institutions would fail after Lehman, but saving individual firms from liquidation is not anywhere close to the same as saving the system from the same tendency. The Fed in particular had become hyper-active from the middle of September 2008 on, but like the Treasury Department it shifted dramatically in early November 2008, too. From the timing and coincidence of both, we can only conclude that all the relevant agencies were in agreement that what was being done before wasn’t working (in other words, stating the obvious).

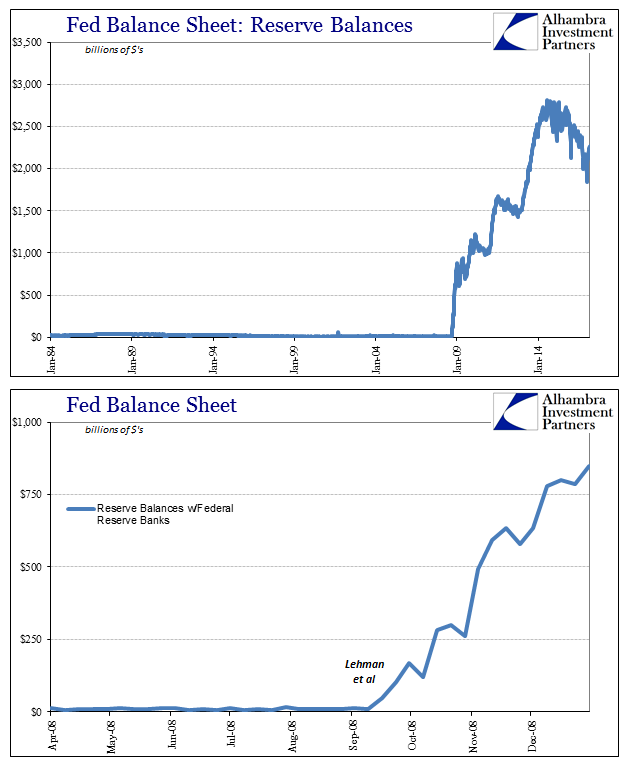

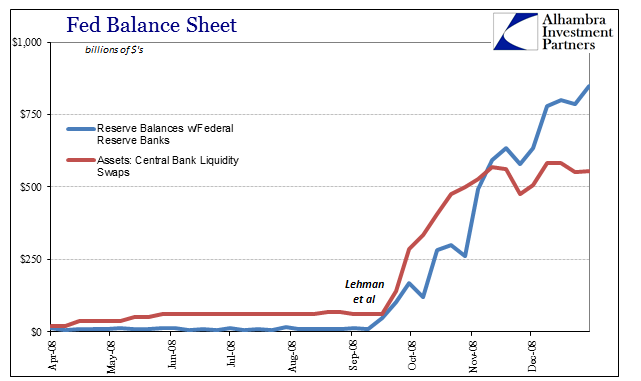

The major change in monetary policy was in how it would “absorb” so much additional “liquidity.” The Fed through various acronymed programs was rapidly expanding its balance sheet, to try to get money into disparate parts of a financial system starved of liquidity capacity. Yet, that condition would only continue even though the Fed was engaged well into hundreds of billions of dollars. The asset side of its balance sheet swelled as it did those things, leaving the level of bank reserves on the other side to do similarly.

The Fed tells us even to this day that the result of so much added reserves was the federal funds rate coming in far below target. The Federal Reserve Bank of New York declared it had:

…encountered difficulty achieving the operating target for the federal funds rate set by the FOMC, because the expansion of the Federal Reserve’s various liquidity facilities has caused a large increase in excess balances. The expansion of excess reserves in turn has placed extraordinary downward pressure on the overnight federal funds rate.

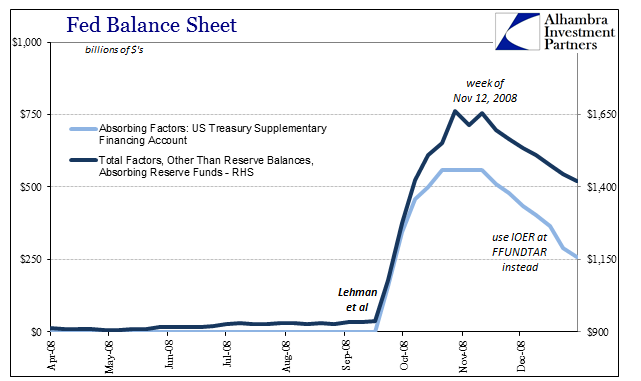

To address this major deficiency, it had before November attempted to “absorb” as many of those reserves as it could. FRBNY was instructed to engage in reverse repos transactions, which are today more familiar in their role within an “exit” strategy (already seemingly at odds with those times). Primarily, however, this absorption technique was to fall on the Supplementary Financing Program (SFP). In the middle of September 2008, the Treasury Department had agreed to sell short-term debt securities and place the funds in a special account with the Federal Reserve. The Fed explained:

When the Treasury increases the balance it holds in this account, the effect is to drain deposits from accounts of depository institutions at the Federal Reserve. In the event, the implementation of the SFP thus helped offset, somewhat, the rapid rise in balances that resulted from the creation and expansion of Federal Reserve liquidity facilities.

There does seem to be a basis for this contention, as the federal funds rate did fall far below target as the balance of excess reserves rose sharply.

But is that causation or mere correlation? The Fed has either implied or, as above, stated outright causation of reserve balances for the irregularity of the federal funds market. This is indeed strange, as it is a blanket contradiction that nobody seems willing to challenge. If the effect of the SFP was to “drain deposits from accounts of depository institutions at the Federal Reserve”, since bank reserves are treated as “base money” another way of saying that is the Fed was, in concert with the Treasury Department, draining base money from the banking system during a monetary panic. Since the federal funds rate was drastically below the target rate supposedly as a result, we can rewrite that statement to say US monetary officials were heavily in action because there was far too much money during a monetary panic.

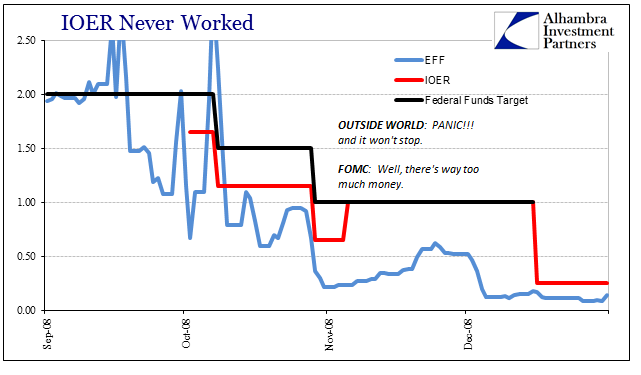

The ineffectiveness of its absorbing techniques had become so severe that by early November 2008 the US central bank as the US Treasury Department decided to change its operative elements. Rather than rely on reverse repos or the SFP the Fed would turn instead to IOER pegged right at the federal funds target. But, as noted last week, that didn’t work (above), either.

We are therefore left challenging the Fed’s conclusions about all of it, starting with the contradiction. In other words, the Fed assumed that the low federal funds rate was a product of its increasing base money in the form of reserves. What if, instead, the low federal funds rate had much less to do with, if not have been unrelated to, the level of reserves (excess or required) at all?

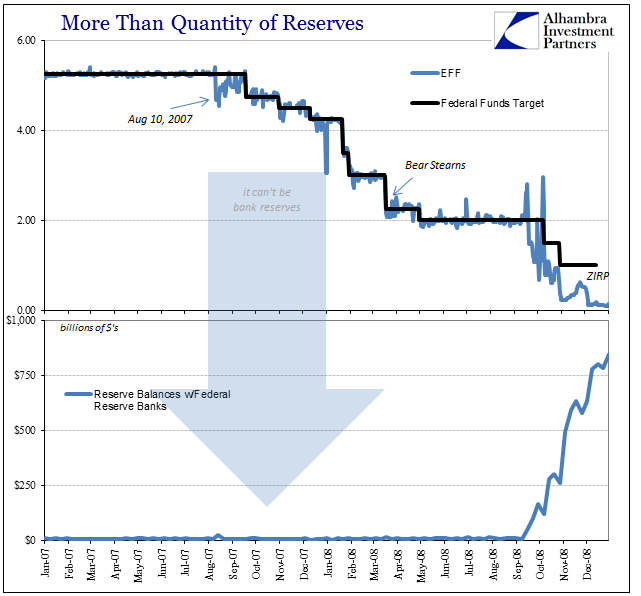

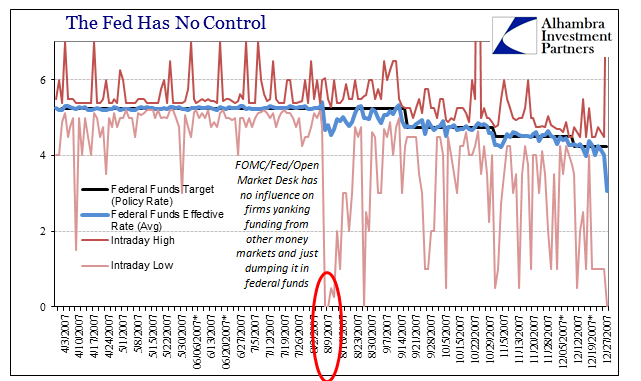

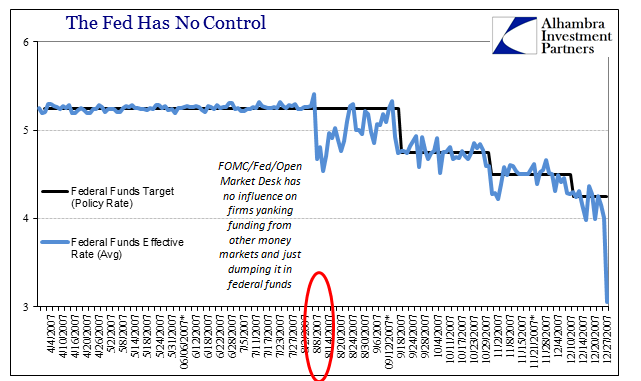

As I point out all far too frequently still, September – December 2008 was not the first period in which the federal funds rate had fallen below target in serious fashion for an extended length of time. The very first instance was August 10, 2007, which in many ways was a complete precursor of all these systemic discrepancies.

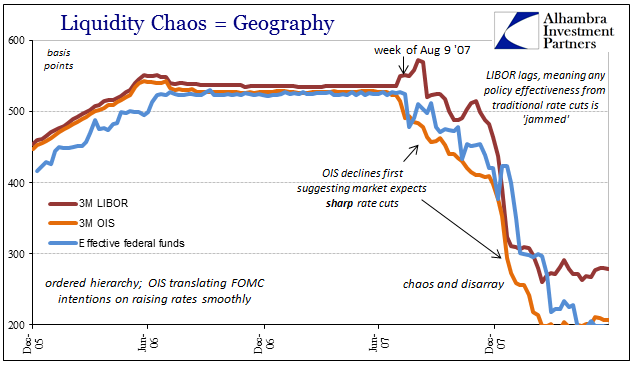

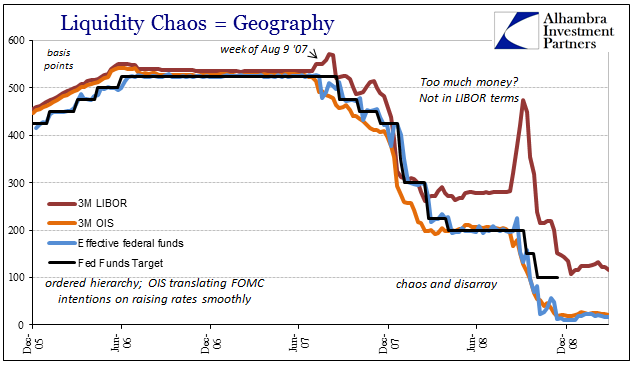

Since it obviously was not the quantity of bank reserves that could have caused this highly irregular circumstance, we are forced in 2007 to look for other ways in which federal funds might be favored over alternate forms of funding arrangements. The primary arbitrage had been between federal funds and LIBOR, meaning domestic US markets versus offshore “dollars.” So where you could in the late summer of 2007 borrow all you wanted in federal funds domestic and pocket a large spread by then lending those dollars in eurodollar markets at various LIBOR points, very few appeared willing to do that.

In fact, this lack of arbitrage only worsened even during the middle of 2008 when relatively calm conditions after Bear Stearns convinced a great many “experts” and all the policymakers that the worst risks were behind rather than still ahead.

In other words, the quantity of bank reserves in the dollar system were irrelevant to the condition where federal funds tended toward shallowness as well as the related and opposite condition of LIBOR illiquidity. The degree to which the federal funds rate would fall and stay below the target is therefore established by the intensity of those liquidity preferences; and in the weeks and months following Lehman, there were innumerable reasons (including the clear lack of monetary competence on the part of any authority) as to why they would intensify as compared to 2007 or any other times. It would seem, then, that “something” big and purposeful is missing from the explanation.

The Fed’s own balance sheet statistics provide a clue as to what it was. In the weeks immediately after Lehman, one of the primary asset side sources to generate the rapid expansion in bank reserves was dollar swaps with foreign central banks.

From this view, we can better understand what the Fed was actually doing even if it didn’t either know it or would ever admit it. It was attempting to drain reserves from the US domestic system first by the SFP and then by IOER while at the same time redistributing them to foreign locations, primarily in Europe and Japan. That is, in fact, what both the federal funds rate below target as well as LIBOR at huge premiums to it says – too much money but only in NYC and not nearly enough in offshore markets where the panic was centered.

It was the banking system that had always provided the means by which redistribution had always taken place (which was captured in far, far more than just federal funds vs. LIBOR). Offshore vs. onshore was a very real divide, only it hadn’t up to August 2007 appeared to be any risk at all. Rather than realize the significance of that fact, established in all sorts of ways, ideology (there is only the dollar with the Fed at its center and bank reserves its base) prevailed and continues to prevail today.

The difference is, of course, that orthodox treatment claims federal funds as a result of the increase in bank reserves which by the whole history of the crisis we know as false; the idea that there was too much money during a panic is as absurd as it sounds. Instead, the level of bank reserves only tells us what the Fed was doing. The correlation between the federal funds rate and that level was mere coincidence, in that liquidity preferences caused market participants to reduce their offshore exposures regardless of the level of bank reserves (at most you can make the argument that the level of reserves increased the intensity of those liquidity preferences, but not that they caused them) and therefore forcing the Fed to do something in response. That the “something” was bank reserves is unsurprising, as is the failure of using that method.

This is an enormously important distinction, one that applies as much today and the rest of the “recovery” period as in 2007 or 2008. There were and are any number of technical factors which would validate this view. Submissions to the RRP, for example, take place between 12:45 pm and 1:15 pm ET and are returned next day between 3:30 pm and 5:15 pm. Federal funds by contrast, can be open to 6:30 pm ET. It is not difficult to imagine situations where financial participants would be worried about late day liquidity (an unexpected margin or collateral call) to where they would eschew RRP (or IOER) paying higher rates in order to keep open all options (paying, essentially, an intraday liquidity premium for federal funds). This is, in fact, exactly the kind of scenario which John Maynard Keynes envisioned when he wrote about liquidity preferences for consumers in The General Theory.

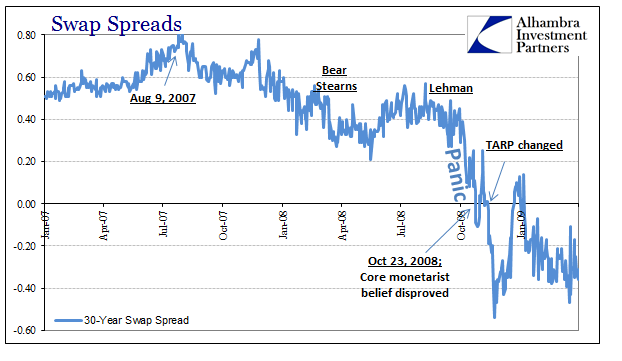

As the hierarchy and potential arbitrage broke down in these forms it also did so in others, including contemporarily swap spreads. The interest rate swap in the 30-year maturity didn’t turn all the way negative until late October 2008, just as it was becoming clear to authorities their initial panic response was itself panicked and ineffective. Where were the arbitrageurs? Governed by the market prices of the UST 30s, somebody should have been furiously writing IRS so as to take the fixed side, but there wasn’t anybody.

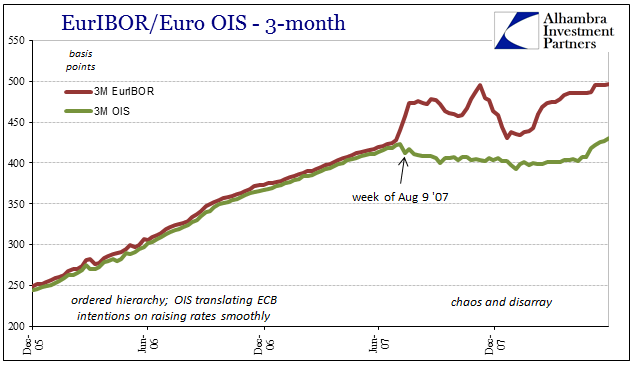

Nor was this ineffectiveness limited to just US dollar conditions, as ruptures of this kind appeared all over Europe and the rest of the world.

All these breakdowns in hierarchy point to a single cause or parameter – bank balance sheets. From that view, bank reserves are just one form of bank liability and not even an important one. Thus, the quantity of bank reserves would be at best a small consideration for establishing global dollar conditions. From this view, a great deal of 2008 as well as thereafter actually makes perfect sense.

Economists, however, continue to hold to the view that bank reserves are base money. Because of that, they can never reconcile what happened in 2008 nor what failed to materialize after it (recovery). Even though it makes no sense to claim that there was too much money during a monetary panic, because the view remains uncritically accepted by the media that adheres to editorial standards of credentials rather than logic we are stuck on Step 1 even ten years after it was fully apparent central banks had no idea what they were doing. That operative condition just rolled on through QE1, 2, 3, and 4, simply proving that still further how bank reserves were never what they were supposed to be.

After having squandered a full decade now, bank reserves remain as firmly in place of orthodox monetary treatment as they were in leading to failure after failure after failure. Because bank reserves are treated inappropriately, economists are left with Baby Boomers and drug addicts to try to explain why the QE’s failed to achieve any recovery. Which is more likely: that trillions upon trillions of currency and money printing all over the world failed to make even the slightest economic dent because especially Americans suddenly grew lazy and addicted (to government welfare as well as heroin), or that monetary authorities just don’t know what they are doing, starting with bank reserves and their role in the global monetary system?

There is a great deal of evidence only for the latter, and not just after August 2007. The quantity of bank reserves only tell us what the Fed is doing; the failure of the economy tells us what banks are doing. Only one of them is actually meaningful.

Stay In Touch