MF Global failed on a trade that would have made it enormously profitable. AIG’s portfolios of “toxic waste” ended up making money – for the Federal Reserve. Bear Stearns and Lehman Brothers were ended like the others by liquidity, not losses. SemGroup was another firm that went into bankruptcy during that period, but one that practically no one has heard of. It failed for largely the same deficiency.

Based in Tulsa, Oklahoma, SemGroup at one time employed 2,000 people in ostensibly the oil distribution business. The company handled 500,000 barrels of crude a day through two pipelines, using its 6.7 million barrels of storage capacity to do what oil companies do. Almost all that capacity was located in Cushing, Oklahoma, today’s dumping ground for energy making up the WTI benchmark.

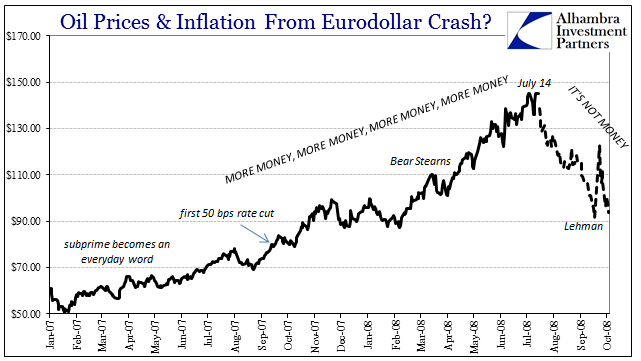

It wasn’t the oil business specifically that ruined SemGroup, but rather oil trading. The company and especially senior management were convinced the oil market was behaving irrationally all throughout 2007 and into early 2008. There was, in their estimation, simply no reason for skyrocketing prices. They bet against it; heavily. The company was short so much oil that at one point corporate headquarters skimmed $54 million from a $120 million loan provided by GE Capital to build a pipeline from Colorado to Cushing to cover margin to maintain their shorts.

As is usually the case, SemGroup just couldn’t withstand the collateral calls on them as WTI, Brent, and every other benchmark seemed headed, unreasonably, to the moon. They made one final, enormous short, one that would pay off to the tune of $5 billion – if only they could make it just two more weeks. The company couldn’t, and on July 22 it was forced into bankruptcy court just days before it would have been proved fabulously correct about the oil market.

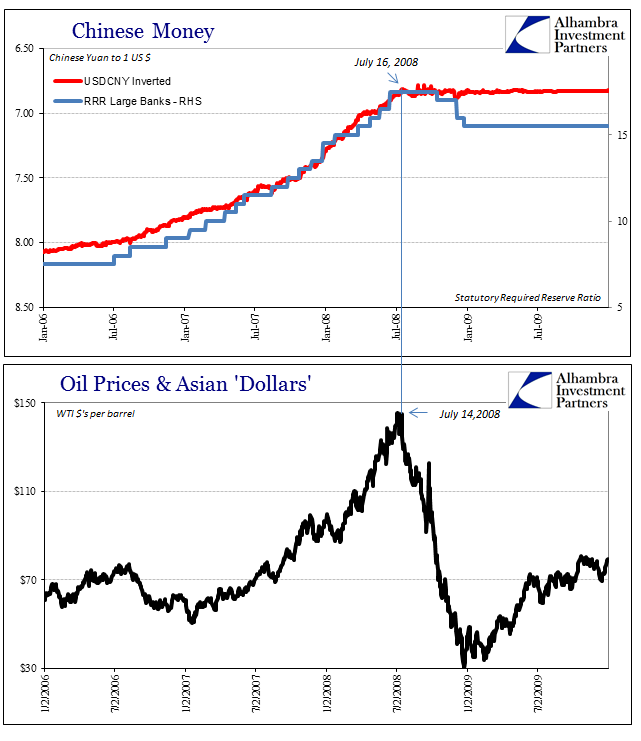

On July 15, 2008, Ben Bernanke testified before the Senate opining, wrongly, as usual, on many topics including oil prices. In his remarks, the Fed Chairman sketched out what sounded like balanced risks; weakness due to housing but with inflation that could keep on rising, as if the two opposing forces would somehow yield a Goldilocks result where the US might avoid recession altogether by nothing more than luck.

However, in light of the persistent escalation of commodity prices in recent quarters, FOMC participants viewed the inflation outlook as unusually uncertain and cited the possibility that commodity prices will continue to rise as an important risk to the inflation forecast. Moreover, the currently high level of inflation, if sustained, might lead the public to revise up its expectations for longer-term inflation. If that were to occur, and those revised expectations were to become embedded in the domestic wage- and price-setting process, we could see an unwelcome rise in actual inflation over the longer term.

The possibility of higher energy prices, tighter credit conditions, and a still-deeper contraction in housing markets all represent significant downside risks to the outlook for growth. At the same time, upside risks to the inflation outlook have intensified lately, as the rising prices of energy and some other commodities have led to a sharp pickup in inflation and some measures of inflation expectations have moved higher.

What some people took away from that testimony was that the Fed was out of the “stimulus” business any more than they were already forced into up until and immediately after Bear Stearns. Whatever slim hope there might have been on the inside of money markets for a further necessary rescue disappeared. The Fed as Bernanke described felt it warranted to worry about weak demand as well as commodity prices going the other way, hoping in the best case that the two would just cancel each other out avoiding recession altogether.

It was a fundamental error, of course, on many accounts, not the least of which was the precarious state of overall economic demand being led downward by a global money system that persisted in a state of malfunction. Bernanke had essentially fooled himself into thinking that things weren’t so bad after all, and the oil market helped him into that position for reasons that SemGroup was right to suspect.

Oil prices rose throughout 2007 and early 2008 on the idea that the Fed would overdo its response. It was widely believed that the central bank could achieve a resolution, and in being careful given the gravity of the situation would err too far on the side of “stimulus.”

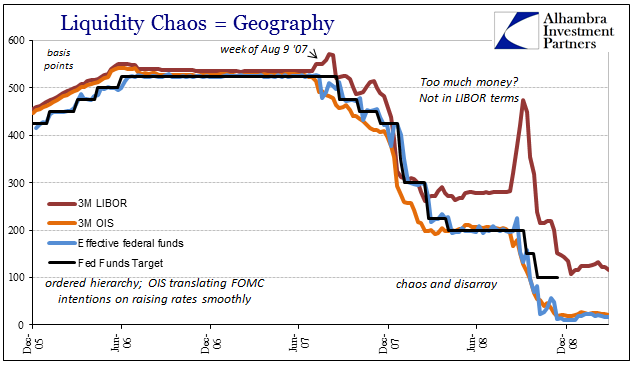

It was predicated on nothing more than the idea that interest rate cuts were liquidity, or at least the impetus for the private system to provide it. Yet, from August 9, 2007, forward, there was in several key prices a constant reminder that this just was not the case. Apart from monetary conditions, it worked out the same way in economic statistics where in the mainstream, nurtured by Bernanke’s optimism as well as oil prices, often severe economic warnings were simply dismissed in favor of optimism for no other reason than this conditioned disbelief.

The oil market was irrational, and in mid-July 2008 it started to become rational again. It was too late for SemGroup, but what is relevant to our current condition is that irrationality in terms of some expectations would continue. In November 2008, for example, a Time Magazine article even blamed the prospect for a bankruptcy liquidation in SemGroup assets for the drastic drop in oil prices.

Clearly, demand for oil didn’t fall that much, but the price of oil isn’t set by demand alone. It’s the product of an extremely volatile mixture of speculation, oil production, weather, government policies, the global economy, the number of miles the average American is driving in any given week and so on.

No, oil demand did fall by that much and would fall much further before it was all over. Economic demand not only cratered, it has yet to recovery almost nine years later, leaving oil investors as well as economic commentary stuck in a conundrum that really isn’t one. Just like the Fed has more recently created a puzzle out of the very low unemployment rate and the lack of wage growth, explanations for oil’s lack of follow-through into full reflation always contain the same color of 2008-type mistakes. It is almost certainly recency bias where now the word “recency” doesn’t really apply. People just can’t (or won’t) believe at these times the world could be stuck in such a bad place.

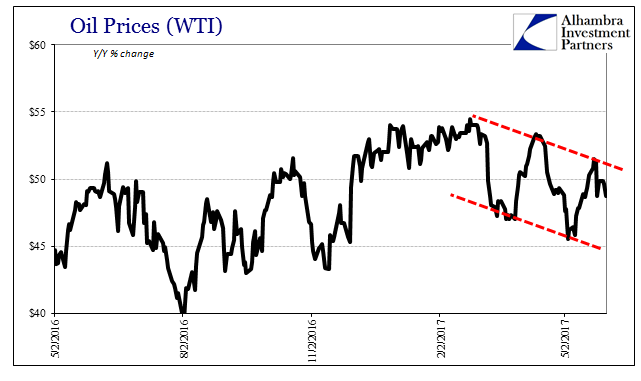

For oil in 2017, it takes on more than just shale or OPEC proportions. Crude prices are it, and have been “it” in both directions. The collapse in late 2014 was a crucial signal about global prospects, which again officials all over the world tried their best to characterize as something it wasn’t (“supply glut”). The same to a lesser extent has happened again, this time over-emphasizing the rise in oil prices from the February 2016 trough as more than it is – or was.

That flirtation, however, has now ended; at least with oil trading in a clear downward pattern going all the way back to late February (lower highs and lower lows).

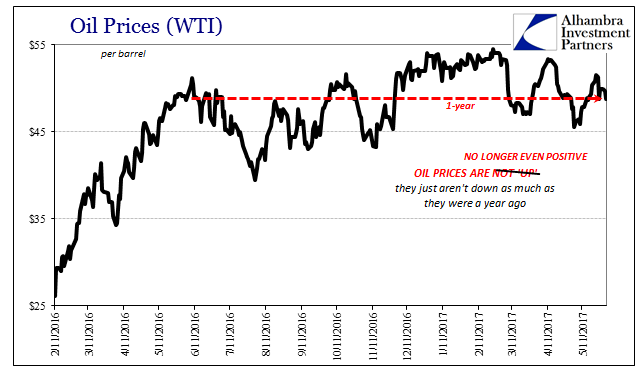

Psychologically, while it aided “reflation” in that oil prices were up on an annual comparison basis, as of now they no longer are. The closing price today is slightly less in WTI than the closing price on May 31, 2016. I have written before that oil prices were not really up, they were merely down less than last year. Now even that first part is no longer technically true. Year-over-year WTI has regained its minus sign.

This is no trivial matter for oil as well as broader matters. The Fed searches for inflation because the unemployment rate is 4.5% when this renewed downward comparison in oil tells us exactly why they won’t find it. As in 2008, they are looking for demand that simply isn’t there.

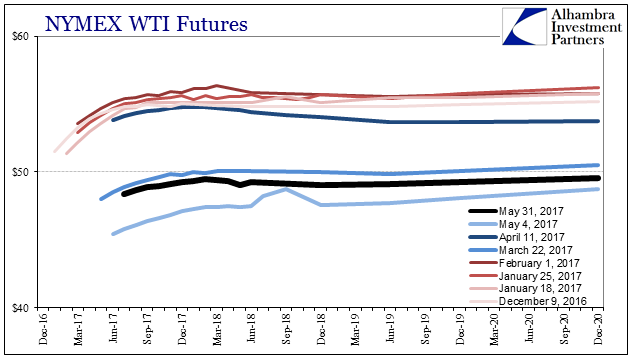

Even the oil futures curve demonstrates as much. Though it remains in slight contango, the curve of late has slipped entirely below $50. That is an enormously pessimistic take on oil fundamentals, and one that is different proportionally than the more-in-contango curve earlier this year under the sentimental upturn of “reflation.”

In truth, unlike the irrationality of oil in early 2008 the trajectory of oil prices has been far more rational this time around. It surged from the bottom, but for a full year now has traded almost perfectly sideways. Like so many other economic accounts, it is conspicuous only for the lack of further momentum when by all historical expectations it and the global economy should be well into unmistakable recovery.

I have to believe that the lack of further price gains have been because unlike nine years ago by now the oil market is totally aware of how powerless the Federal Reserve actually is; and that liquidity, meaning global money, and therefore economic considerations, are completely unlike how all are characterized (glowingly) in the mainstream. After all, the price collapsed at the very moment Janet Yellen and all those economists like her were most sure demand was about to truly take off, and that under QE there was no possible way for further deflation or disinflation caused by dangerous monetary illiquidity.

Bernanke in July 2008 was using a world that didn’t actually exist to make all the wrong moves and say all the wrong things. Somehow, after so much time and proof, a great many people still don’t see it.

Stay In Touch