Some economic and financial conditions leave a yield curve as a more complex affair. Then there are others that are incredibly simple. The UST yield curve is the former, while right now the Chinese Treasury curve is the latter. Even still, the media manages to make it something it isn’t because the world from its perspective is surely improving, and Chinese money is tight for prudent reasons of intentional policy.

A stubborn anomaly in China’s $1.7 trillion government-bond market has worsened, as an odd combination of tight funding conditions and economic pessimism pushed long-dated yields well below returns on one-year bonds, the shortest-dated government debt.

RMB markets are indeed “tightening”, so longer-dated government paper continues to reflect the consequences of that condition, even now to more extreme levels. For an economy already precariously positioned given the events of the last few years, it’s not a trivial concern.

It is not so much inverted as heavily malformed, though in truth that is more pedant semantics than analysis. There is no question as to the first part, just as there isn’t for the second. What seems to be misunderstood is the reasoning for what is taking place at the short end.

What is going on here is nothing short of disorder. There is simply no way to characterize it as a product of intentional monetary policy. To begin with, the PBOC doesn’t operate (ever) with such messy design. China’s central bank has in its history operated with a much more conditioned approach, even when their method and intent have been misguided or mistaken. The appearance of almost open chaos in 2017 brings to mind RMB conditions in the middle of 2013 – the last time the treasury curve inverted.

After having experienced that degree of illiquidity four years ago, Chinese authorities instituted rather quickly additional liquidity channels so as to avoid ever again those circumstances. It’s not as if the PBOC has sat out this last year, either. They have been heavily, hugely engaged using just those means, but to no further avail.

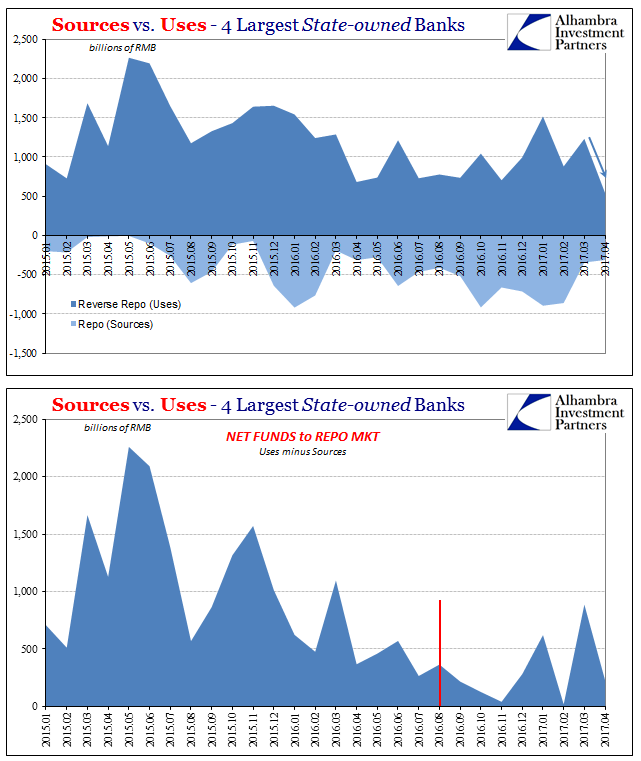

We can argue the intent of policy, but what is unambiguous is why and where. The Big 4 state-owned banks have been left with little spare monetary capacity. It is a topic I have written about before (more than a few times), but still bears repeating.

The effects of the PBOC balance sheet transfer directly to the financial conditions of China’s Big 4 State-owned Banks (SOB). These heavyweights had been over the past few years sourcing more and more RMB from repo markets than they have been redistributing excess RMB back into them. They have done this even though in parallel these banks are using the MLF (and possibly the SLF) to such a huge degree…

Taken together with the MLF activity and other huge accommodations, especially to the Big 4, I don’t see how “tightening” adds up to a policy direction. If anything, we have to take the PBOC at its word, which remains a neutral policy position. Therefore, the accommodation especially through the MLF makes sense as the central bank struggles through excess RMB (and an enormous quantity of it) just to keep to that neutral position. Judging by rates in April, they have yet to achieve that desired outcome.

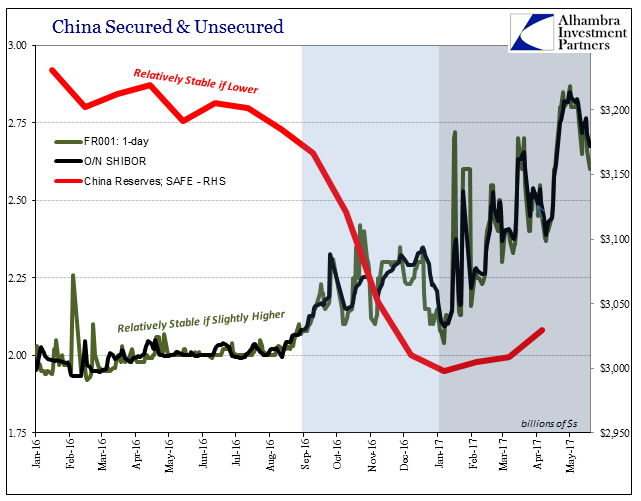

Judging by a lot more in June, they still haven’t. The overriding deficiency remains, as always, the “dollar” system and China’s ill-suited connection to it. They can wish for “inflows” and claim to be ready to buy all the UST’s in the world, but eurodollar erosion is still the constant baseline, if intermittently applied. There is as yet no spare RMB because there continues to be a (“dollar”) lid on reserve balances at the PBOC. It really is that simple, and fully accounted for right on the central bank balance sheet.

The long end of China’s treasury curve is merely the expected response to prolonged serious tightening, the further predictable intermediate term consequences that we have witnessed all over the world for just about a decade now. The only difference was that for years it was thought the Chinese were immune to such Western pressures, when all along their deal with the “dollar” devil was just waiting to be cashed in.

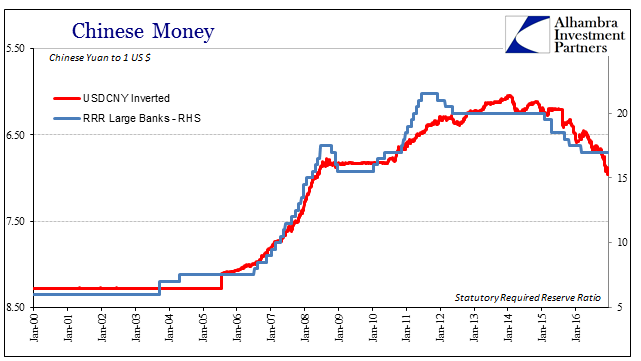

By pegging the yuan to the dollar for so long, the central bank essentially obtained any free “dollars” from its exploding merchandise surplus – as well as a great deal unrelated to pure trade (financial). That kept the currency stable, but it also created the Chinese “dollar” short whereby all those “spare” “dollars” were left on account at the PBOC rather than flow, as is commonly believed, to the importers who needed (and still do) them. As the asset side built up due to foreign accumulations, primarily “dollars”, the liability side (China money) could follow along, meaning Chinese money wasn’t purely fiat in the very strict sense of the term. It was “backed” by forex conditions even more than balances.

Stay In Touch