Nothing ever goes in a straight line. For every rally there will inevitably be a retracement, a minor selloff often of no more than profit taking. These are generally pauses where a durable trend either overcomes doubts, or succumbs to them. In the stock market, they call it the wall of worry. In bonds, it’s become a bit more complicated.

At this particular moment, US treasuries are again being sold. It’s really not to this point all that much, but you wouldn’t know it from the commentary trying to describe it. The headlines all scream in unison BOND ROUT! It is in many ways the opposite of stocks, where even larger corrections (like the liquidations in 215 and 2016) get shrugged off as nothing of great concern.

This disparity is, however, quite easily explained. Stocks on the way up are a reflection of the way the world is supposed to be. It just isn’t possible, in mainstream convention, for prolonged economic agony. Share prices as they are now, as they have been since especially QE3 in 2012, are signaling the end of the malaise and the belated return of conventional sense. Bond yields going only lower are a loud (and more robust) contradiction to good orthodox understanding of the way the whole world might actually work.

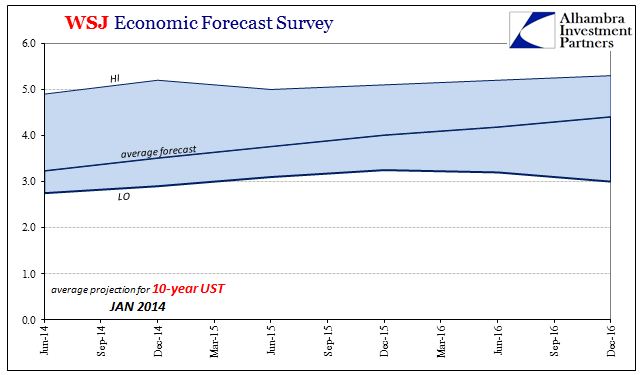

The Wall Street Journal every month conducts a survey of more than 60 prominent economists. Each gives future projections about 10 economic parameters like GDP and the CPI. They have been doing so going all the way back to December 2002, though you wouldn’t know it because the results are rarely mentioned, reflecting overall very poorly on the respondents. Among the primary variables is the 10-year UST yield.

In January 2014, not a single one of those economists forecast falling interest rates (as represented by the 10s). Most were extremely negative on the bond market, with the mere average estimate for the end of 2014 coming out to 3.52%, up from around 3% where the 10s had ended the turbulent BOND ROUT! of 2013. One economist actually thought yields would be above 5% by the end of that year.

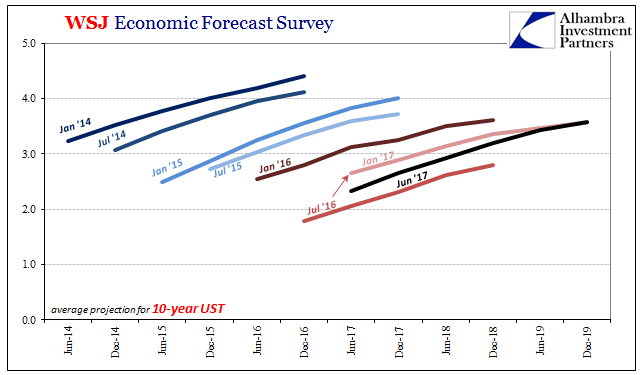

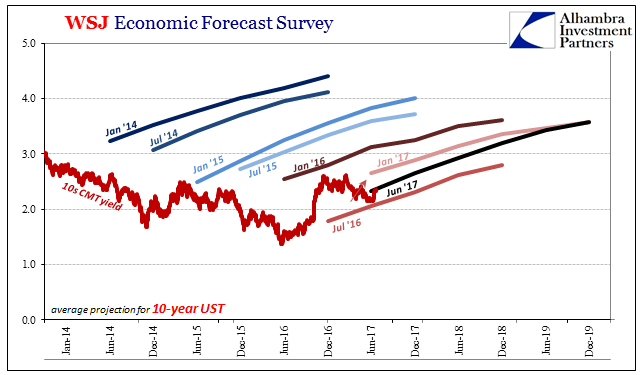

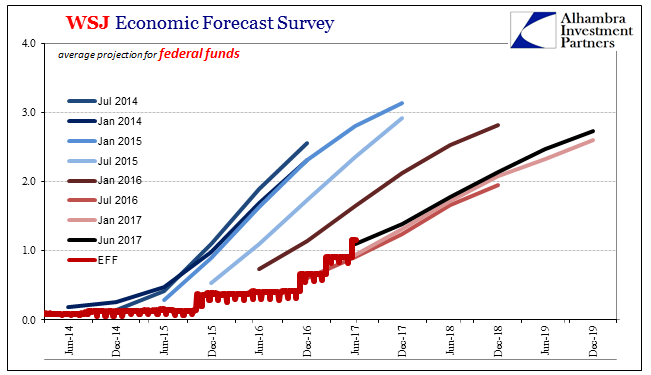

If you follow in time the monthly projections and how they are forced to change given what does occur, what sticks out is what doesn’t change. No matter what the 10-year Note actually does in actual trading, the slope of each and every projection every month is always, always the same (I’ve only included a sample of each January and July forecast averages). For economists, interest rates have nowhere to go but up even when they don’t.

It betrays this steady bias, a rigid almost religious fervor for the way it is supposed to be – no matter how many times in reality things just don’t work out that way. In a lot of ways it becomes harder to accept reality the longer it goes. It is the intellectual equivalent of the fallacy of sunk costs; economists are so sure that normalcy is coming, that especially monetary policy has to work (since it is designed by economists), the more time passes without that happening the more sure economists become that it will.

Rather than being forced to reassess and simply adapt to what market data is saying, as with any good science, the more hardened these positions instead become.

Therefore, every even minor bond selloff is treated as the BIG ROUT that gets started one that will make 1994’s seem small. It has to be that otherwise economists, and the media who depend upon them to craft narratives about what is going on, are in danger of being completely disproven. Protracted stagnation of this kind and of what bond yields represent is supposed to be impossible, purportedly made so by the application of orthodox principles in the form of central banks.

In some ways it is understandable in a very human sense. Interest rates have to go up for normal to happen, meaning for economics to be legitimized again. Seeing that in each and every minor selloff (even the “reflation” “routs” weren’t all that impressive in this context) is a defense mechanism of self-delusion that all people use on a daily basis (though for often small things) just to navigate such a complex existence.

The problem is, however, largely one of time. At some point, the economy that “should be” has to be recognized for what it always was – a fantasy devotion to economics that was never established in real world operation. When this last happened in the middle 2000’s, officials like Alan Greenspan were able to sidestep the contradiction as some unimportant quirk of 21st century financial technicals (the ridiculous “global savings glut”, for one). He had that luxury because then the economy was at least plausibly normal(ish).

There is no such in 2017. The paradigm that “should be” has been obliterated; destroyed, in fact, in the hot summer of 2007. There is simply no going back. It’s a damn unfortunate result, but an established one nonetheless. The sooner economists stop chasing fantasies and recognize their obvious biases, the sooner they might cease hyping what they clearly don’t get and instead work toward the real problem (money). Only when that happens can we project a realistic path out of this disaster, and then the realistic possibility of a truly epic bond rout.

Stay In Touch