To the naked eye, it represents progress. China has still an enormous rural population doing subsistence level farming. As the nation grows economically, such a way of life is an inherent drag, an anchor on aggregate efficiency Chinese officials would rather not put up with. Moving a quarter of a billion people into cities in an historically condensed time period calls for radical thinking, and radical doing. In one official party plan, it was or has to happen before 2026.

The idea has been to build 20 new cities for this urbanization, and then maybe 20 more. It led to places like Yujiapu in Tianjin. China’s answer to Manhattan was to include a replica Lincoln Center, a Rockefeller Center and even twin towers. Built to fit half a million, barely 100,000 live there.

There are numerous other examples of these ghost cities, including Kangbashi dug out of the grassy plains of Inner Mongolia. It is in every sense a modern marvel, 137 sq. miles of tower blocks and skyscrapers that sit almost entirely empty. There are now plans to build yet another one, south of the capital Beijing this time, to supposedly relieve pressure and pollution of that city’s urban sprawl. In the Xiongan New Area, this newest city will be three times the size of NYC, enough, if plans were ever to actually work out, to draw almost 7 million Chinese.

These are mind-boggling numbers and end up making truly eerie places for the few times when their existence is allowed to be acknowledged in the mainstream. The reasons for them are really not hard to comprehend, however.

The older ghost cities started out as pure demographics, a place for China’s new middle class to urbanize and economize. The more the rest of the world demanded for China to produce and ship, the more Chinese (cheap) labor it would all require. And there had to be something other than slums for this to happen, else any such intrusive transformation risked what was and remains a delicate power balance.

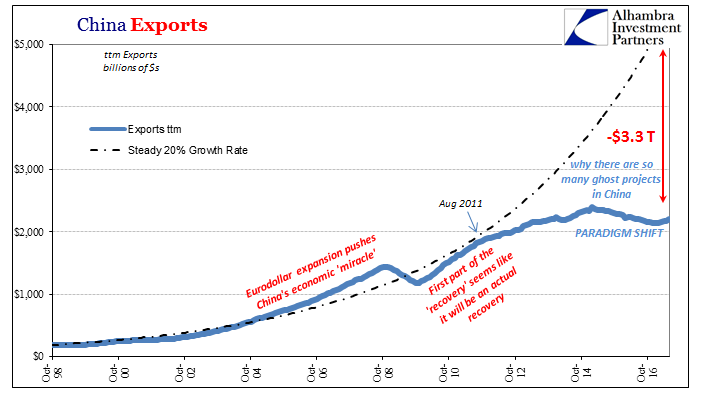

Then in 2008 suddenly the world paused in its love affair of Chinese-made goods. No problem, though, as Chinese officials assuming it was temporary merely sped up the process of building for the future, getting ahead of the curve, as it were. Surely China would need to after the full global recovery get right back on the same trajectory as before.

That never happened, and though some economists in particular still believe it will, there isn’t the slightest sign of global demand getting nearly that far back. What do you do, then, if you are China? There is logic to keeping up the illusion, that the future will eventually look a lot like the “miracle” past, because what else would China Inc. otherwise do? If it won’t be building stuff for export to the West, then it will have to be building something.

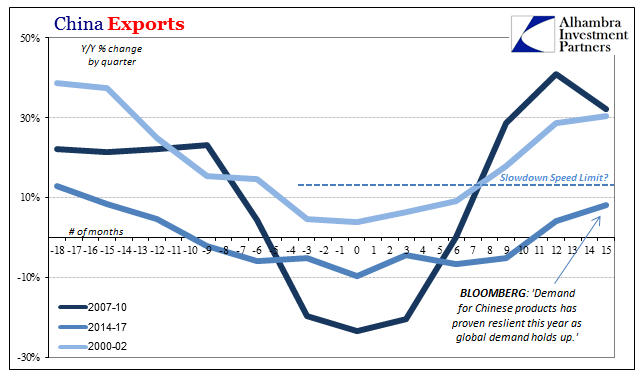

No matter how many times in the Western media they say demand is robust, catching up, or resilient, the Chinese know better.

China’s overseas shipments rose from a year earlier as global demand held up and trade tensions with the U.S. were kept in check amid ongoing talks. At home, resilient demand led to a rise in imports.

Demand for Chinese products has proven resilient this year as global demand holds up.

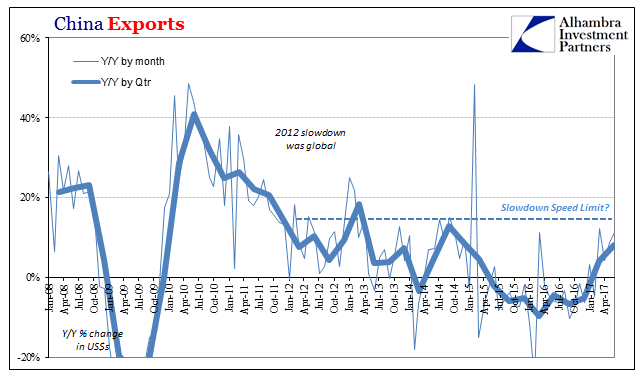

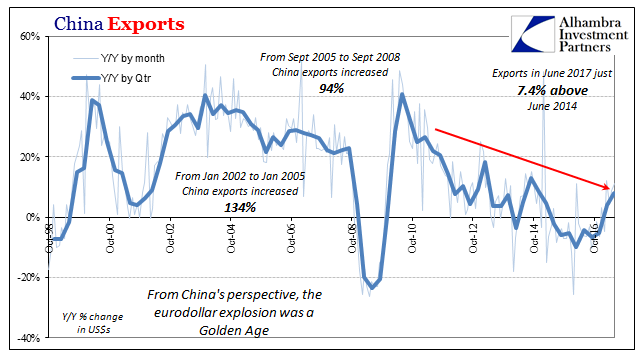

Chinese exports in June 2017 are estimated (currently) to have risen 11.3% year-over-year. It sounds like what was written above about the global condition. But in truth, 11% growth, as 15% or even 20% growth at this stage, keeps China in the ghost city state. It isn’t anything close to “resilient”, let alone enough to make up for lost time and absorb the empty cities already built.

There are instead already indications that China’s trade statistics are topping out – at levels not yet even as much as the insufficient growth rates produced in 2014. For the three months of Q2 combined, exports rose by just 8.1%. While that was the best quarterly rate in more than two years, it was less than what decelerating global demand required of China in Q4 2014 in the early stages of this “rising dollar.”

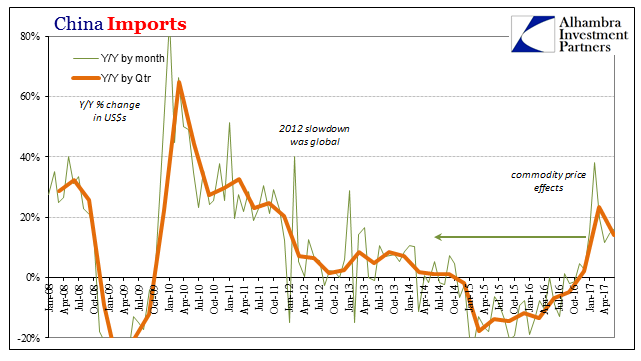

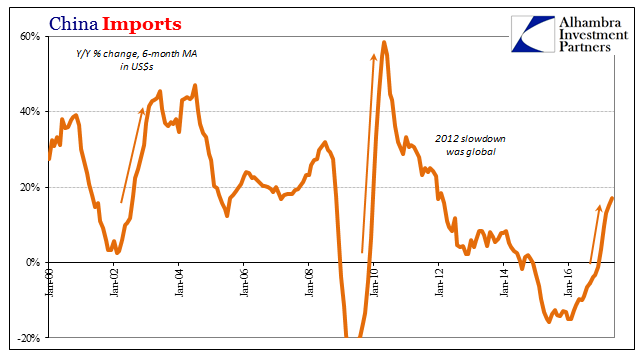

On the import side, the increase in June was for the fourth straight month less than 20%. Given the dramatic contraction especially in 2015 of Chinese imports, 20% only seems good outside of relevant context. After China’s experience with the dot-com recession, by contrast, by early 2003 imports grew by sustained 40% for several years.

The media can talk in glowing terms all it wants about China’s economy, but the truth is very different. It is instead consistent with the rest of the global economy in 2017, striking only for the distinct lack of momentum as “resiliency.” Enough time has passed since the end of the downturn in 2016 that if this was going to change it would have.

Whether in trade or local economy terms, going back to 2011 there is a ceiling on even the rebounds. There is something still very wrong with the economy, as even though it might be better this year than last it is still far short of normal. That is a reflection here through China on the rest of it.

Unless and until Americans and Europeans start buying Chinese goods again, any goods for that matter, there will have to be more ghost cities coming. Neither rebalancing nor global recovery are in China’s future. A 2014 Chinese government study concluded that as much as $6.8 trillion in so-called investments had been wasted from 2009 to that point. In the strictest sense it certainly seems to have been, but, again, what else were they going to do? Economists called it “stimulus” and still do, but in truth it was actually the last option in maintaining the (recovery) lie.

They are not ghost cities. It is still a ghost recovery.

Stay In Touch