Well, that clears that up. In case you missed it, back on June 27 Mario Draghi triggered the latest declared BOND ROUT!!! with what was characterized as a very upbeat economic assessment for Europe. And if things are moving forward there, they just have to be everywhere else.

It came off as “hawkish” in the sense that if real acceleration is at hand, ECB normalization of first QE then interest rates can’t be that far behind. The closer we are to the first part, closer is the second. Bonds sold off, and the collective mainstream imagination ran wild.

In truth, Draghi wasn’t “hawkish” at all, nor was he all that upbeat. The media, primarily, saw what it wanted and connected dots that it had created. As for the economy, he merely stated that it was progressing. Why that was particularly important was never stated, especially since Mario Draghi always says the economy is progressing. Out of his mouth, it never is otherwise.

More important than all that, however, the ECB chief was left to try to describe the current state of our central money problem, without recognizing it yet as just that. The economy may or may not be meaningfully improved, but inflation, the economy’s chief monetary indicator along with bond rates, will not behave. For Draghi’s speech, it was characterized as a contradiction.

Today the ECB finished up its latest policy meeting. For the mainstream, Draghi is now “dovish.” Gone is the certainty with which the world seemed to be moving toward a better place, replaced with caution and apprehension. Many ascribe this apparent 180 degree shift as a policymaker not wanting to upset markets. If bonds sold off in a rout after his last speech, he must have noticed and reacted with a more soothing posture this time.

None of that is actually going on, of course. Draghi was no more “hawkish” in late June as he isn’t now “dovish” in mid-July. At both times he was consistently confused. Today, he came as close as might be ever expected to stating that as a fact outright:

There really isn’t any convincing sign of a pickup in inflation.

As some reports noted, he stated that same thing several times with slightly different wording. The problem continues to be an absence of all the things required to make money become inflation – starting with wage growth. Without that, can the economy really be improving?

The answer is no, and even an economist like Mario Draghi knows it. In that respect, the European economy is as stuck as the US economy. When friendly outlets like the New York Times notice this lacking vital component, it cannot be as something of a trivial difference:

Central banking increasingly looks like an act of faith.

Mario Draghi, the president of the European Central Bank, and his Bank of Japan counterpart, Haruhiko Kuroda, have spent trillions of euros and yen without generating as much inflation as they want. Yet they have little choice but to insist their policies will eventually work.

The eurozone is finally experiencing a robust recovery and the only things lacking are a pickup in wages and inflation, Mr. Draghi said on Thursday.

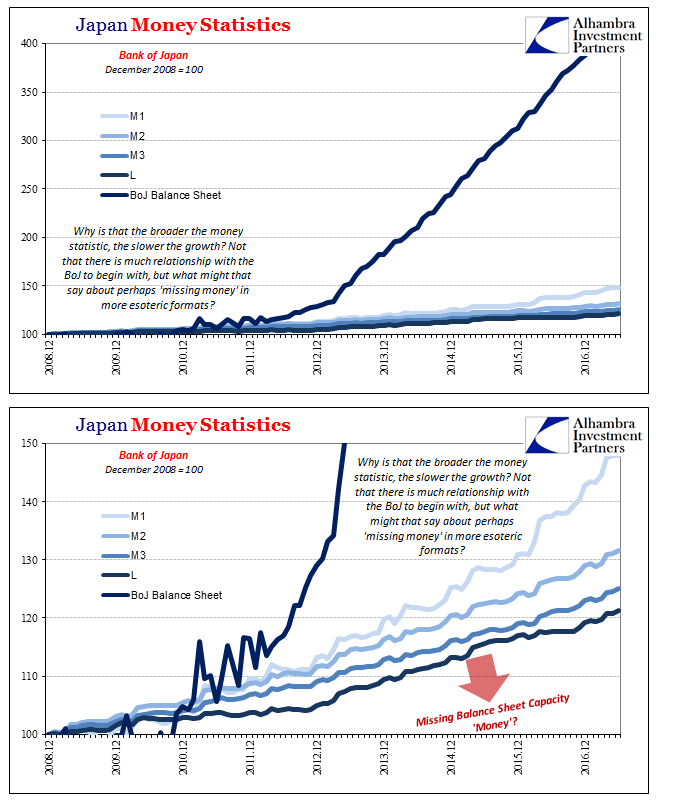

Is it really a “robust recovery” without a pickup in wages and household income? Mr. Kuroda can answer that question best with Japan’s experience stuck for a quarter century in, of all things, Japanification. The essence of that permanent stagnation is the lack of income and wage growth, the lagging behind of households that policymakers can’t for some reason see as the most important economic element.

Work equals recovery, and with more work comes more wages. Anything else is just the shifting of numbers, the economy flying erratically like a rocket without its tail fins.

Europe’s economy is booming, except it’s not. Mario Draghi is hawkish, except he’s not. If there is one thing policymakers, media, and regular folks in all these places are starting to really understand, it’s that something important continues to be missing. They may not yet know what it is, so the focus on inflation (and the bond market) is good in that “we” are finally starting to ask the right questions.

Stay In Touch