In July 2012, the LIBOR manipulation scandal broke wide and before Congress then-Federal Reserve Chairman Ben Bernanke used it to cleverly cover up for his crisis actions (more so inactions). He told the Senate Banking Committee that the LIBOR system was “structurally flawed” before intimating it had been that way for some time. Asked if the rates calculated by the British Bankers Association were reliable, Bernanke replied he would not, “give that assurance with full confidence.”

With recent government recommendations moving away from LIBOR, the fixing scandal has become something of a convenient excuse. The Federal Reserve has had for the last ten years starting August 10, 2007, a LIBOR problem. A big one. Bernanke more than anyone else has had great incentive to discredit the numbers.

A little over a week after his Senate testimony, Chairman Bernanke tried again in the House. One Congressman, apparently, was sufficiently awake to have none of it. Representative Scott Garrett challenged the Fed chief directly:

You have been before this committee countless numbers of times since 2008 and if this is the crime of the century, as so many people are reporting today, never once did you ever once come and mention it as being a problem, never once did you come here and say this is what you’re going to do about it.

It became the so-called crime of the century in official circles because it solved, partly, this lingering issue. The Federal Reserve’s problem with LIBOR was not that it didn’t work, but that it did! The cheating that went on while dastardly and wrong was a minor, trivial matter in the grand scheme of 2008.

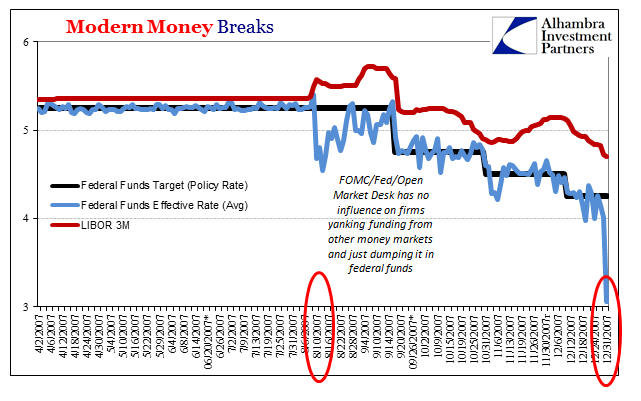

The whole of the crisis can be summed up by LIBOR on that one single day. Though August 9 is rightfully (now) remembered as the distinct start of the systemic break, why that was became perfectly clear on the next day.

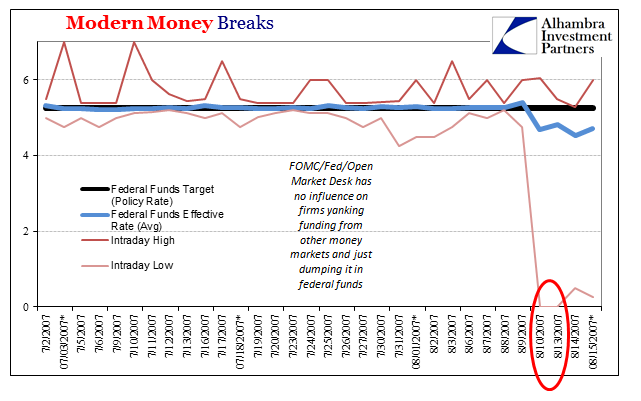

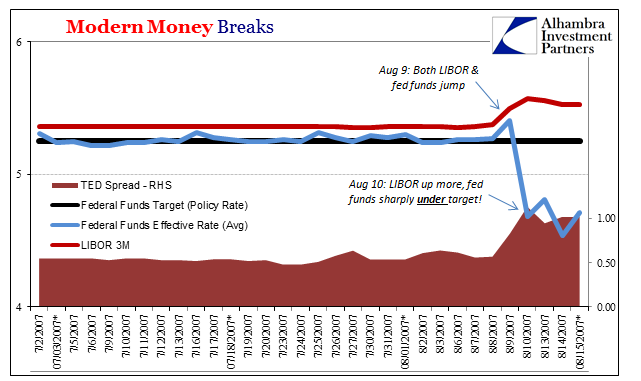

On the Thursday the 9th, both LIBOR and federal funds rose precipitously as you would expect of liquidity issues. On the 10th, however, LIBOR stayed up and even went further while federal funds did the opposite; closing that day well below the target rate.

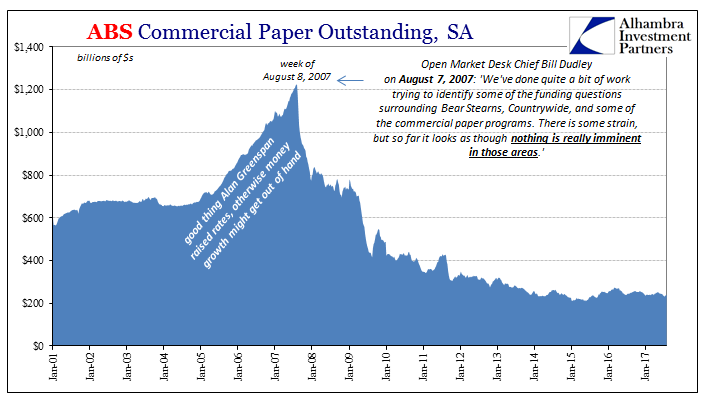

Earlier on that Friday, the FOMC held an emergency conference call given all that had occurred the day before – including the ECB being the first central bank in the crisis game with a €94.8 billion liquidity tender. The Fed’s response was a $19 billion three-day repurchase at 5.15%, 10 bps less than target.

MR. DUDLEY. Coming into New York time this morning, the federal funds rate was under upward pressure—6 percent or so for foreign names and 5.75 percent for domestics. We did a $19 billion three-day RP (repurchase) this morning, a single tranche RP with a 5.15 percent effective rate. There were $31 billion in propositions, and we accepted $19 billion. After that action, the funds rate has come off a bit. Foreign names are now 5.5 to 5.63. Domestics are 5.25 to 5.5. We expect the funds rate to come off through the day.

It did, and then some. I supposed you can chalk it up to that $19 billion as a technical or even symbolic matter, but this essentially dumping of excess cash in NYC would continue the next few weeks with no Fed action to attribute it to (or later in the year; or throughout 2008).

It was so much that on both Friday August 10 and Monday August 13 somebody out there in the wilds of global money markets were taking 0.00% interest for lending federal funds cash.

As that was going on, of course, LIBOR rates continued to do the opposite. You would think that would merit some mention during that emergency conference call on the 10th, or the one that closely followed conducted on August 16. In both of those calls, some 50 pages of combined transcripts, the term LIBOR was spoken exactly zero times. Not one single mention.

When the FOMC finally got up to deliberating these eurodollar rates at its regular September meeting, what the discussions instead revealed was that these “experts” didn’t really know what to make of the rate, the conditions, or the money.

MS. JOHNSON. So the spreads of overnight pound LIBOR, relative to target, opened up widely, and they were not addressed. They were allowed to just sort of sit there. The term pound market had a problem, too. Of course, many of the dollar issues that we have spoken of— and that Bill talked about—are really being captured as a London phenomenon. But you might say that, from the point of view of the Bank of England or the U.K. economy, these dollar issues are somewhat separate from the domestic economy. There is some truth to that, but also the institutions are involved, the institutions have obligations, and the shocks to the institutions reverberate back into the domestic economy, it seems to me. [emphasis added]

This Ms. Johnson in the transcript is Kathleen Johnson, at the time staff economist but very shortly to be elevated to the position of Senior Advisor, Division of International Finance (which explains a lot, actually). She is in the quoted part above absolutely right, but not in the way she meant it. Johnson was suggesting LIBOR whether pounds or eurodollars was something for the Bank of England to take care of because it was the banks in London doing all the trading in it.

Others like future Fed Chairman Janet Yellen were almost eager to view the LIBOR issue as one of term risk and nothing more significant than that.

MS. YELLEN. Really, the spike in the spread between term and overnight loans in the interbank market has been quite sizable, and it’s obvious that that has been complicating the difficulties that banks have had in managing liquidity.

I have also been concerned, given how many other borrowing rates are linked to LIBOR, that if the spread remains elevated, it has the potential to spill over into the rates that a lot of borrowers pay.

In other words, in times of trouble banks will always shorten maturities, therefore, in Yellen’s argument the issue wasn’t strictly LIBOR vs. federal funds it was instead 3-month LIBOR vs. overnight federal funds and nothing really out of the ordinary. Thinking this way, or like Ms. Johnson, misses the real distinction which is offshore dollars, really “dollars”, vs. onshore federal funds.

Yellen’s theory was easily disproved by something as simple as the TED spread, though Fed officials at that time, as they have done repeatedly, dismissed the reduction in the 3-month US Treasury bill equivalent yield (the TED spread measures 3-month LIBOR over 3-month bills equalizing maturities so as to isolate what should be just credit risk, or, as in this case, liquidity risk) as another anomaly to not quite ignore but given much less weight in the discussion of what was taking place than it really deserved.

It was a global crisis for banks, which is why the ECB, Swiss National Bank and others were practically begging the Fed for swaps.

Even when debating what they at the time called the ACF, making dollars available by parallel onshore and offshore auctions, they still never viewed these funding markets as they were. To these policymakers, all that mattered to each central bank was what the banks in their respective jurisdictions were doing. If banks in Europe were having dollar as well as euro issues, that’s for the ECB to handle. In fact it was easier for policymakers to think wrongly on the subject because they were having euro as well as dollar problems.

Cross-border funding, though a reality, was never, ever appreciated or understood for what it truly meant – as suggested very clearly by LIBOR over federal funds. They compartmentalized rather than saw that there was a single crisis point – global banks and credit-based money.

MS. KRIEGER. Well, starting with the last question, I think the sense is that it’s a dollar funding problem. Obviously, the markets are deepest here, so that’s part of the interest in offering it here to the broad range of institutions and the institutions that need it.

And what good would that do if a geographical divide had appeared, as the LIBOR spread to EFF or OIS openly declared? The geniuses here should have easily predicted the effect of offering funds in domestic dollar markets; the excess would be dumped in US markets (along with funds withdrawn from offshore in a feedback loop) with no way of getting into offshore eurodollar places (where LIBOR declared it badly in need) without private channels being reopened. The pitiful ACF and other swap lines that followed were tiny compared to the funding strains going on in so many areas simultaneously (as noted yesterday, in just ABCP alone the decline was almost $300 billion from the week of August 9 to this policy discussion on September 18, hitting hard European and Japanese issuers; and they were offering through the ACF cumulative totals of at most $40 billion over 4-weeks through the ECB, and $20 billion through the SNB; nothing to that point for BoJ, BoE, of BoC).

LIBOR demonstrated conclusively that they really didn’t know what they were doing. The first chance they got years later, Fed officials jumped wholeheartedly on board to discredit it; again not because it was unreliable but because it still today points the finger of blame squarely back at them. LIBOR told the world to look offshore dollar as the epicenter of crisis, dysfunction and panic; the official US central bank response was “not my job.”

Stay In Touch