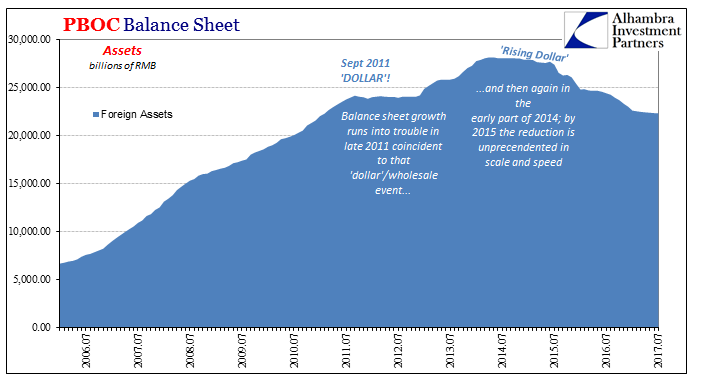

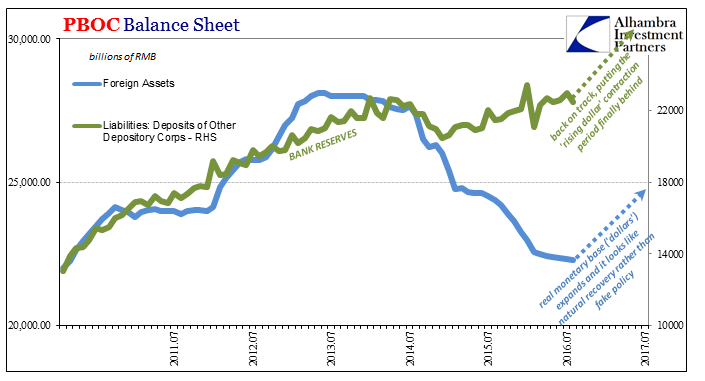

As much as officials in Beijing may outwardly fight it, they are still in the “dollar” business. It’s not raw conjecture, either. Though we don’t know the specifics of their policy positions, in this context we don’t need to know them; it’s all right there on the central bank balance sheet.

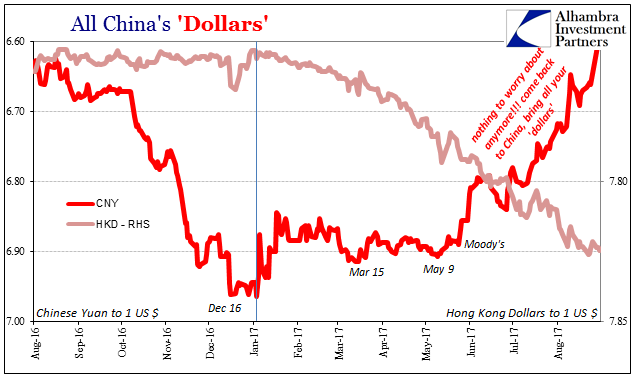

The most prominent thing about China right now is not its economy but its currency. CNY having spent the balance of three years dropping in often globally disruptive fashion (because it wasn’t really about China), is now hellbent for the moon. From a low of less than 7.0 to the dollar (during a one-day flash crash the PBOC went to some pains to deny ever happened even though it so clearly did), in just three months the yuan has erased more than a year of problems.

We simply don’t have enough information to piece together what is really going on over there, but it isn’t hard to guess “over there” involves a lot of Hong Kong. That shouldn’t prevent us, however, from realizing why whatever it is that is happening is happening. In this global context, that is (right now) the more important part.

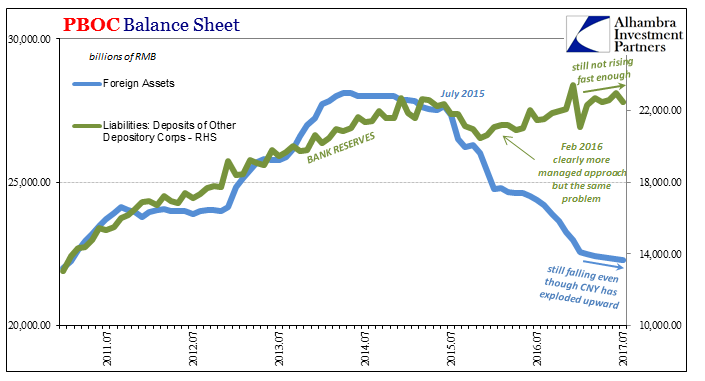

The easy correlation of the “rising dollar” as it pertained to CNY was whenever it dropped, bad things happened all over the world. It was a messenger of “dollar problems” located specifically right at the basis of China’s monetary system. The PBOC’s balance sheet is built upon “dollar” assets so their sudden and often acute (August 2015, for example) disappearance was that “devaluation” that economists couldn’t ever figure out.

Therefore, a “rising yuan” would seem to be the perfect antidote. If CNY dropping is monetary deficiency, then CNY rising should be its opposite, right?

Not quite.

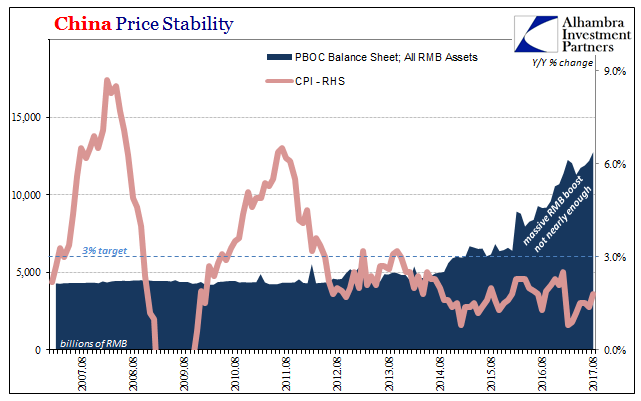

The past few months have seen the PBOC’s balance sheet still bleeding forex assets (“dollars”). Since the end of April (through the end of July), another RMB 102 billion has left the central bank’s books. That’s a far lower rate of decline, of course, but hardly what one might think of in light of CNY’s rocket appreciation during that time. It’s the primary clue that the currency move is artificial, an attempted manipulation rather than “dollar” market healing.

It is almost certainly the case where policy is attempting to lead the market where it wants the market to go. If currency instability to the downside was the measure and signal of “outflows” and the risks related to them, then shoving the exchange rate upward in a vulgar display of power might do well to convince “dollar” lenders that it’s safe to go back into to China. It’s certainly meant as an enormous “we’re back open for your business” gesture.

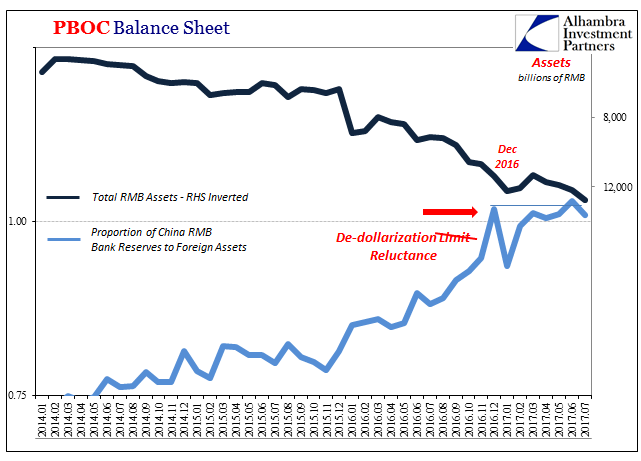

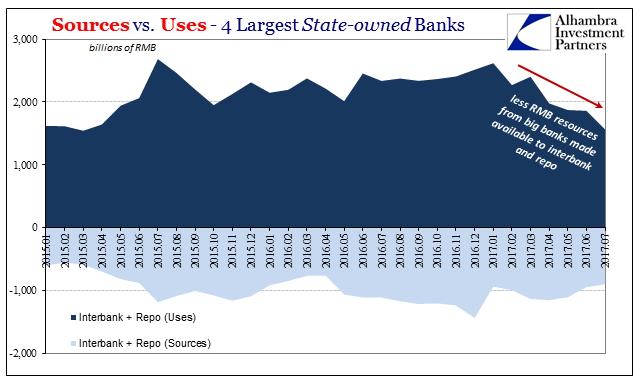

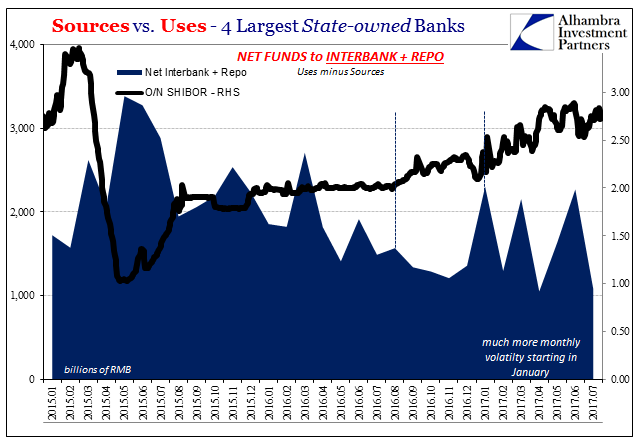

The reason the Chinese want more “dollars” is that they have pushed the limits of current internal policy. Starting in early 2016, the central bank shifted to cushion the downward monetary effects of “dollar” outflows by opening several liquidity conduits available largely to the largest banks. It was never quite enough, especially in the back half of last year when money rates started to rise.

There is nothing of actual practice that prevents the PBOC from simply “printing” RMB in greater amounts than they have done. Should they wish, they could. The fact that they haven’t, however, demonstrates fully that the Chinese remain tied to the “dollar” no matter how many times they might make noises about getting away from it.

Rising CNY as a “dollar” tactic in theory if it worked would mean “dollar” inflows again, likely heavy, which would then expand the PBOC’s asset side as a matter of natural flow. The increase in forex assets would therefore give it the flexibility on the money side (liabilities) to achieve calmer, less blatantly problematic RMB conditions both inside and outside of the big banks.

If Chinese officials were truly ready to ditch the “dollar” they wouldn’t bother with convoluted and potentially risky CNY manipulation (whether through HKD, JPY, or even EUR). It is instead the least worst option insofar as upsetting the status quo. Going too much further in “unbacked” RMB despite mainstream confusion on the subject can reignite uncertainty (which hasn’t disappeared) and therefore increase “outflow” risks. It makes sense to try to get the global money market to settle itself on China before taking more drastic steps.

The timing of the action also makes sense in this context. There is, or was, a global “reflation” background keeping (for now) a lid on some of the more dangerous monetary tendencies. More than that, though, the Chinese are simply running out of time. Not only is a political change possible this year, in economic terms nothing has so far truly worked.

China’s economy like that for the rest of the world has stabilized, but that hasn’t meant what it was supposed to have meant. It has at best stopped getting worse, but that hasn’t opened a possible path to restoring actual growth. The Chinese economy is clearly stuck.

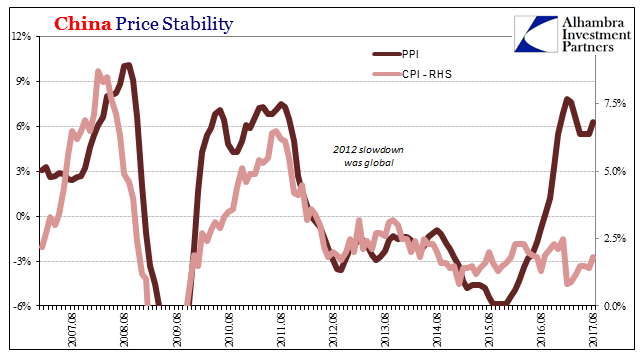

Inflation estimates released over the weekend demonstrate well this disparity. Their Producer Price Index (PPI) rose 6.3% year-over-year in August, reflecting lingering “reflation” hopes of the RMB type, while the Consumer Price Index (CPI) rose by less than 2% for yet another month (the Chinese government has set 3% as its official definition of price stability, and therefore the policy target the PBOC must work to achieve through monetary means).

Getting “dollars” to flow back in would be like an effective QE, a balance sheet expansion where bank reserves in China unlike those elsewhere actually matter; and one that would appear to be market-based rather than policy-based. After all the “stimulus” that has been tried recently, officials appear to be attempting one last go at “dollar” expansion. If it fails, then perhaps the Chinese get more serious about more drastic steps.

That they aren’t there yet in my view suggests just how drastic they think it could be to go beyond that monetary boundary. The Chinese economy is in a very precarious state, no matter all the happy talk about rebalancing and stabilization. The former isn’t really happening, and the latter isn’t what it was supposed to be. Putting a whole lot into maintaining the status quo when it was the status quo that put you in this position says a lot.

Stay In Touch