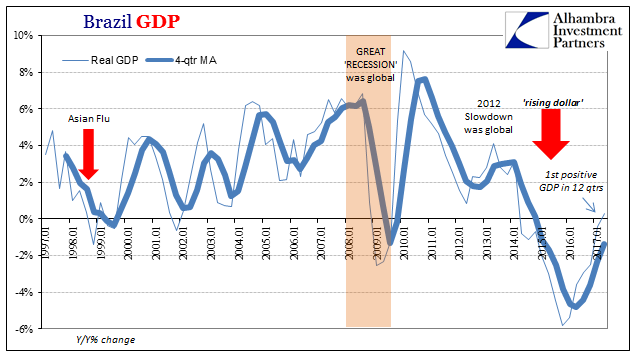

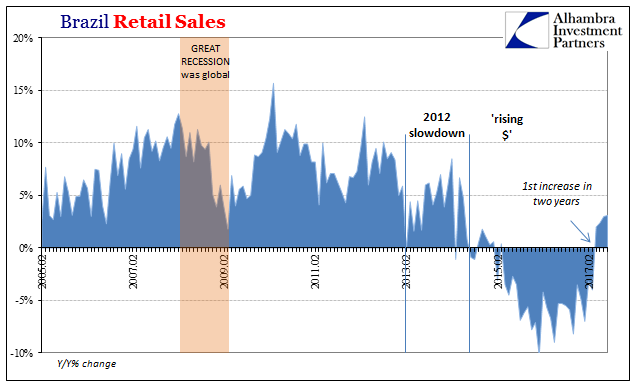

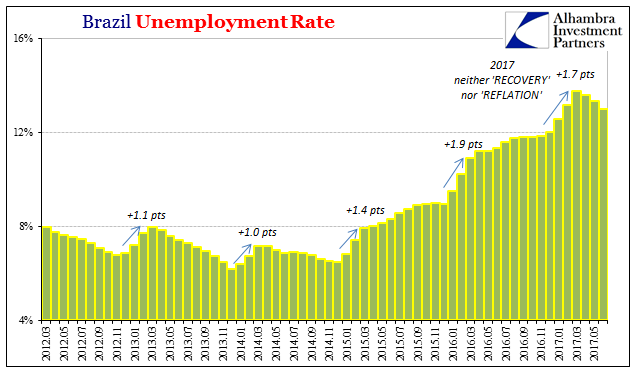

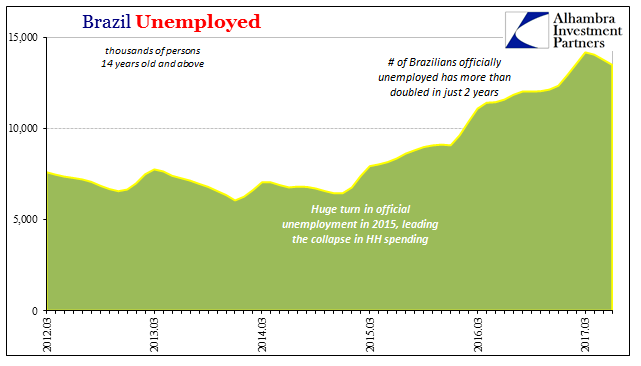

Of all the countries around the world impacted by the “rising dollar”, Brazil got the worst of it, at least out of the major economies. What Brazilians have experienced over the past four years is nothing short of 1929-style collapse. By every economic statistic, that economy has been utterly devastated.

In Q2, however, real GDP rose year-over-year for the first time in three years. Not since economists here in the US tried to make sense of 2014’s Polar Vortex has Brazil’s measured output increased. That confusion and Brazil’s sudden downward lurch were actually quite related.

In the linear orthodox world of recession (or outright depression)/not recession, that must mean recovery and relief has started? Unfortunately no.

So far what is indicated is what we find everywhere else in the world in the aftermath of this global downturn 2015-16. The contraction ends, but only listless, meandering partial growth thereafter. There is no momentum or positive cyclical contributions, and especially none like you would expect after three years of serious contraction. By all historical experience, Brazil should be booming by now.

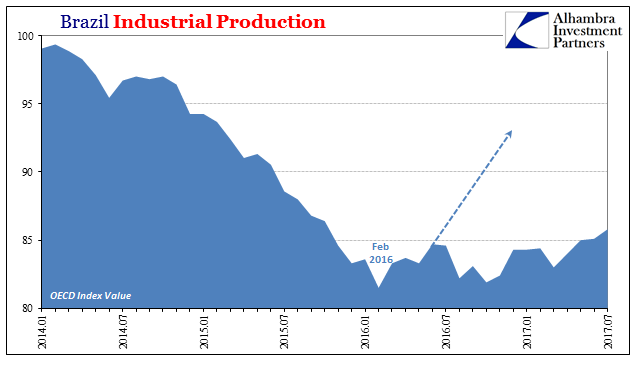

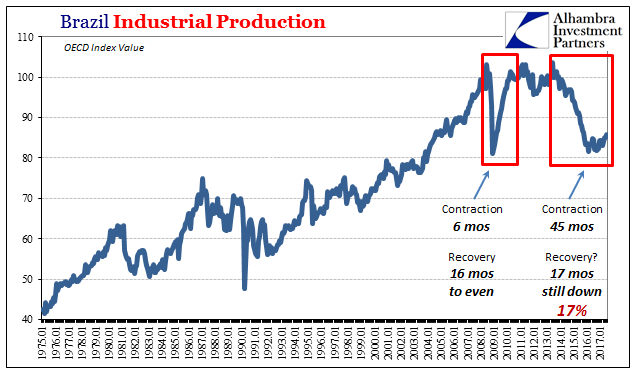

Industrial production, the bedrock of the Brazilian resource economy, is perhaps the perfect illustration of all this that is missing. In domestic as well as international estimation, the trough of Brazil’s contraction was the same as we find everywhere else around the globe – February 2016.

The total decline from the peak in June 2013 was an unfathomable 21.4%. What really makes it so is the time element. During the worldwide Great “Recession”, IP collapsed by a similar amount, down 21.2% peak to trough but only 6 months top to bottom. It took the next 16 months for industrial output to regain that prior peak.

It has been 17 months since the more recent bottom, and yet Brazilian Industrial Production remains 17% less than the peak four years before. The series has returned to growth, but in an unusually shallow manner not just set against the preceding contraction but for any other context, as well. This is the condition with which the world economy has become far too acquainted.

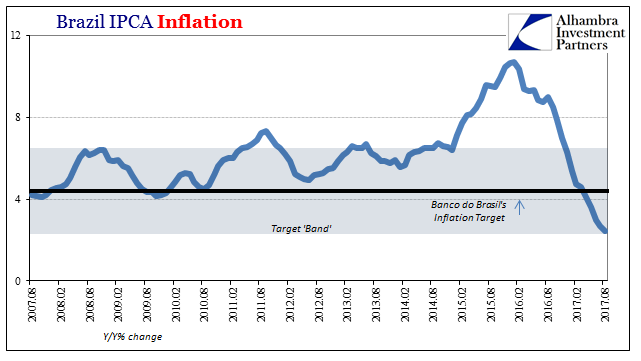

It hasn’t mattered the currency’s re-emergence from the “rising dollar” doldrums. As the real sunk in response to the global monetary system’s decay hitting now the EM parts (after ravaging America in 2008 and Europe in 2011), consumer price inflation reached ridiculous proportions as the consequence of Brazilian banks being forced to pay high premiums to secure “dollar” financing (and the mistakes of Banco do Brasil in making it worse along the way).

But as the real has stabilized and reversed, so too has inflation. The latest monthly estimate (August 2017) was actually fractionally below the lower bound of the central bank’s target band. It hasn’t, however, aided all that much in what should be Brazil’s recovery. If inflation was one of the channels devastating that economy, and it was, it is important to note that the lack of it now hasn’t led to symmetrical effects on this other side of the “rising dollar.”

The economy rebounds but it really doesn’t; meaning that the contraction has stopped, but little other apart from that.

The direction is right but the intensity is all wrong. It raises the question of “where are all the cyclical forces?” Because of their global absence, Brazil again being perhaps the most extreme example, we have to consider that the downturn wasn’t actually cyclical, either. If there was any place in the world where we should expect to easily find evidence of cyclicality, it would be here where the worst had happened.

And yet there isn’t. Wherever the “dollar” storm hits and focuses, it leaves afterward less than when it had started (sometimes a lot less; like the US after 2008, huge swaths of Europe after 2011, and here in Brazil after 2015-16). It’s the only way all around the globe we can find this dreadful pattern of what sure seems like permanent withdrawal of capacity.

Stay In Touch