The year 1995 wasn’t exact a good year to remember. There was the Oklahoma City bombing, the San Diego tank rampage, the New Jersey Devils winning the Stanley Cup in a lockout shortened NHL season, and some former Buffalo Bills running back named OJ getting into trouble out in LA. Steve Forbes would announce his candidacy to challenge President Clinton that September.

Despite all that, in 2017 both the bond and stock markets are almost desperate to repeat the year, at least its financial and economic characteristics. To be more precise, it is stock investors who are betting on a 1995 while bond investors are holding out against that scenario – leaving Economists and the media to openly cheer for it and directly against them.

Though it took place largely in ’94, the bond “massacre” lingered and still stings in bond traders’ collective memories. Alan Greenspan’s Fed has begun to raise interest rates after several years of very low federal funds, “stimulus” the central bank judged necessary because of a sluggish, almost jobless recovery (just ask President George H.W. Bush who Clinton defeated on “it’s the economy stupid”). That for many people is as compelling a setup as there may ever be.

There were questions in ’95 about the economy, but those would soon be answered in the affirmative. It was clearly growing again, so long bond rates sold off, hard, to reflect the economic opportunity of the strengthening growth cycle.

For stocks, it was also affirmation.

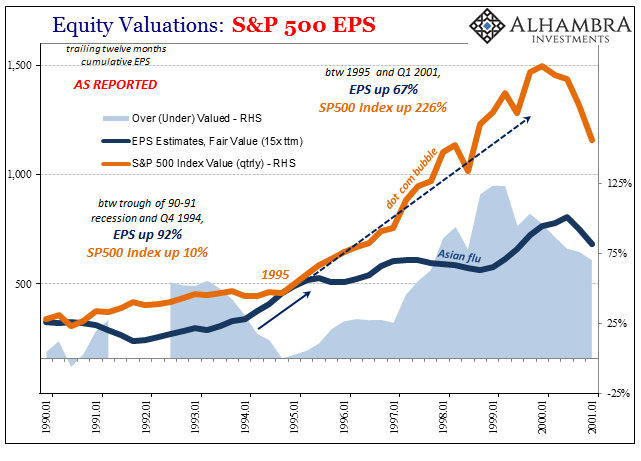

If we look at the current state of the stock market, at least as presented by the S&P 500, it is about as overvalued right now as it was in 1994 (defining “fair value” to be 15 times ttm earnings). Earnings had predictably slumped as is usual in the 1990-91 recession and like the economy overall were slow to rebound from it. Starting around 1993, however, EPS began to rise sharply so that by 1995 the index had actually achieved fair value.

From the recession trough, earnings had surged by 92% with only a 10% rise in prices.

The problem, of course, was what came next. Given the (false) confidence injected by Greenspan, stocks went on a nearly six-year run that was never corroborated or supported by earnings growth. Throughout the dot-com bubble era, EPS rose a decent but not spectacular 67%, while the S&P 500 index bubbled up 226%.

It was this later period that calls our attention, not 1995, especially in comparison to today. Like then, stock prices have for several years risen without the support of earnings. In the late nineties, that was easily rationalized in one part due to the economy of the time. It was running at a truly robust clip, not quite mid-1980’s growth but solid in sustained fashion. It was very tempting to just assume given that economic background EPS would simply catch up at some point (especially in the “new economy” prosperity everyone was buying into).

Even the EPS growth background in 1993 and 1994 made it seem almost likely. With the “maestro” running the show, and the promises of the “new economy” becoming reality in a lot of places, investing took on the characteristics of the future economy that “will be.” People merely lost their sense of time, or how many years valuations had continued to stretch without ever checking these assumptions against realized fundamentals.

The choice for investors today is 1994 or 1999. Is the overvaluation in the stock market about to made up by EPS growth that once again catches up to it, triggering another bond market massacre along with it, or are stocks rationalizing fundamental characteristics that are further and further divorced from reality?

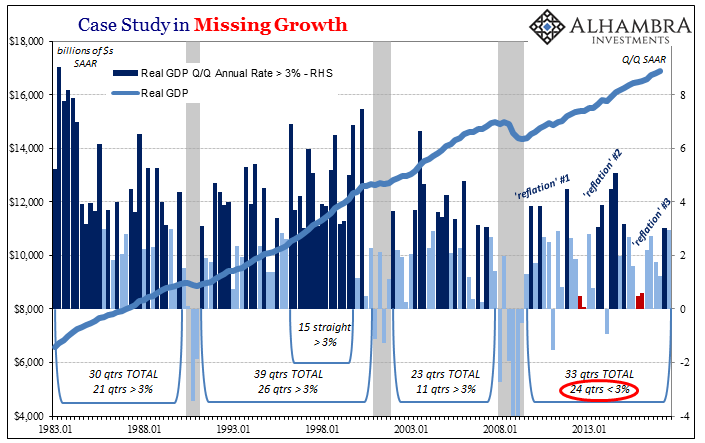

The market is not the economy, and the economy is not the market (whenever I type that phrase out it comes into my head in Joe Calhoun’s voice), but fundamental analysis does matter for each of these markets. The probability that things work out like 1994/95 are slim given the backdrop of growth (really anti-growth, ongoing non-linear contraction). There are none of the characteristics of either age indicated anywhere right now, which is precisely the position of the Treasury market.

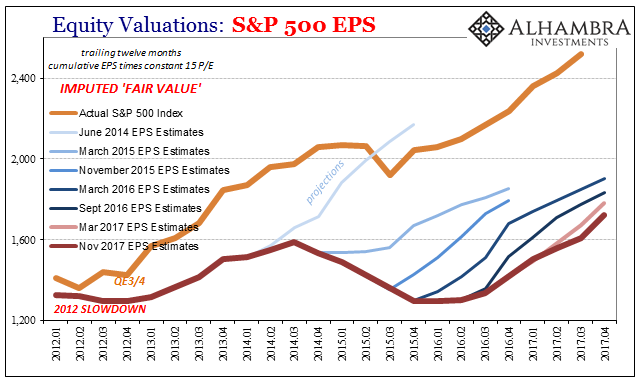

EPS for the S&P 500 has been rising for five quarters in a row, though not robustly so. In the current (Q3) quarter earnings for the index are finally expected (pending expected downward revisions) to surpass the previous high reached more than three years ago. That gentle rebound is nothing like 1994, and it’s not even late nineties, dot-com bubble EPS growth.

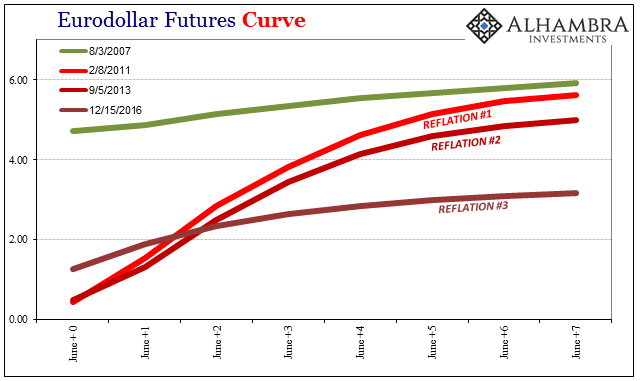

So valuations turn again only forward, the economy that “should be” but never is. This appeal to what’s always over the horizon goes back to QE3, when stock investors decided that the third time was the charm though bond investors bought the premise for only a few months in later 2013. The bonds vs. stocks disagreement has been a constant feature since then, which for all that has happened (including “rate hikes”) is really noteworthy.

If the markets and economy were on the cusp of revisiting 1995 we should have seen something by now that would suggest it. Anything. Instead, as hard as it is to believe, 2017 has been disappointing in almost every way imaginable on economy as well as the baseline characteristics driving it (money). Stocks may be overvalued to the same degree as in 1995, but that’s really the only similarity between then and now. There are many more shared characteristics with the dot-coms, and that’s without considering the no-growth paradigm that persists today.

There isn’t even central bank (psychological) support anymore, even though it was always a misimpression about what (little) central banks actually do. What’s left are rising risks, not in bonds but stocks. It’s exactly the opposite of how the financial world is currently described – which may be one reason for it. Though separated by just four years, there was a world of difference between 1995 and 1999.

Stay In Touch