As expected, Cyber Monday hit records all across the retail industry. According to Adobe Insights, sales recorded by online outlets, including those of traditional brick and mortar stores, hit $6.59 billion. That’s a record not just for a Cyber Monday but any single day in the internet’s two decades of mainstream usage.

It was, Adobe said, a gain of 16.8% compared to last year. The analytics firm also estimates that online sales made last week on Black Friday were up 10% over 2016.

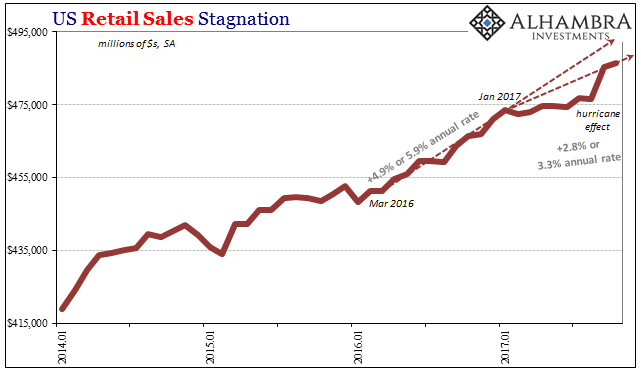

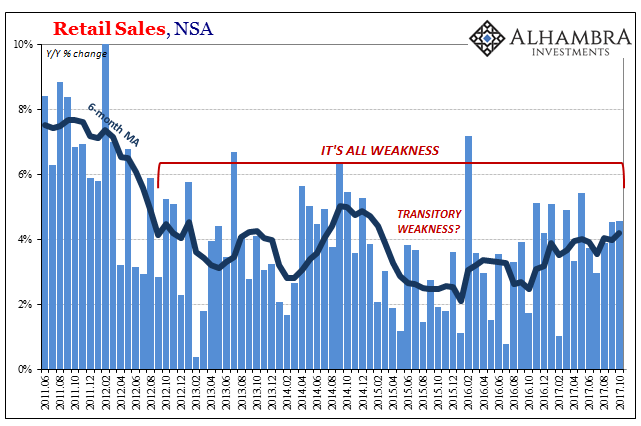

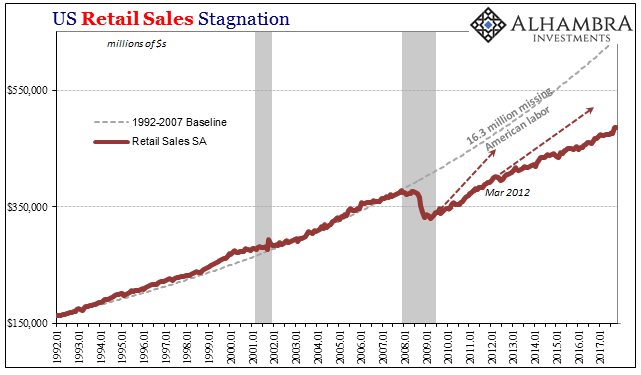

Retailers have been quick to tout their beefed up virtual presence, and their results, as noted yesterday. That’s all well and good if it means consumers are spending more overall. It doesn’t necessarily follow, however, as retail sales have been suggesting for some time. In other words, consumers are increasingly drawn to internet shopping out of necessity, meaning prices, prices, prices. A healthier condition would be driven by income and wage growth instead.

The National Retail Federation (NRF) had earlier promised a more comprehensive review of total Black Friday festivities, including sales recorded on Cyber Monday, to be released today. As of this writing, no data has been made available (when it is published I’ll update this post or if noteworthy put out a separate story). Thus, while news of online success permeates the mainstream narrative very little is being said about the whole consumer picture.

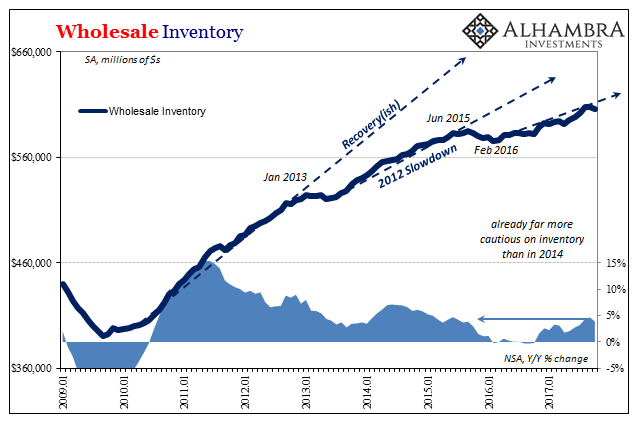

One notable data release that did take place as scheduled this morning does relate to that overall view of the current retailer experience. The Census Bureau reports in its advance release that wholesale inventories fell rather sharply in October 2017 – right in the middle of what was the buildup getting ready for the Christmas retail rush.

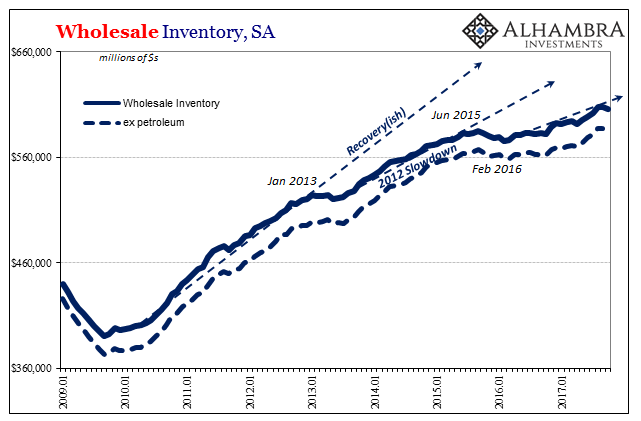

Though the advance inventory report for October doesn’t break down wholesale inventory by specific categories, including petroleum, as opposed to wholesale sales excluding petroleum inventories makes little difference in the overall inventory pattern and picture.

The data, subject to revisions as always, suggests far more caution on the part of US sellers as a whole, where wholesalers take their cues from retailers. It was the latter who apparently liquidated a whole lot of stock in September. While that may have been a drawdown related to storm disruptions, the fact that there was no resounding rebuild in October (and then a wholesale inventory drawdown) instead strongly suggests intentionally lightening the inventory load ahead of the holiday season.

That’s not the behavior of a confident goods economy salivating over the prospects of a Christmas holiday celebrated in light of a 4.1% unemployment rate. Inventory in 2017 was already lackluster across the supply chain, owing in big part to the persistent overhang from 2014 forward where the US retail and wholesale industries had been overoptimistic about the economy (where might they have gotten that idea?). It doesn’t appear as if retailers wish to make the same mistakes overemphasizing the significance of online shopping in the context of otherwise weak consumer spending.

This year, in one sharper contrast to 2014, there isn’t so much outright over-production, I believe, because retailers in particular just aren’t seeing the uptick in overall sales, or at least not nearly to the degree that would match the mainstream rhetoric. They appear in heading into the make or break Christmas season much more subdued (as noted also yesterday, in hiring as well as holding inventory), a function surely of actual rather than the usual hoped for, and hyped up, economic conditions. The rest of the supply chain, therefore global economy, is falling in that line.

Stay In Touch