I could understand it if its track record was spotty, or partially mixed. But the level of denial runs deep and wide with the yield curve. There is a growing chorus of nonsense, really, which is attempting to spin the flattening as some kind of benign technical rotation that through illogical convolution equals the opposite of what is obvious.

Let’s start in the right place with the premise that a flattening yield curve doesn’t necessarily mean recession. There is an unhealthy obsession with curve inversion, though one that is at least rational (relative to all this) in its basis. The problem lies in thinking that a turn in the business cycle is the worst case, and so it might be incumbent upon good analysis to look for it.

The worst case is instead, as we all should easily appreciate, the complete lack of any business cycle. This is truly where so much confusion reigns; if you believe the binary recession/not recession model of the economy then the world just doesn’t make much sense, the bond market least of all.

It has left the mainstream groping for some kind of answer where the yield curve can be simply negated. Two weeks ago, Bloomberg said it was, get this, record high stock prices:

With the S&P 500 Index hitting another record, and year-end only weeks away, pension funds and investors committed to a balanced portfolio may want to lock in equity gains and add fixed-income, according to Deutsche Bank. Of course, it’s not exactly an ideal time to be purchasing 30-year Treasuries either — they yield 2.75 percent, down from as high as 3.21 percent in March. But the duration at least serves as a hedge if the stock-market rally comes to an end.

In other words, the big money managers are just hedging a little for how awesome everything is. Not only that, the comfort that might come with thinking buying at the long end is because of this has been met by equally peaceful selling at the short end. Allegedly. Also from Bloomberg:

The seemingly worrisome dynamic in the world’s largest bond market — the flattening Treasury yield curve — may have a relatively simple explanation: Japanese banks are selling short-dated U.S. debt.

A combined uptick in currency-hedging costs and paper losses on Treasuries with short maturities has likely spurred Japanese lenders to pare exposures in recent months, according to Citigroup Inc., citing shifts in dealer inventories and Ministry of Finance transaction data. [emphasis added]

I have to note the inclusion of “a combined uptick in currency-hedging costs” into this attempted rationalization for what it really is, a familiar negative to those who get what bonds actually mean (interest rate fallacy):

The negative yen basis swap acts like leverage where even yields on the interim “investment” are negative. Any speculator or bank with spare “dollars” could lend them in a yen basis swap meaning an exchange into yen. Because you end up with yen you are forced into some really bad investment choices such as slightly negative 5-year government bonds, but that is just part of the cost of keeping risk on your yen side low. Instead, the real money is made in the basis swap itself since it now trades so highly negative. The very fact of that basis swap spread means a huge premium on spare dollars; which is another way of saying there is a “dollar” shortage. Because of the shortage and its premium, you can swap into yen and invest in negative yielding JGB’s in size and still make out handsomely. There has been, in fact, a rush of foreign “money” into Japan to take advantage of this dollar shortage; the fact that there has been such enthusiasm and it still has not alleviated the imbalance proves scale and intractability. [emphasis added]

The other side of a dollar shortage is, quite simply, “a combined uptick in currency-hedging costs” from the perspective of Japanese banks.

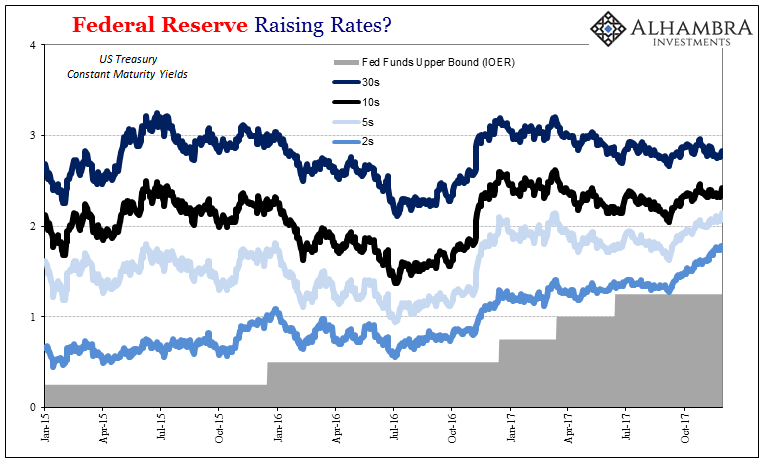

The yield curve is itself really two different things that meet somewhere around its middle. At the short end, things like bills and short-term notes are instruments that act like more purely monetary alternatives the closer to overnight you get. These move often in direct relationship with monetary policy rates (T-bills and repo irregularity the obvious and notable exceptions).

At the farther ends to the right are more purely economic considerations. Placing money in UST’s or some other alternative for many years speaks to general opportunity, or really the perceived lack of any. In the mainstream these two often very different parts are fused for that one misconception – that the central bank and monetary policy is always right and effective.

What the left or short side of the curve is saying is that the Fed is increasing some money rates; that’s it. It makes no comment on the veracity of any economic or really monetary (persisting dollar shortage, for one) interpretations of that policy. The FOMC is voting to increase the federal funds corridor and the short end of the UST curve is recognizing the higher rates for money alternatives it presents.

The long end is where the meaning goes. It is clearly saying that no matter what the Fed does today, the utter lack of economic opportunity remains the same. The Fed may be “raising rates” but the bond market here is totally unconvinced that they are doing so for sound, legitimate reasons (of inflation, unemployment, and money, or “dollars”).

This is the breakdown of interpretation. The mainstream, or most of it, still, somehow, thinks the Fed is infallible. If it is “raising rates” then surely the world is getting so much better, maybe even overheating. The bond market unlike the media hasn’t forgotten the last few years.

Forget that falling yields have been consistent with actual economic growth, the absence of it, this time Economists have got it right? What changed? Central bankers started out downplaying any economic risks, and then the Great “Recession” happened; after it, they played up the recovery story at every opportunity, and it never came. Now they are, out of nowhere, economic experts despite being utterly wrong from Day 1? That’s a lot of days (3,770 since August 9, 2007) to just set aside in order to start believing this time, this time, they have to be right.

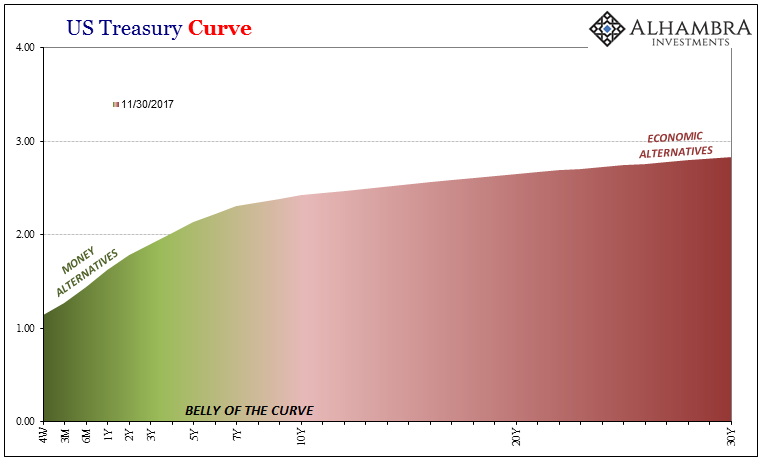

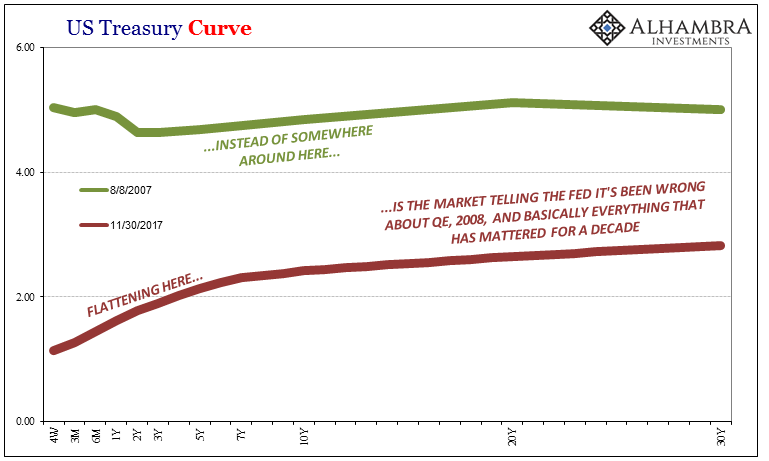

The yield curve is quite simple, which again proves Economists don’t understand bonds (therefore money). The long end is saying unequivocally that nothing has changed or will change no matter what happens in the short run (TIPS and eurodollar futures agree, too). If the yield curve was to have flattened at higher nominal rates across-the-board consistent with, or even just close to, pre-crisis levels, then these attempts to force benign interpretations of what otherwise is a very, very bad sign would stand a chance of being other than laughable.

Stocks may have jumped on tax cuts, but the bond market just shrugged – a very telling dichotomy, one that is being litigated in these examples with clearly increasing absurdity (a mark of desperation) on the one side. Economists believe heavily in the power of tax changes, too. Some problems are bigger than all that.

Stay In Touch