As part of its effort to stress its own self-importance, the Federal Reserve conducts a survey of the Primary Dealer members through its New York branch. A written questionnaire is sent out to each bank in advance of every monetary policy meeting. The purpose is for monetary policymakers to make sure that there aren’t any big surprises, that the market, or, in this case, orthodox Economists working for one part of the market, is seeing things consistent with how the Fed wants them to.

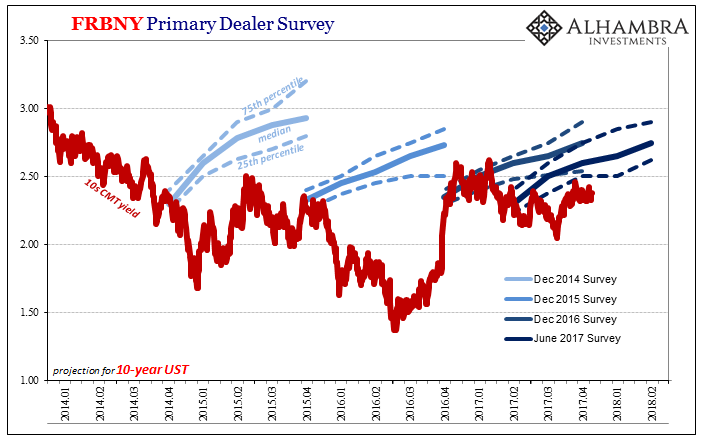

In September 2013, the Primary Dealer Survey questions included a few pertaining to the then ongoing “taper tantrum” roiling markets around the world. It was “reflation” #2 and like the others, both the one before and the one after, it came on rather quickly and harshly. On the issue of benchmark interest rates, in the form of the UST 10s, the Primary Dealers all saw interest rates rising still further into the foreseeable future.

Of those surveyed, 65% believed that the 10-year yield would be above 3% by the end of 2014; more than three-quarters, 78%, thought the same for the end of 2015, including 15% who were expecting the 10s to get above 4.50% compared to just 6% who guessed, correctly, 2.01% to 2.50%.

With the long end of the treasury curve trading sideways to slightly lower over the past nearly two months, that means yields here are lower today than one year ago. But, as you can plainly see above, the Primary Dealers never, ever expect rates to go lower. They are seriously biased toward rising nominal yields not just at the right of the curve but in all spaces.

One of the problems with at least the Dealer survey is, again, it’s not really the Dealers who are being surveyed; it is the Economists at those banks who are given the task of reporting to other Economists at the Fed for what the “market” thinks is going on. This is not the first time such massive disconnect or even dissonance has played out in this fashion.

Practically the whole of the last ten plus years has been in one way or another Economists confirming each other with each other and then wondering why it never works out that way. In early 2007, at a time when there was at least a chance something might have been done before the worst of the panic, the FOMC spent a lot of time dismissing the market verdict of eurodollar futures which was very plain in suggesting grave, broad market concerns about what was unfolding – that subprime wasn’t the real element to focus on.

Eurodollar futures were in policy discussions dismissed outright for among other reasons the surveys. These had showed Economists at the Primary Dealers expecting other things than the traders at those very same firms who were actually putting those firms’ money into those alarming eurodollar futures prices.

What specifically elicited Lacker’s question was Dudley’s prior attempt at an answer, “Well, another explanation is that the economists who make the dealer forecasts are not the traders who execute the Eurodollar futures positions.” In other words, the FOMC was taking the side of the economists. This is disturbing on so many levels, to discount very good market information in favor of econometrics, and to so in blanket fashion.

Thus, the Primary Dealer surveys amount to the same kind of echo chamber as the Beige Book. That’s a problem because it reinforces all the wrong ideas in the official sense about what’s really going on – the view from Economists rather than the market (though the latter isn’t really needed in that market prices do tell you what’s really happening so long as an Economist you can actually stand to be blatantly and persistently contradicted).

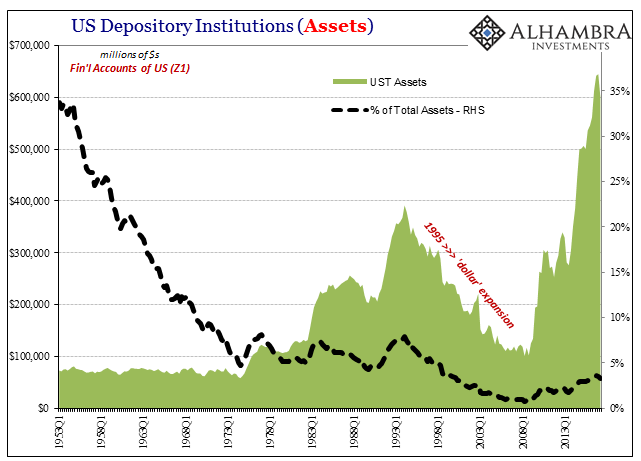

As it turns out, banks have been buying the feathers out of UST’s at the very same time their Economists expect rates to rise if not skyrocket. Though interest rates have nowhere to go but up according to the Primary Dealers, the banks themselves have been lining up to buy those very bonds their own Economists tell them are the worst investment of our lifetime.

We hear very often that regulation is to blame for this, particularly the LCR put into the Basel 3 schematic. You can see here (and what’s below), however, that banks act not on government but true market conditions (that are often very different than what officials say). It was the fourth quarter of 2008 when the US domestic banking system began its UST binge, one that was to accelerate massively in Q3 2013 just as the survey results were talking only the opposite for rates and therefore prices.

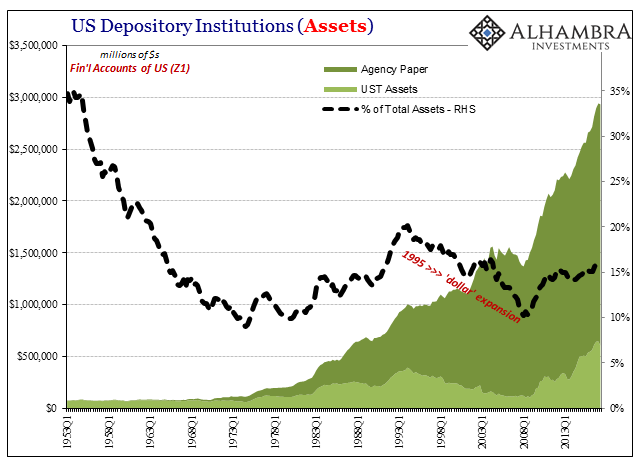

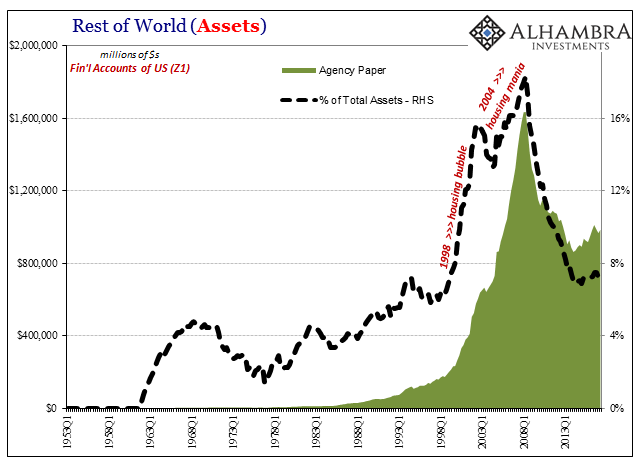

What we find in bank holdings of treasuries is only part of the story, and in many ways a small part. Banks have always been cognizant of their liquidity profiles, it’s just that in the years before the crisis (especially 1995 forward) they started to believe Alan Greenspan and his “put” way too much. UST’s had come to be supplemented by agency paper in terms of what counted as the highly liquid.

It may seem counterintuitive, but US banks have been going nuts for agency debt assets since the worst right after Lehman. Despite the hardships supposedly forced on the system when Fannie and Freddie were pushed into conservatorship in September 2008, the week before Lehman, US banks have been keen to own any MBS stamped with a GSE guarantee. Why?

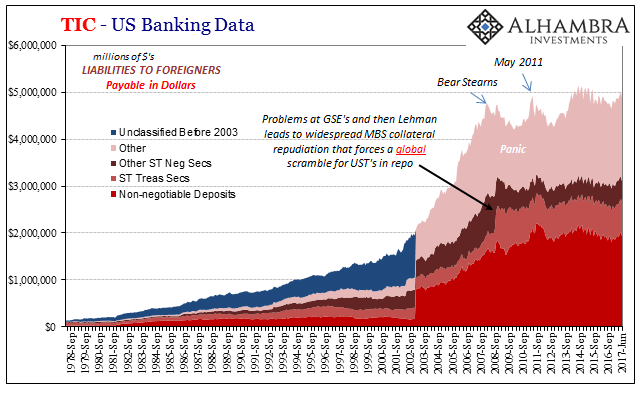

Balance sheet mechanics. There are funding considerations, too, including repo fallout especially in the full-scale repudiation of any and all private label MBS, but more than that banks needed highly liquid, repo-eligible paper that did not explode their balance sheets (what you see below being forced to reverse).

The combination of UST’s plus agency securities, even those with the GSE’s in restructuring, were highly attractive not on a return basis but the far more important survival one. It’s the perfect example for how the eurodollar system turned itself upside down; before 2007 everyone really believed in riskless return and so massive expansion was prioritized over everything (reduce as much as possible the operating liquidity cushion in agency and UST holdings); after 2007, what is considered is returnless risk, where liquidity preferences continue to drive bank considerations no matter what the Fed does or Economists say about the economy and markets.

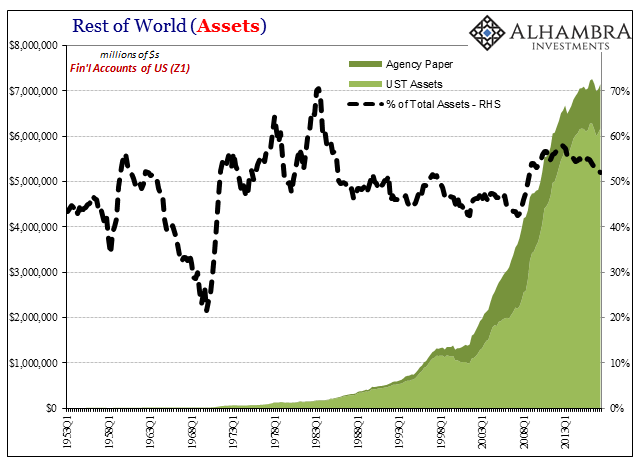

The domestic banks are only one part of the equation. In the modern banking system of the eurodollar, global banks matter as much if not more than their onshore counterparts.

They, too, hold some manner of liquidity cushion though one that had been more constant during the bubble years. That may be because for our purposes here, using the Z1 figures, the statistics do not break down into official and non-official capacities. An overseas central bank is more likely to hold its “dollar” “reserves” in the form of safe and liquid instruments like UST’s and agency debt than offshore private banks operating in eurodollars.

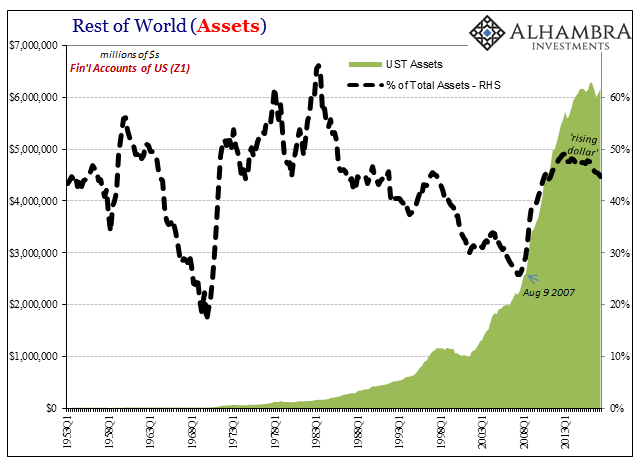

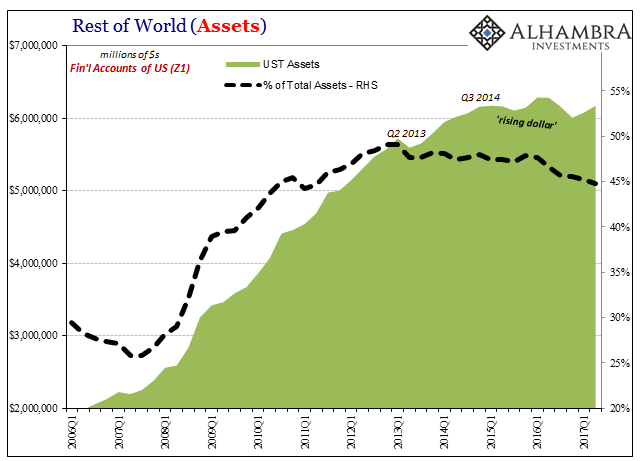

In terms of UST’s alone, foreign banks have been buying them as fast as they possibly can. Again, this is not regulation taming previous reckless behavior, it is the global monetary system coming to terms with its past bad assumptions by force of ongoing systemic illiquidity. In the early eighties, foreign institutions held two-thirds of their credit assets in the form of UST’s; by Q2 2007, that proportion had fallen to one quarter on the basis of agency paper steadily gaining favor as eurodollar finance spilled out in one form as a US housing bubble.

Domestic banks may have been fine with what happened at Fannie and Freddie, but foreign firms and central banks were not. They sold out and a great deal of it was transferred right onto the Fed’s balance sheet due to its various QE schemes dedicated to the MBS sector. Without agency debt for their liquidity assignments, that’s why they increasingly turned to UST’s. Between 2007 and 2013, they went from one quarter of all ROW credit assets held in them to one half.

In other words, there was a hell of a lot of pressure on the UST side to support the continued fluid operation (collateral flow) in funding markets like repo (as well as collateral in FX) as well as to provide a liquidity cushion as a matter of altered behavior (enhanced by regulation). And most of it was coming from the overseas portion of the “dollar” markets.

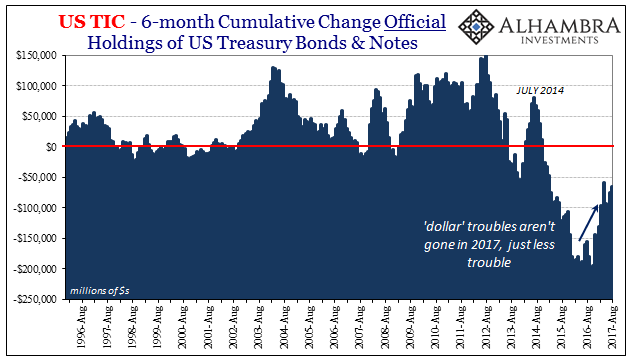

Starting in the middle of 2014, this “rising dollar” period, the ROW sector began selling very heavily out of their UST holdings. Rather than lead to higher yields on them as Economists had steadily projected, the opposite occurred.

Part of the problem here related(s) to interpretation, meaning who was actually selling and why. Again, the Z1 statistics combine official and private activity together whereas something like TIC does not.

This kind of collateral tightening is beyond the grasp of Economists, even those who work at Primary Dealers. Banks particularly offshore private firms may not be buying UST’s because of purely economic considerations, but it doesn’t really matter in terms of the price. In other words, you can try to make the argument that yields are held down by these technical matters and therefore on economic grounds alone rates “would” be higher than they are, therefore proving Economists right to some degree in their theory and projections (and so the matter becomes one of timing).

Except that UST buying as a matter of collateral (as well as balance sheet factors) is an unambiguous measure of tight money conditions (something we know especially in the “rising dollar” period for why foreign officials were “selling” their UST’s so heavily), which is consistent with reduced future economic opportunity and therefore lower overall nominal yields. It is one mechanical property for how markets end up pricing the interest rate fallacy.

Constant perhaps overburdened UST buying for these reasons (including FX collateral) isn’t some artificial injection to set aside as “transitory”, it is instead (one of) the means to the end; one that Primary Dealer Economists don’t understand that their traders do in practice even if those traders don’t completely appreciate from an individual basis what that might mean in the big picture monetary context.

Stay In Touch