The TIPS market corollary to interest rate case impatience is overhyping any round number that might in isolation appear to confirm the bias. To reiterate the mistaken assumption: if you believe that economic growth just happens, then given how much time has passed since that was true or apparent you have to believe each long end selloff is the one that you’ve been waiting for. The result is an almost comical overreaction to regular market action; nothing ever goes in a straight line but nowadays the smallest moves are described in the most epic terms.

For inflation expectations, I’ll let the Wall Street Journal hype the latest apparent signal of superlative significance:

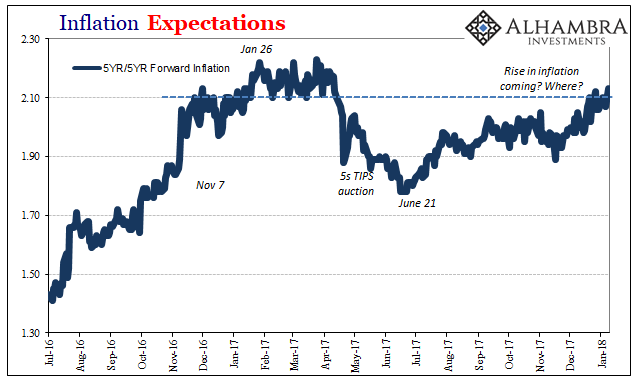

A measure of the bond market’s expectations for inflation crossed a key threshold in the past week, highlighting investors’ renewed economic enthusiasm.

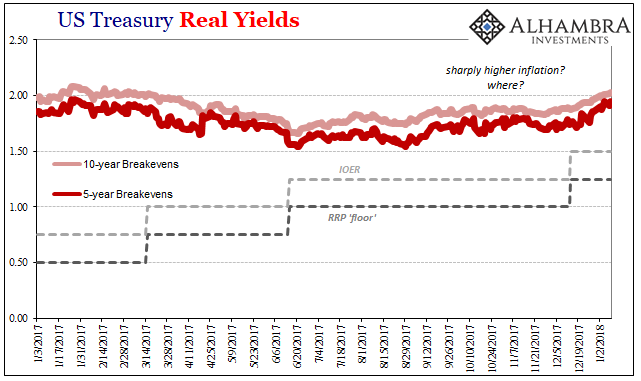

The 10-year inflation break-even rate, which reflects the yield premium on the 10-year U.S. Treasury note over the comparable Treasury inflation-protected security, topped 2% on Tuesday for the first time in more than nine months, according to Thomson Reuters. It settled Friday at 2.027%, its highest level since March 16.

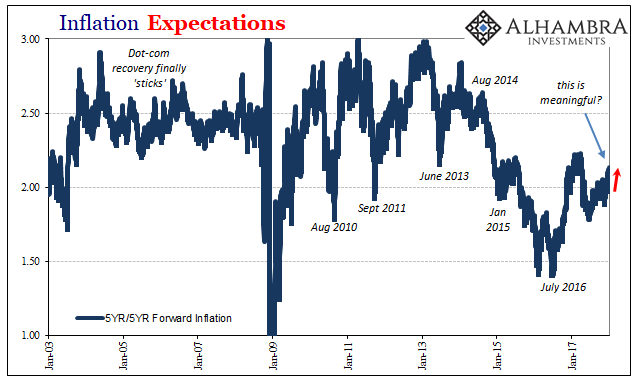

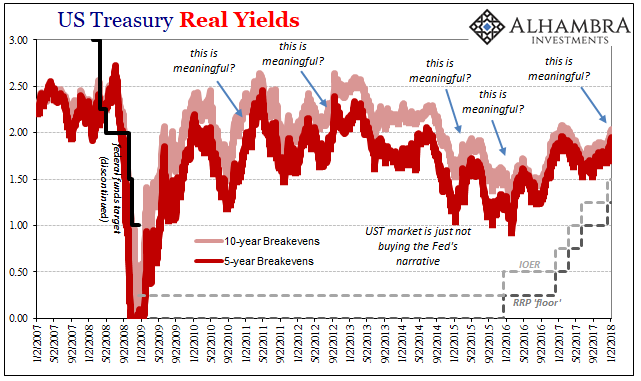

Why is 2% a key threshold? In truth, it’s mere trivia but made out to sound momentous because “the first time in more than nine months” seems really impressive – until you see it in context. Even the shorter-term view fails to dazzle, or even compel all that much, let alone its minute stature in the longer view.

That’s ultimately a huge problem for analysis like this. It fails, doesn’t even attempt, to explain why crossing 2% for 10-year breakevens is now significant in a way that any of the past and far more intense increases in inflation expectations weren’t. In other words, if 2% means something in January 2018, what changed to make this one different from all those other times before, most if not all reaching far higher than 200 bps?

Inevitably, the only (honest) answers you might get back are what I wrote above, that enough time has passed surely healing all economic wounds by now and leaving the world finally ready to resume its normal place, or the related idea that “rate hikes” mean something.

The latter is at least a reason, but that doesn’t mean it’s a good one. After all, if monetary “stimulus” failed to stimulate any part of the economy (not even housing is anywhere near its historical let alone precrisis condition), why would its removal declare anything other than its removal?

Stay In Touch