NOTE: This is really the second half of an earlier missive on the changing nature of the eurodollar system post 2014-16. While it’s not absolutely necessary to read the first here, it’s probably a good idea.

The reason nothing ever goes in a straight line is that first everything is always changing. How and why are questions we often don’t have good answers for. And not only that, how we respond to changes expected and unexpected is really nothing more than the messiness of the scientific process, trial and error carried out on perhaps the grandest human scale.

So it is with the monetary system. The eurodollar has never stood still. Even over the last ten years, in decay it has remade itself time and again (and again?). Just when you think you have it clocked (literally), something changes and you’re left searching for new cues and clues – and trying to make sense of what these new facets mean.

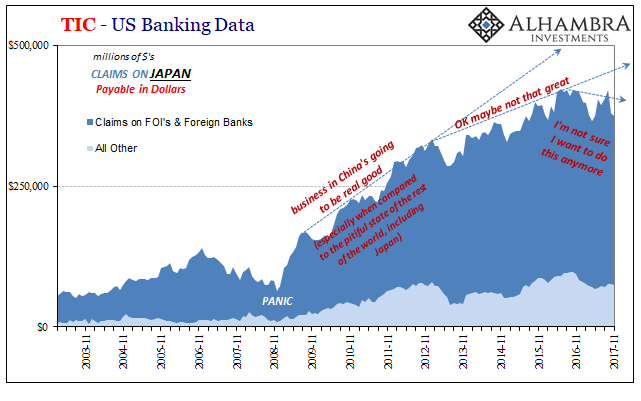

The most prominent alteration to the systemic dynamic since 2007 (with a clear break at Bear Stearns) has been the removal of European banks, and their partial replacement by Asian counterparts, primarily Japanese. The way in which European banks supplied “dollars” was not quite the same as the way the Japanese would come to. Not only did the eurodollar become more Asian, it became more derivative, more FX in operation.

One reason for that is European participants in this credit-based monetary system were never shy (precrisis) about creating “dollars.” Whether Swiss or British, Deutsche Bank or even Unicredit in Italy, dollar liabilities were added on an ex nihilo basis at the margins the minute whatever firm saw any trading opportunity – governed, as always, by risk vs. return.

The Japanese are different. Operating more so on what was once called “hub and spoke”, Japanese banks particularly after 2008 conducted more of a redistribution regime. In other words, owing largely to the Bank of Japan’s post-crisis affinity for multiple QE’s, financial firms in that country had an excess of yen (bank reserves) and nothing to do with them (defeating, of course, the idea behind QE).

This was the real carry trade, where a Japanese bank overflowing with bank reserves in yen would swap them into dollars because risk-adjusted opportunity was with dollars. Not in America, of course, nor really in the other developed and Western economies, but across particularly the Asian world in the aftermath of the Great “Recession” the EM’s still needed “dollars” and everyone just knew their growth model was left intact.

Thus, this Asian “dollar” required a lot of FX to mobilize as well as an almost 19th century kind of banking process to complete it. Before the modern bank, the one possessed after 1995 and RiskMetrics with quantifying everything, lending in particular was done on a personal basis. The local country bank did business with other businesses in the area because that bank’s officials knew personally, and made it their mission to know personally, what their customers were doing, how they were doing, and why they might need or not need the bank.

Try as it might and often as it claimed, there was one country in Asia that while attempting to modernize along Western lines has resisted often vociferously foreign penetration. In banking terms, that meant the kind of in depth mathematical risk profiles were harder if not impossible to conduct. Chinese financial firms remained somewhat of a mystery even in 2009 just as the rest of the world would come to depend upon China economically for everything in this “new normal.”

Japanese banks, however, were doing quite a lot of business with Chinese firms in large part because the old keiretsu model of conglomerate integration while reformed still held. As I wrote back in December 2015, the moving of Japanese production capacity offshore had financial ramifications, too, particularly where a lot of that capital flight ultimately landed:

Much of that, as I have chronicled over the past few years, has ended up in China. That suggests that as Japanese formerly keiretsu penetrated further into mainland China, they likely brought with them their banking “core.” At the very least, Japanese banks with close ties to these offshoring Japanese firms were likely introduced to Chinese industrial counterparts.

A match made in eurodollar, or Asian “dollar”, heaven. The Japanese banks, stuffed with yen bank reserves, were in close contact with the Chinese who, by the way, were in desperate need of “dollars” because they were still going to have to finance that economy’s return to its “miracle” growth levels. Without European banks to supply them, the Japanese stepped right in – paying what had become a structural premium for harder to source (post-crisis shortage) swaps largely from American firms in order to cash in on awesome Chinese opportunity that largely eluded everyone else.

The bedrock assumption behind all this was economic in nature; as always, risk versus return. The rest of the developed world was after 2008 all risk, no return. China in particular looked like the exact opposite. Until the cracks started to appear around 2012.

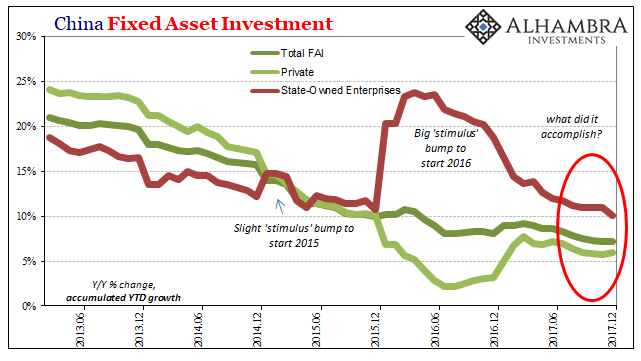

So much of Chinese debt and leverage, internal as well as external, was originally written under vastly different assumptions. If you believe that the Great “Recession” while global in nature was still a recession, then 25% export growth is your baseline assumption for how you view financial considerations. That includes so-called hot money as well as, more importantly, interbank lending. If Private FAI is booming along at 30%, there isn’t likely much credit or liquidity risk.

But if pre-crisis growth doesn’t come back, or, worse, starts to look like it never will, all those prior transactions have to be revalued. The risk profile changes dramatically, moving toward one without a lot of upside, the very sort of re-evaluation that hit the West hard during the crisis. This is why for the EM’s the “rising dollar” of 2014-16 was their 2008.

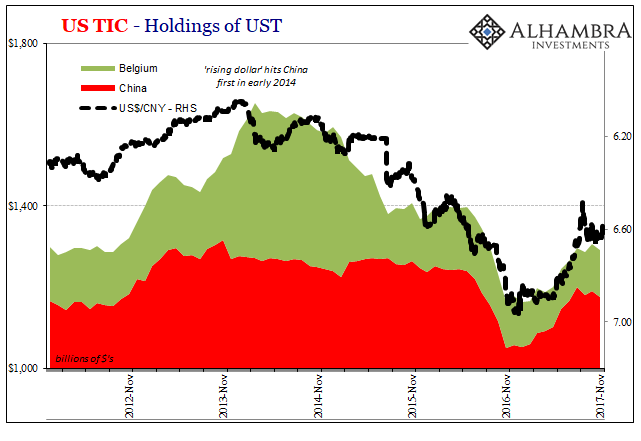

Quite rationally, Japanese firms decided to reassess their piece of the dollar-yen carry trade – leaving in the balance China to source “dollars” elsewhere. That Japanese withdrawal happened to occur during an overall worldwide bout of illiquidity (obviously contributing to it). The effect was Chinese banks increasingly uncovered, left to obtain “dollars” at whatever price they might be charged from wherever they could find them (including the PBOC “selling UST’s”).

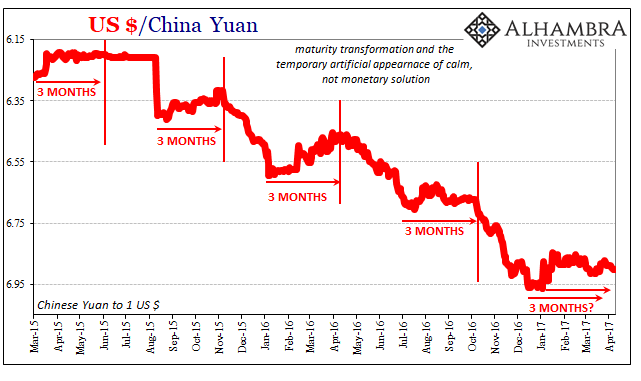

That price, lower CNY, reflected increasing risk (credit as well as liquidity) as an economic case. It became so clear and obvious that, as I wrote above, it was for China easily clocked.

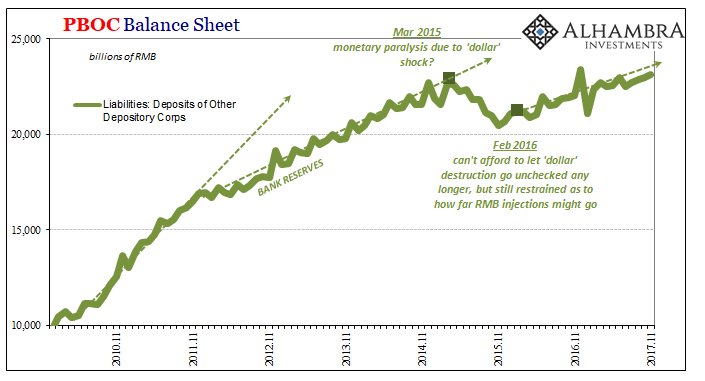

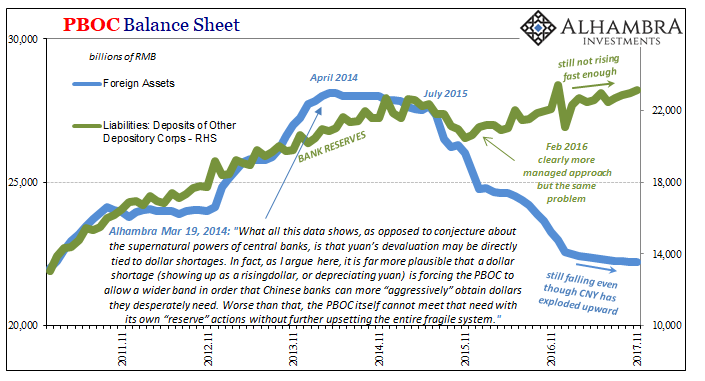

But the Chinese didn’t sit idle and watch their monetary system go down the drain, taking their economy with it and threatening to upset the entire social structure. OK, they did at first, but after enough punishment was inflicted by the “dollar” they finally in January 2016 responded. Using first the textbook approach, they did massive fiscal “stimulus”, stuffing an enormous amount of (likely wasted) construction activity through State-owned channels. In addition, the PBOC completely reversed course, opting for a more direct RMB increase on its balance sheet to try and offset the persisting, relentless “dollar” drains (not just those emanating from Japan).

None of it worked. Though the Chinese economy found some “reflation” it was hollow. An organic rebound from the 2015-16 downturn with clear and obvious momentum just never materialized. CNY kept to its regular clock and by the end of 2016 it was still falling.

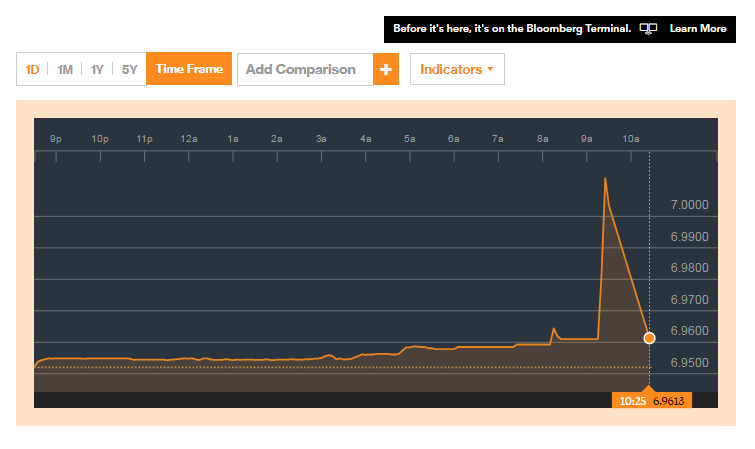

On December 28, 2016, the Chinese currency experienced a flash crash, blasting below 7.0 to the dollar. A shocked PBOC responded by denying it had ever happened, even though it appeared on every screen in the world. It’s the most openly desperate central bank episode I’ve ever witnessed. How bad do you have to believe things are if you feel it necessary to flat out reject reality?

I have come to believe that’s the moment Chinese officials decided there weren’t many other options left. They had flirted with Hong Kong before, earlier that year during the worst of the “rising dollar” that January. And they kept at it later in 2016 with lower level activity.

From China’s perspective, something had to be done about CNY because nothing else was working. To get a handle on the currency meant to get their hands on offshore “dollars.” They couldn’t keep using their own “reserves” because it publicly confirmed the lack of success and power (and kept CNY to the downside).

Hong Kong banks were more like Japanese banks in the “dollar” business. They were not, for the most part, creators but redistributors. For this to work, the Hong Kong banks had to source “dollars” from somewhere else. But where?

No matter how this all turns out, it has been to this point impressively innovative and creative. It would be a shame if it doesn’t work, and I don’t believe it will, because there is a lot to admire about what took place here in 2017.

The Chinese problem was in general terms quite simple. Chinese banks had lost their marginal outlet in Japan because Japanese banks viewed them (with, again, good reason) as increasingly risky propositions without the upside they had once believed was an almost guarantee. That risk profile was shared by more than firms operating out of Tokyo, which accounts for the full scale of CNY’s decline.

So, from the perspective of Chinese monetary authorities, if your own banks are not acceptable to global “dollar” markets without having to pay huge and disruptive premiums for eurodollar funding, why not substitute more pristine banks for them in the same process? That’s basically all that happened, whereby Hong Kong banks were placed out front to obtain the “dollars” they could get at better prices because of Hong Kong’s (to this point) sterling reputation. A second step, or backchannel, and by all accounts a very creative one, was then opened to China’s banks.

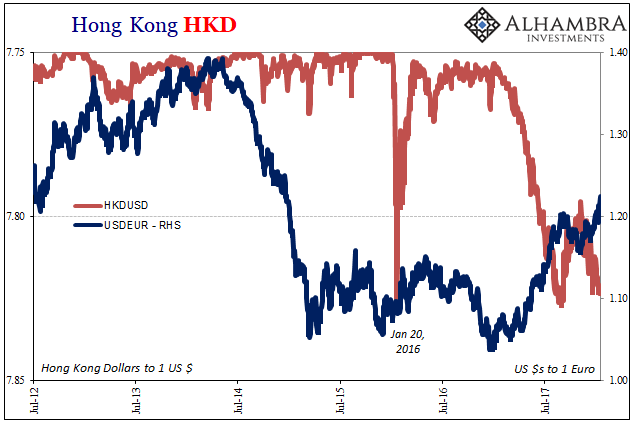

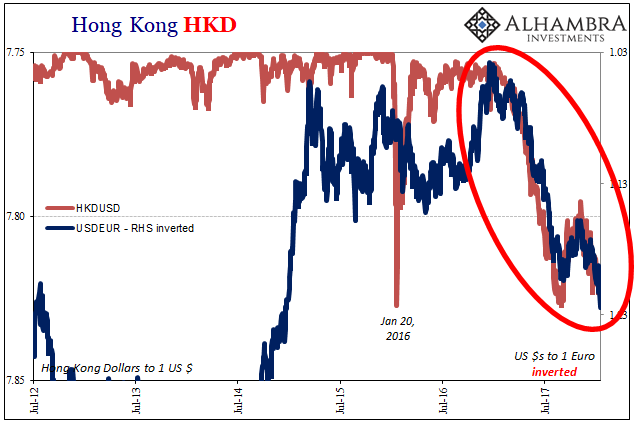

With Hong Kong out front instead of China, that would have made the risk/return calculation more palatable to where such things really, really matter. Such as Europe:

When I look at the chart above, it stands out immediately, crystal clear in not just the relationship but what that relationship means in this very context. In case you aren’t as obsessive about graphics in the way I am, here it is with the euro upside down and rescaled to just the past few years:

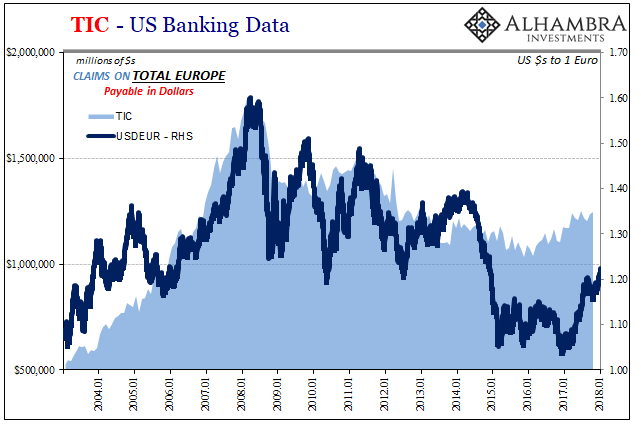

I think it’s pretty obvious who it is has been on the other end of Hong Kong, therefore China. We can add some additional layers to the interpretation, using TIC data, for example.

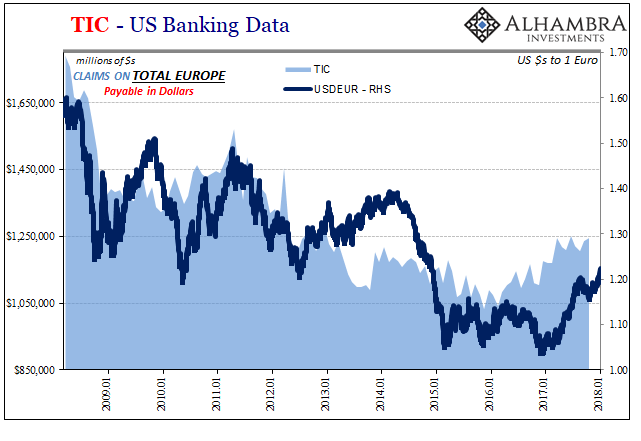

Making some minor adjustments, focusing especially on the period after Bear Stearns, really puts it in focus.

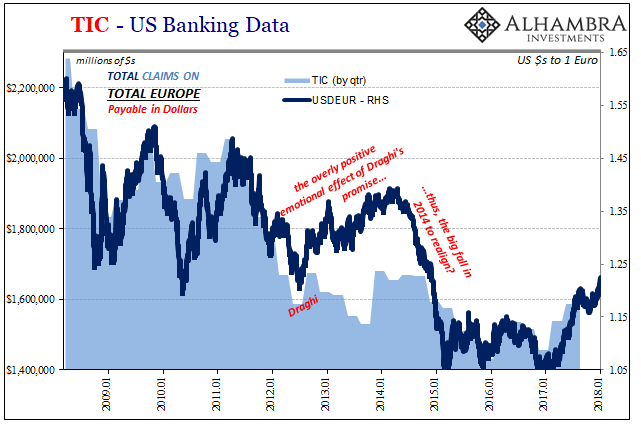

And to really drive the point home, I’ll use the more comprehensive quarterly TIC figures that in addition to banking liabilities (in dollars) include offshore currency components as well as dollar claims of US customers on European banks:

I know that’s a lot, so here’s the short version summary: Japanese banks withdrew from China forcing China to stand Hong Kong in for them so as to get Europe back in the dollar business. Writing something like that really reinforces the difficulties here, particularly given that the mainstream still views currencies and money as if none of this exists. Central banks in the orthodox convention are, well, central to their own game.

All these movements and correlations, however, show that’s just not the case – the euro in particular, as demonstrated above. It really is just simple supply and demand dynamics, only that what is being supplied is “dollars” outside of official boundaries. This is an offshore monetary ecosystem that means more than any dozen or two QE’s all strung together. It’s credit-based, therefore banks and bank balance sheets first and foremost. Because there is no scrutiny, no official acknowledgement, it’s all hidden and therefore only comes out of the shadows through this kind of ex post facto piecing together of price movements that at first sounds plain ridiculous.

What are the implications of HKD and EUR?

The most immediate is, obviously, the weak dollar. We can see very clearly what’s behind it, and to anyone viewing DXY or USDEUR in isolation this all looks suspiciously like “reflation.” It appears as if good and positive things are happening, the kind of prices and indications that might ceteris paribus suggest more positive outcomes. Throw in rising CNY, which is as a result of all this, the world does start to look a whole lot better (relatively).

The greater implication is a more universal one, given that what has happened tells us a lot less about what will happen than you might think. Europe is back to doing a little in the dollar business (US$ swap spreads decompressing are one effect), but why?

If I agreed to lend you money in the past at very favorable terms, and then refuse to do so at rollover because I’ve judged the risks as being greater, you might offer then to put up collateral as an additional assurance. That is, in fact, perfectly natural, and the common progression of risky credits.

But it’s not a perfect substitute, and though I may now lend to you on collateral, I may not give you all the money you ask for. Not only that, it further changes a whole bunch of things sometimes in ways we don’t often appreciate (you can’t use that collateral the way you once did). It’s an additional constraint.

In one important sense, that’s just what China did in 2017. They were rejected on their prior interbank basis given the greater economic risks that despite mainstream rhetoric otherwise everyone operating in these markets better appreciates. So they offered Hong Kong as collateral.

The response in Europe was somewhat favorable to the proposition, to pick up some of the slack in “dollars”, but only some. And it’s causing HKD distortions along the way (now a triumvirate of CNY/HKD/EUR, with HKD on the losing end). Furthermore, given when all this started, I have to believe that underpinning Europe’s apparent generosity are first a whole bunch of trading premiums we have no idea about (is someone, PBOC, subsidizing somewhere along the way?), but more so some further risk/return assumptions that may not last all that long.

In other words, when EUR started to rise as more “dollars” flowed out from the continent (and not just to China via Hong Kong) they did so under “reflation” expectations. China in particular was at the end of 2016/beginning of 2017 thought to be accelerating as the key basis for “globally synchronized growth.” What if that doesn’t happen? Will European banks, though back in dollars but reluctantly so, keep on supplying through Hong Kong? How might they respond if Hong Kong starts to get a little dicey (HKD) itself?

We are, in essence, asking the very same questions that eurodollar participants have been asking about other factors at various points (2008, 2011, 2014) over the last decade. The answer to all those questions have so far been uniformly negative. Is this time different? Does the Hong Kong bypass, lovely and elegant as it has been, provide a lasting solution where all those others haven’t?

There’s a whole lot more that we don’t know, or that I could offer as pure speculation. This is all, of course, just inference to begin with. They call it shadow banking for a reason, though I don’t think even “they” knew in the slightest the full extent. It’s a real handicap to analysis that we always have to bear in mind.

Still, as any community banker will tell you, if your borrower has to do increasingly odd things to pay you back, even if they can post some collateral along the way, it’s not a good sign. At some point the boom has to boom, risks have to have a plausible payoff for it all to continue.

Stay In Touch