China’s shock “devaluation” was not the only one in 2015. It was the currency disruption that most people remember, even if years later they’re not sure exactly why. Paying attention to CNY makes sense, requiring no further explanation for why it might be given focus even from the otherwise unaware.

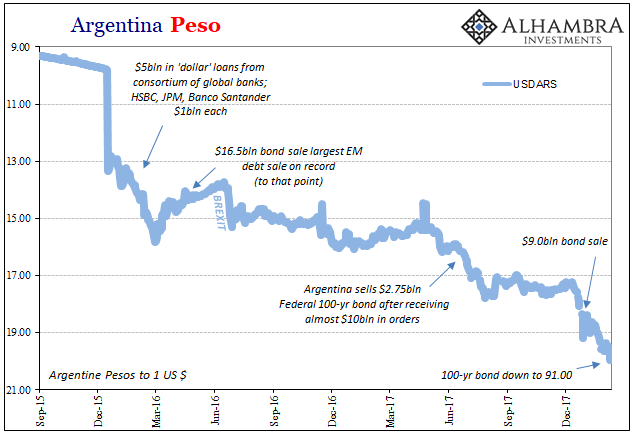

In December 2015, while global liquidity conditions further deteriorated the Argentine peso was likewise beaten down dramatically financial trading. From 9.803 pesos to the dollar on December 15, it was 13.33 two days later. The timing was, as usual, attributed to Janet Yellen and the first “rate hike” in the United States. Psychology is not unimportant, but as I wrote about a month before, this was something else wholly unrelated to the Federal Reserve’s clear confusion:

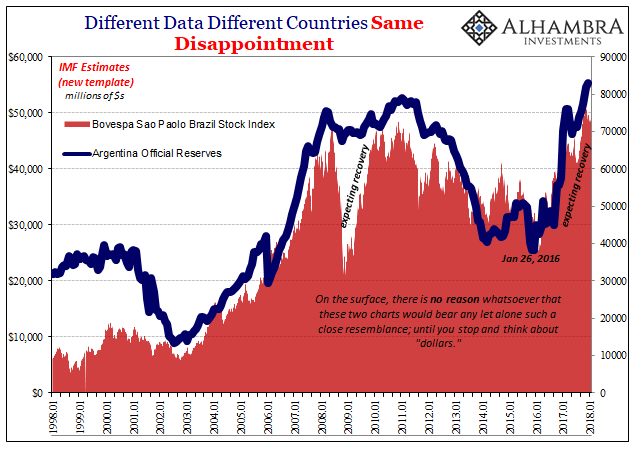

Like Brazil’s international financial experience, it looks like a “dollar” run and quacks like a “dollar” run. As we know from the second chart presented above, there aren’t any private banks as counterparties here, foreign or domestic (not that a domestic bank could even think to provide “dollars”), which raises an intriguing question – which central bank in the world is “on the hook” providing long derivative instruments (the counterparty to Argentina’s short derivative instruments, likely swaps and forwards, shown immediately above) and thus “supplying” “dollars” to Argentina in 2015? For almost any country, these are enormous sums; projected repo flows of -$12 billion and short forex of $15.3 billion speak to not just your everyday financial imbalance even in this swirling world of 2015.

Like China, Argentina got caught up in the “dollar” run or squeeze. It finally came to a merciful end in late February 2016, several weeks after the global illiquidity reset in worldwide liquidations.

Over the two years since then, Argentina has been busy in the Eurobond market. As the name implies, Eurobonds are the offshore brother of eurodollars; the former as tradeable securities drawn from existing savings, the latter credit based created, and destroyed, by bank balance sheet factors.

Therefore, in one sense it made great sense. Just as US companies during the worst of the Great “Recession” began borrowing hand over fist from the bond market in lieu of bank credit collapsing, the “rising dollar” pushed many countries and the corporations (and governments) inside them toward bonds as an alternate funding mechanism. These are not substitutes but in many cases a last resort.

For Argentina, it started with a bang. On April 19, 2016, for the first time in a decade and a half the nation was able to source global bonds. The legacy of old default was finally put behind, and a then-record (for EM’s) $16.5 billion was floated to equally impressive demand. In this day and age, there is no memory when a few hundred additional basis points in yield are in line.

Having reestablished this “dollar” conduit, Argentina has been back several times more. This past June, they even managed to sell $2.75 billion of a 100-year bond. As if the country weren’t some dangerous credit, brokers booked about $10 billion in orders for that sale.

It hasn’t been limited to federal authorities, either. Local governments equally starved of financing, especially in “dollars”, have been selling bonds left and right. Through February 2017, it was estimated that the country’s 23 provinces as well as the autonomous city of Buenos Aires had issued nearly $8 billion in debt of their own.

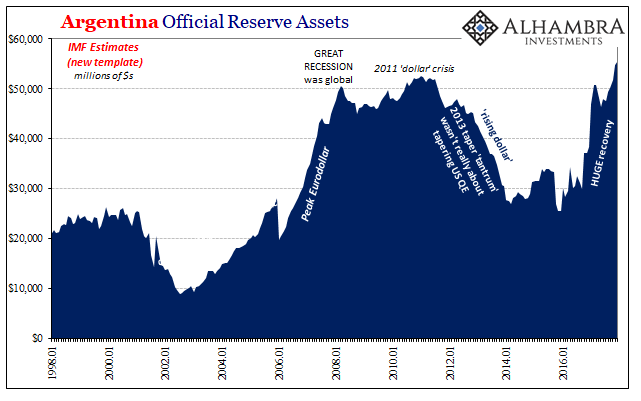

Having been built spectacularly during the middle 2000’s like other EM’s on the massive monetary expansion of the eurodollar system, the several crises beginning in 2007 had first arrested the increase in Argentina’s official monetary reserves so that by 2013 things were going in reverse – economy from money.

This 2016-18 debt binge has had the practical accounting effect of refilling Argentina’s lapsed reserves. In latest updated IMF figures, they have recorded a record level as of December 2017. Congratulations all around?

Obviously, something’s not right. All throughout 2016 and early 2017, though “dollars” were flowing back into the country, the Argentine peso never really rebounded. There was an initial snapback higher, but from Brexit until April and May last year the best for the currency was stable to slightly lower. By the time the 100-year bond was celebrated as a great financial feat, the peso was sinking again.

Though more extreme than others, including its South American neighbor Brazil, the post-“rising dollar” period has been less recovery in substance than narrative. It’s as if one had been booked ahead of time as if a guaranteed outcome. The fact that Argentina like other EM’s was an EM seemed to have meant to “investors” the high prospects for huge profit.

This was the operative paradigm for decades before 2014. If one, or many, EM’s got into trouble, they would rise out of it in spectacular fashion. The old mantra of buying when there is blood in the streets is applied to risky areas first and with greatest enthusiasm. If the downturn was over, then the upturn provided, it seemed, an opportunity unlike anything seen since 2009.

Bond buyers, however, may have made several crucial miscalculations. The first is assuming prudence, meaning that chastised governments will act upon being let back in with restraint and caution. There is no reason to believe that has ever been the case, and quite a few examples, including Argentina 2016-18, where once the shackles are taken off it devolves quickly into a free-for-all.

The second and greater missed assumption is the baseline over which all these things take place. How many times have we now witnessed the reversal of sign as being interpreted as something far more strenuous and sustainable than turns out to be rational? Argentina’s part in the crisis ended, so everyone naturally assumed the recovery from it would be as spectacular as the severe downturn (symmetry).

The fact that the country was able to sell so many billions in bonds rather than raise red flags actually further reinforced the circularity; the more it looked like the crisis was over the more bonds they sold, and the more bonds they sold the more it looked like the crisis was over. No one stops to check assumptions under such FOMO.

If there is an ironclad law of “dollar” gravity over the last lost decade, it’s that wherever the eurodollar strikes the victim is left worse off than before. Symmetry is repeatedly violated. We find time and again where a downturn takes place followed by mere positive numbers, an upturn in the technical sense only and one truly and dangerously devoid of necessary momentum to get out of an “L” and into the “V” always taken for granted.

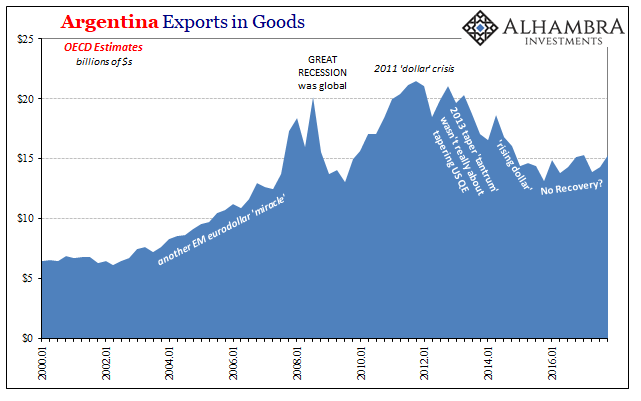

There aren’t a whole lot of reliable statistics about the Argentine economy. Much is black market and skewed. The OECD, however, does track the country’s trade dynamics, particularly its export sector vital to the overall economic baseline. The pattern is an all-too-familiar one, especially what’s at the far right on the chart immediately above – meaning what’s not at the far right.

Though billions upon billions have been added to reserves, and debt overflowing freely, there really hasn’t been a recovery. There is growth indicated by a plethora of positive numbers, but as we know that doesn’t mean it is growing.

That’s a problem for many reasons, not the least of which for any system taking on enormous leverage in anticipation of actual growth. Argentine bonds have in 2018 sold off, as the peso drops precipitously once more to (and today past) 20 to the dollar. As stated above, “something” isn’t right.

What you get in the mainstream description of it is the farthest from helpful:

The selloff in U.S. equities is seeping into other markets globally as investors pull back from riskier assets. At the same time, the peso has fallen to a record low against the dollar amid growing concern that the central bank is under pressure from President Mauricio Macri’s administration to pull back on its fight against inflation.

No. Argentina is, in fact, a pretty good if more extreme example of what’s been taking place over the past few months. Lost in this current euphoria about inflation and “globally synchronized growth” has been several troubling developments in money and global “dollar” liquidity; an escalation as I’ve called it several times since September (I think global stock market liquidation qualifies easily as the next step in the line).

In 2016, for the first time in several years there was a shift in sentiment and outlook from only the downside risks to more and more what looked like a possible upside. Outside of mainstream rhetoric, the more 2017 passed it seemed instead quite limited in that direction. That didn’t stop the financial insanity including EM bonds and stocks, but in the shadows there has been a shift back toward examining downside risks again.

Thus, we have the unappealing scenario of achieving but 2014-levels of economic growth with 2011-style expectations for it. There are a lot of places where it is, and has been for some time, just at such an extreme. US stocks are almost tame by that comparison.

To begin this year, Argentine President Mauricio Macri authorized the government to issue another $15 billion in Eurobonds in 2018. The government had previously stated that it required $30 billion in total financing, of which 40% would have to be floated in foreign currencies. That’s the problem with leverage; once it starts it never ends especially when it can be so easily sold on promises for tomorrow’s economy.

Some parts of the global monetary system, and therefore liquidity, are beginning to wonder if tomorrow might instead end up looking too much like yesterday: way too much debt and not nearly enough, if any, growth.

Stay In Touch