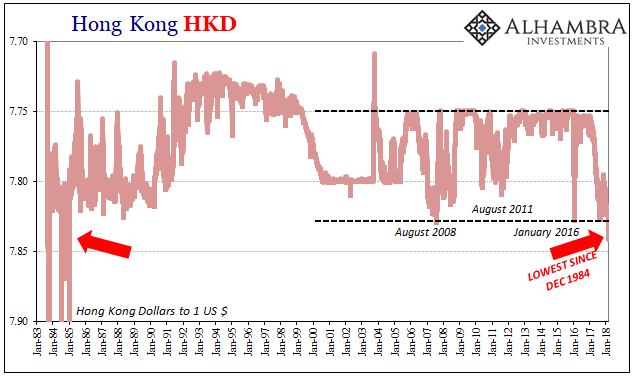

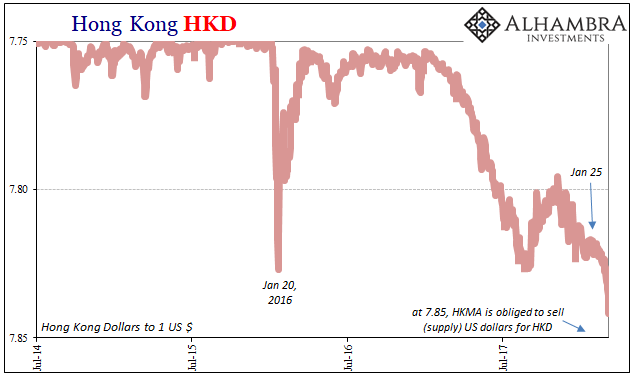

The Hong Kong dollar is a hair’s breadth away from a currency crisis. Plummeting over the last week or so, the exchange value crossed 7.84 today. At 7.85, the HKMA is required to sell US dollars in order to buy up HKD. That may be just what Asian banks are looking for, some other US not HK dollar supply.

In predictable fashion, monetary officials in Hong Kong publicly claim to be unconcerned. This is all, they say, just an unwinding of the fear trade. HKD has been rightly viewed as a safe haven for reasons of stability and predictability, so as the world gets back to normal under this globally synchronized growth paradigm there should be outflows from Hong Kong. The result, HKD weakness.

Since the global financial crisis, we have seen large amounts of funds flow into Hong Kong, and now we are seeing these same funds flow out.

Howard Lee, Deputy Chief Executive of the HKMA, Hong Kong’s monetary board that acts in lieu of a central bank, sounds pretty confident. As I’ve stated elsewhere (subscription required), I don’t doubt that he actually is.

Central bankers over the last eleven years have been good at two things; taking price movements in the exact wrong way while at the same time convincing the media to sell the world on how what suggests a warning instead projects confidence. George Orwell was writing about Economists, it seems.

The last time we could make a similar analogy was gold in 2013. Then, as now, the price decline was widely broadcast as an end of the so-called fear trade or fear bubble. In keeping with global economic reflation of the time, it appeared to suggest that markets were aiming for the same scenario right where you would expect if it was a real thing.

Of course, that’s not what happened because that’s not what drove the gold price lower. Gold’s crash was a warning, another “dollar” related irregularity (collateral) about what was coming later that summer and then more so over the next few years (“rising dollar”). The global monetary system wasn’t loosening up taking on risk, it was doing the opposite where banks (the true suppliers of global “dollars”) were getting out of the money business, creating escalating havoc along the way.

Hong Kong officials can act as they please, of course, just as US and European policymakers have time and again been similarly caught looking in the wrong direction. The difference for the HKMA is 7.84 (FX rather than collateral irregularity). There is no margin for error left in a currency that is supposed to be stable and predictable. Required support from the monetary board isn’t that at all. What’s left will be the expected blame poured upon those evil currency “speculators.” That’s almost certainly next.

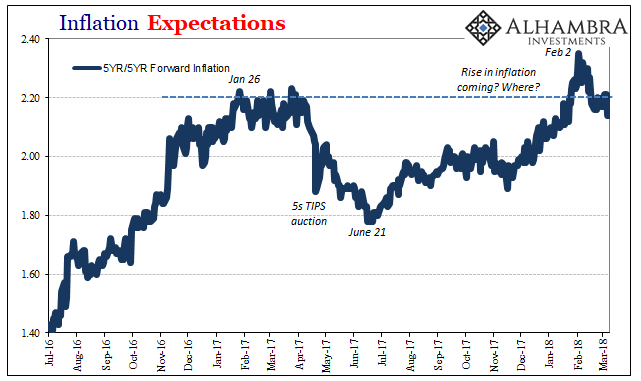

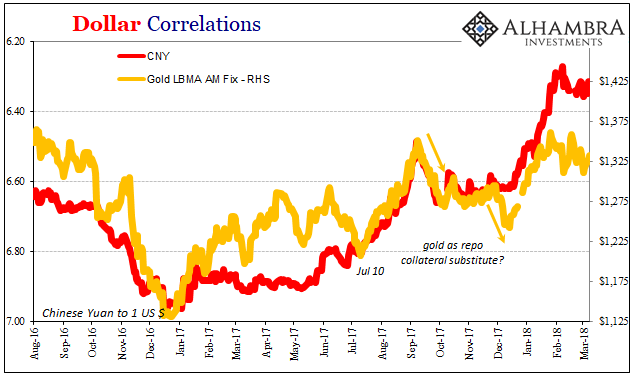

There are a few interesting correlations, including the sudden reversal in things like inflation expectations (not mention CNY itself). The global stock liquidations at the end of January spilling over into February coincide with HKD’s most recent downturn. Prices (like gold) that were surging last year on reflation (related to CNY) aren’t anymore. That includes both copper and crude oil since early February.

These important market indications of global “dollars” are on edge, more than a little unconvinced by the likes of Howard Lee. Then again, what was he ever going to say? It’s what they always say, even though it never seems to turn out that way. With 7.84 breached, 7.85 is now well within reach. The “speculators”, I’m sure, are well aware.

Stay In Touch