In June 2008, ICAP actually launched a US-based alternative to LIBOR. It ended up as nothing more than one very minor footnote lost in a sea of more pressing problems and events. Still, that they even tried is somewhat significant and relevant to today.

Before the whole cheating scandal came out, there were questions surrounding just what LIBOR was indicating. The major difference for this upstart New York Funding Rate (NYFR) was it as a mid-rate rather than an own-rate. In truth, this wasn’t really much of a distinction at all, but at the time it seemed important to certain people (at ICAP, apparently, encouraged by others).

Though it was a New York survey, they were still interested about conditions in the eurodollar market (though I still can’t figure out how and why nobody ever seemed to appreciate the full ramifications of what that meant). At odds was the feeling banks handing in their LIBOR panels to the British Bankers Association might have been shy about doing so because it reflected their “own” borrowing costs. Possible stigma about being more honest, and potentially making things worse, led some to suspect LIBOR wasn’t a true enough picture of funding conditions if individual firms were ever tempted to fudge.

NYFR would, in theory, fix that by asking participants what they thought any A1/P1 institution might be able to fund at during heaviest eurodollar trading early on in each New York session (while London was still going). This removed any potential stigma and for a brief time was thought to be a better unsecured notation.

If you are to specify exactly when the panic portion of the Global Financial Crisis began, surely it was on September 29, 2008. Global stocks markets commenced their crash liquidations that day, and given the significant events surrounding them the FOMC held another emergency conference call as all that started to unfold. Addressing things like LIBOR-OIS, Open Market boss Bill Dudley also noted:

MR. DUDLEY The NYFR index, which is the U.S.-based alternative to LIBOR, has actually been much higher than LIBOR over the past week or two. So LIBOR actually may be understated.

Subsequent studies have been noncommittal as to whether that was ever the case. In truth, it never really mattered. LIBOR was more than sufficient enough to tell policymakers: 1. They were failing; 2. Why they were failing; and 3. Where. Eurodollar, not dollar. Would it have mattered if NYFR had been suggesting unsecured eurodollar at another +20 to 40 bps over LIBOR? No. Not one bit.

LIBOR has several times been made into something of a scapegoat as if the Fed was occasionally implying it shouldn’t be held responsible because of bad information.

Even though LIBOR became further tainted in its fixing scandals, handing them another opportunity to decry its informational contributions, ICAP quietly scrapped NYFR for good in August 2012. They couldn’t find at least 12 banks willing to submit their thoughts on the mid-market unsecured condition; there was by then no more mid-market unsecured.

FRBNY in conjunction with other government bodies and banking groups has been since 2014 working hard to once again replace LIBOR. The Alternate Reference Rates Committee (ARRC) has come up with what they call SOFR – the Secured Overnight Financing Rate. This is derived from US$ repo funding backed by US Treasury collateral.

It seems a logical choice given that repo has effectively replaced unsecured interbank funding going back to 2007 and 2008. But that doesn’t mean unsecured rates tell us nothing, even though officials almost everywhere seem nearly possessed with disposing of LIBOR.

Which brings us to the current situation. Yesterday, I did it the polite way by saying they didn’t know what they were doing, and so they still don’t now. Today I’ll come at it with less inhibition as a way of declaring their statement purposefully full of sh–. The passage in question is the same one from the FOMC meeting minutes intentionally included as an official response to recent LIBOR-OIS, which I’ll reproduce one more time.

In short-term funding markets, increased issuance of Treasury bills lifted Treasury bill yields above comparable-maturity OIS rates for the first time in almost a decade. The rise in bill yields was a factor that pushed up money market rates and widened the spreads of certificates of deposit and term London interbank offered rates relative to OIS rates.

Understand what they are saying here. The FOMC is trying to claim that LIBOR is up because T-bill rates are; the latter are monetary equivalents. Bill rates are higher because of, purportedly, tax reform and the Trump budget. In other words, a heavier supply of bills at auction would lead to rising bill yields and therefore as money equivalents other money market rates would move up, too, including LIBOR.

That’s crap.

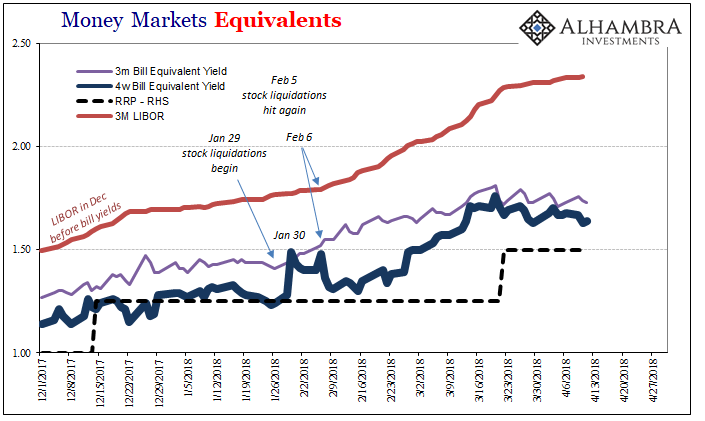

January 29 – stock liquidations start.

January 30 – 4-week bill yield shoots higher, from 128 bps near the RRP “floor” to 149 bps, a highly unusual single-day move.

Rinse, repeat.

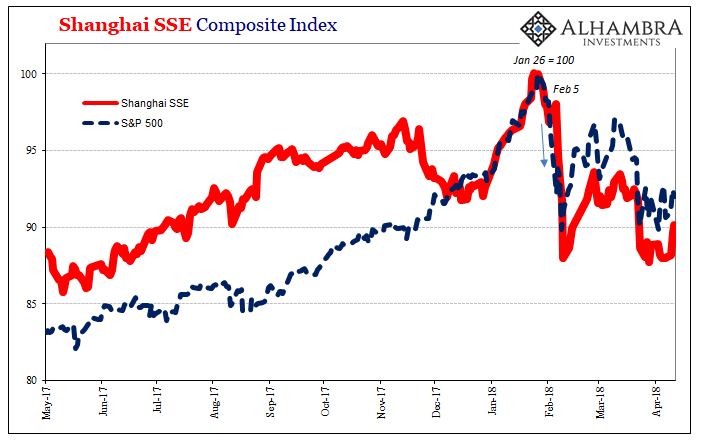

February 5 – stock market liquidations get serious.

February 6 – 4-week bill yield shoots higher again, this time to 148 bps.

Liquidations in stocks, liquidations in bills (by the way, who is it that holds and manages the largest stockpile of T-bills on the planet?)

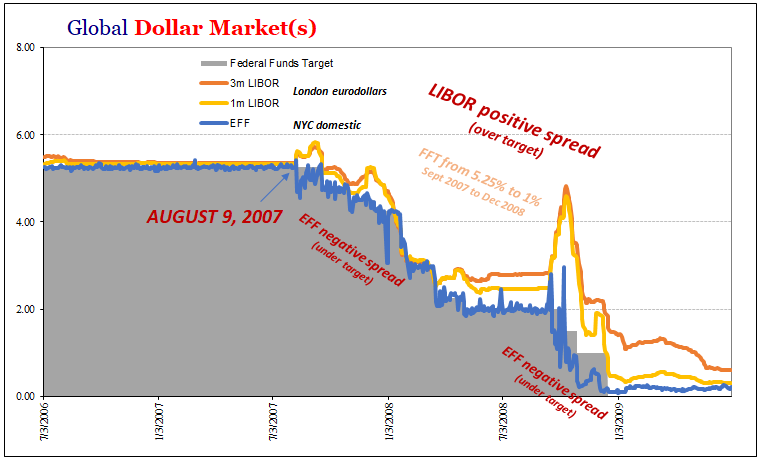

If we’ve learned anything from LIBOR during the crisis, and NYFR for that matter, it is that when higher spreads appeared it was due to liquidity risk rather than anything else. Credit risk, all that fuss over subprime, was blown way out of proportion. It was a pure monetary event, one described very well by the original eurodollar indication.

In other words, as you can plainly observe on the charts above, liquidations in multiple markets, spread out globally, led to a rising LIBOR spread which indicates, surprise, rising liquidity risk. Budget deficits? Come on. Seriously.

I have actually devoted (published tomorrow) yet another article (a third) just to this one passage because I think it’s that important. All that is wrong with the current period is summed up in this one shameful, shameless bit of purposeful prevarication.

Instead, they deliberately throw out this seemingly nondescript reference because it will serve as a de facto official explanation (without appearing to make a big deal out of it) while at the same time they know it will never be challenged. Even though it is, again, demonstrably false, the mainstream media and almost every form of financial commentary is deathly afraid of something like OIS; they don’t understand it, they believe nobody else does, so therefore if the Fed says something about it, then it must be so. Leave it to who are still treated as experts. Failure isn’t just an option, it’s become the job description.

Say the word “swap” and people go running for cover. OIS is the overnight index swap, and what it is really doesn’t even matter. Complexity has been a shield for this massive dereliction and for a very long time. It’s how you get an entire decade where conventional wisdom still thinks of 2008 as a subprime mortgage problem. It’s how the entire global economy could have shrunk, and then stayed that way through intermittent but serious further monetary problems no matter how much QE undertaken wherever.

If anyone ever does challenge them on this topic, the FOMC’s typical lawyerly ways were foresighted enough to include the term “as a factor” in their address of it. We didn’t deny there might be liquidity risk, they might say, we chose not to specify anything other than this T-bill crap as one possible explanation.

They know exactly what they are doing, and the day they don’t get away with it is when it ends.

Stay In Touch