The global economy is not falling off a cliff. There isn’t even evidence it is about to or is nearing such a situation. The most alarming that might be said of how things appear right now is that conditions aren’t getting any better.

It’s hardly the stuff of severe global unrest. This is why individual developments are always cast as isolated cases. For workers to take the streets by the millions in some faraway undeveloped country in 2009 would make sense. In 2018? It seems out of place.

But that’s exactly what is transpiring and in too many places to ignore. Last month, some 200,000 of Brazil’s truck drivers (out of a million; one in five is an impressive demonstration of frustration) went on strike and the country was left at the mercy of unpreparedness. Only a few Western outlets identified and wrote about the genesis:

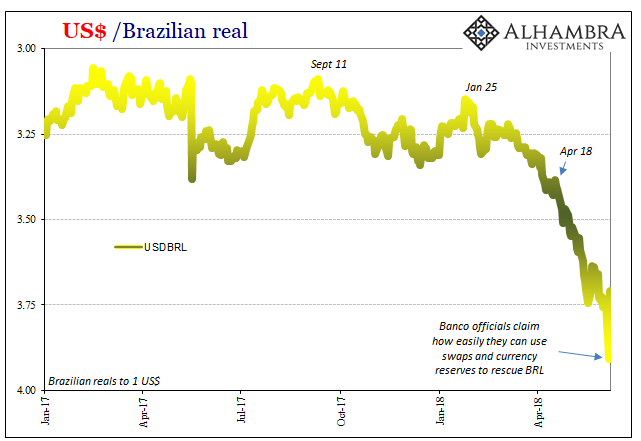

A depreciation in Brazil’s currency, the real, to a two-year low against the dollar, together with surging oil prices, is driving up fuel costs. This is combining with political uncertainty over elections in October, which are expected to be the most unpredictable in decades, as well as investor doubts over Brazil’s troubled fiscal situation to severely test the centre-right government of President Michel Temer.

But just as the Financial Times gets is right, they get it wrong. Why is the real tanking? Rising UST yields, at least according to the article or anyone else recognizing currencies.

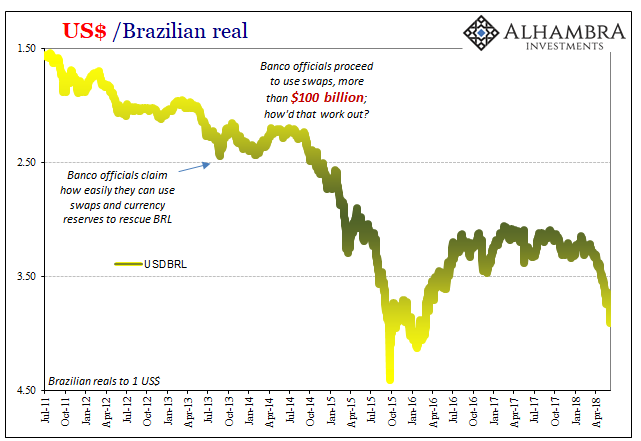

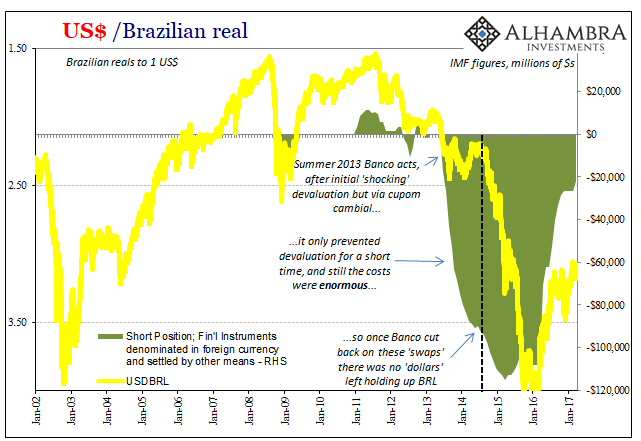

It surely wasn’t rising yields in the US bond market that caused all this massive trouble the first time (not that yields are moving upward all that much now, at least at the long end). UST yields in 2014 and 2015 were falling, not rising. As noted last week, officials at Banco do Brasil were at the time practically bragging about their nation’s massive stockpile of reserves. The real collapsed anyway though no mainstream explanation was ever given. The whole thing (“rising dollar”) remains as if a black hole in the mainstream.

There are now rumors of another trucker strike set for Thursday next door to Brazil in Argentina. That economy can ill-afford another massive blow, already absorbing substantial degradation such that the IMF was brought in to administer the largest bailout in the organization’s history.

What is going on?

The media narrative is simple. This is standard operating procedure for countries like Argentina and Brazil. Even in the best of times officials in these places can’t get out of their own way. Therefore, they are going to screw it all up at the worst possible time, just when the rest of the global economy starts to take off in synchronized fashion. Well, almost synchronized.

The reason this narrative can’t account for 2014-16 is that it is all backwards. Brazil like Argentina (and the rest of the EM’s) has fallen back into crisis not because of their idiosyncrasies despite globally synchronized growth, they are primary examples of how unflattering characteristics are so exposed when there isn’t growth. These pressures really intensify, more importantly, when there isn’t likely to be anytime soon, either.

It’s the same downward spiral repeating for a fourth time: economic doubts feed monetary doubts which double back on economic doubts; sputtering economic growth leads to “devaluations” and crisis which then further depress economic growth. Central banks throw everything printed in the orthodox Economics textbook at these problems to no avail. They can’t break the circle.

This has been coming for some time. Reflation #3 built up relatively quickly toward the end of 2016 and into early 2017, but then it was arrested almost as fast. By last summer, there was the growing possibility that that was it, the best was realized and despite several years of contraction and often devastation there was not going to be momentum and symmetry.

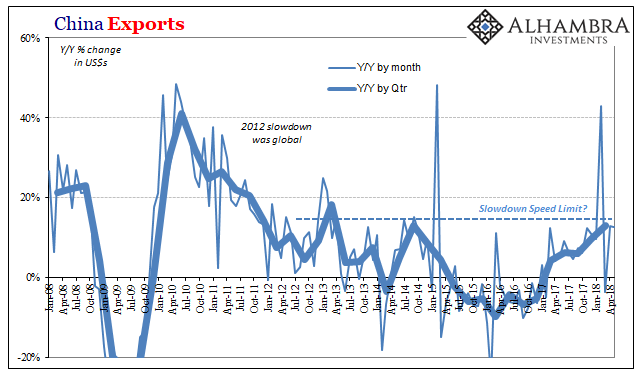

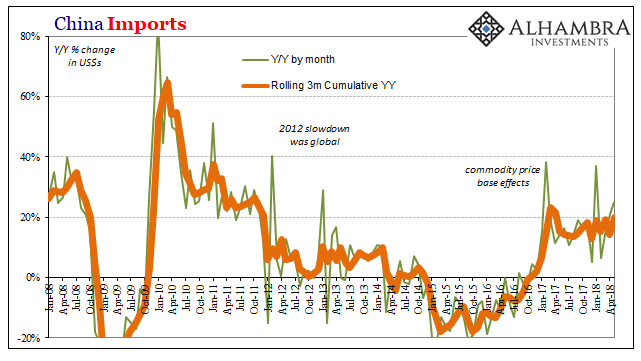

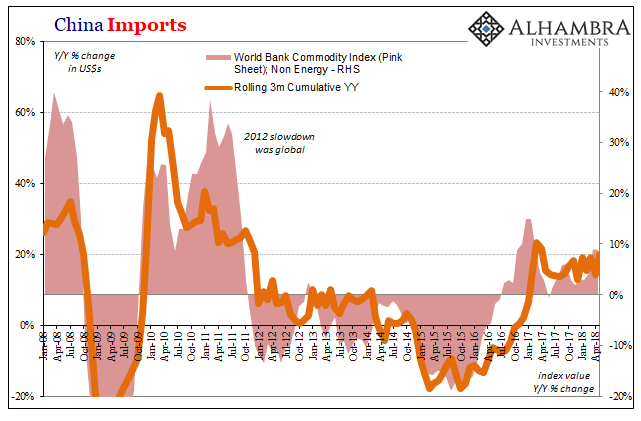

The best example of this deficiency is where it matters the most – China. The numbers by themselves sound almost impressive. In May 2018, the country’s Customs Bureau estimates that Chinese exports rose 12.6% year-over-year. Better than that, imports were up more than 25% last month.

As much as the media makes these out to be good numbers equivalent with the strength provided by globally synchronized growth, they are the exact opposite. These are uniformly bad numbers, and worse they are every bit as consistent as they have been throughout the past year or so (factoring all sorts of distractions, too, like Golden Weeks and trade wars).

In other words, demand from the end user economies like the US has stalled. That’s a huge problem for China’s economy which remains oriented toward manufacturing and export. They talk about rebalancing and internal sources for marginal expansion, but month after month it proves to be nothing more than that – talk.

That means for the rest of the global economy, including and especially Brazil and to a lesser extent Argentina, it can only depend upon the generosity (or gullibility, if you want to look at it another way) of Chinese authorities to bridge the divide. For Brazil to manage well enough without US demand flowing toward China requires Chinese authorities to boost (waste) their own activities.

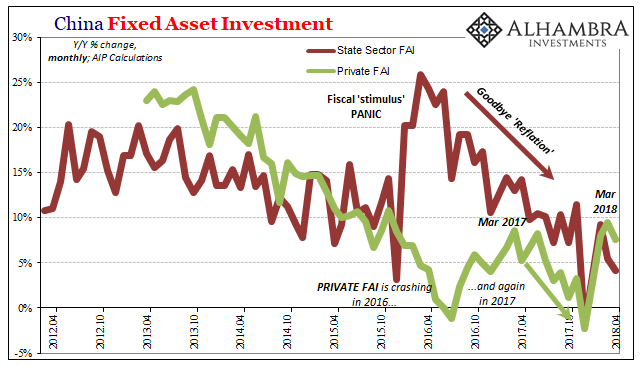

But just as there are only signs of China’s external ceiling, there are more of the nation’s internal reluctance. These include political shifts that aren’t the usual ceremonial handovers. The Chinese are serious about an “L” shaped global paradigm because they have no luxury or wiggleroom to pretend otherwise. They could do all the “right” textbook things in 2012, but that was it.

Now, in the middle of 2018, they aren’t any longer alone in contemplating the “L.”

Stay In Touch