CNY has held up over the last few days after Chinese officials intervened. Central bank actions like these tend to work if only over the very shortest timeframes. The tentative calm there, however, hasn’t extended universally.

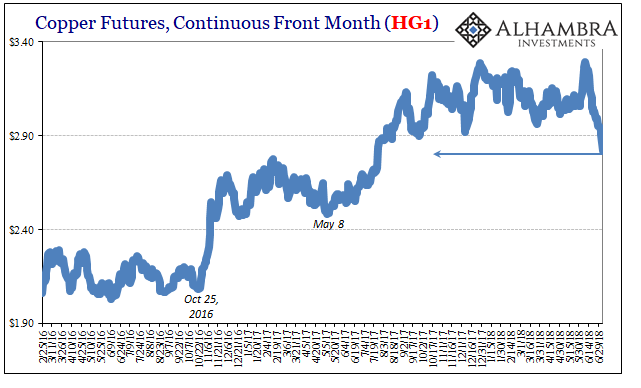

Copper, for one, has fallen right out of its Reflation #3 range. Selling off solidly for almost a month now, today it was pounded down to near $2.80. This breaks all recent lows by more than a little and sends a decidedly deflationary signal throughout global markets hoping for a respite.

There are plenty of those.

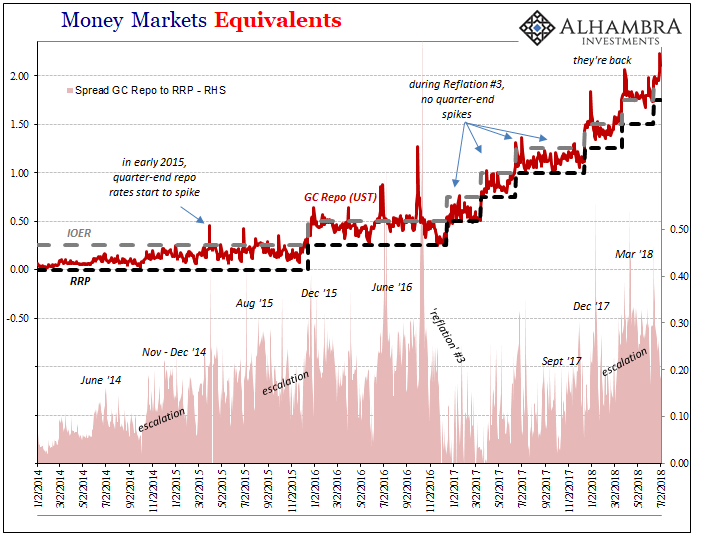

As we start Q3, we take note of the end of Q2. As has become custom, we find certain money market rates exhibiting a familiar quarter-end window dressing. Money dealers in particular pull back on offer in repo markets, leaving certain participants somewhat exposed. This calendar bottleneck can become dangerous if it falls in line with amplifying pressures.

The GC repo rate (UST collateral) was 2.233% on June 29, according to DTCC’s compilations for the last trading day of Q2. That was a spike of roughly 28 bps from June 27.

This makes three quarters in a row now where the GC rate has exhibited quarter-end tightness – the reluctance of dealers to offer spare capacity. The first in that string, on December 29, the final trading day of Q4 2017, seems to have announced something of shift in repo.

That’s just QT and rate hikes, they say. The four prior quarters, Q4 2016, Q1 2017, Q2 2017, and Q3 2017, were not blighted by this phenomenon. Therefore, the timing where it begins right at the end of 2017 would be consistent with the Fed’s actions and could offer a plausible interpretation of the cause. That’s right around the time where balance sheet reduction, the opposite of QE, began to be pressed into the markets.

The problem with this theory is, as usual, it doesn’t account for anything before. These quarter-end repo problems aren’t new, they are instead another in a long line of indications suggesting renewal.

This can’t be the work of the Federal Reserve, nor can it be about T-bills. The first quarter-end repo spike shows up at the end of March 2015. It was then when the “rising dollar” was transforming from an outside if serious oddity into a substantial global rebuke of every mainstream assumption (recovery, liquidity, dollar, etc.)

I wrote in that month pretty much the same thing I’ve been writing again lately:

While these are disparate indications spread across all sorts of markets and geographies, the one commonality between them is the “dollar.” If we are to attempt any kind of more realtime indication of what eurodollar function looks like, it probably doesn’t get much [clearer] than this as all these market rates and prices are suggesting the same thing at the same time – look out for another “dollar” episode potentially just getting underway.

Over that specific quarter-end and then the next six that followed, the repo spike appears alongside some of the most unambiguous signs of global “dollar” strain and worldwide economic downturn – textbook deflationary pressures. At the next four, however, it disappears consistent with reduced liquidity pressures associated with Reflation #3. Then, out of nowhere, it’s back again to end Q4 2017 and somehow it’s the Fed? Or T-bills?

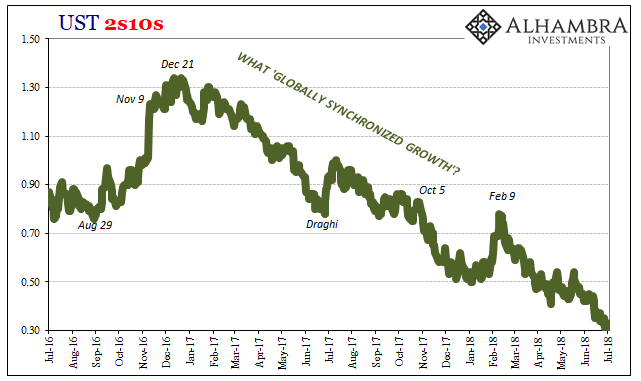

It has to be the Fed or else it just doesn’t fit with globally synchronized growth. There is sure coordination and harmony to it, just not aligned any longer with the narrative.

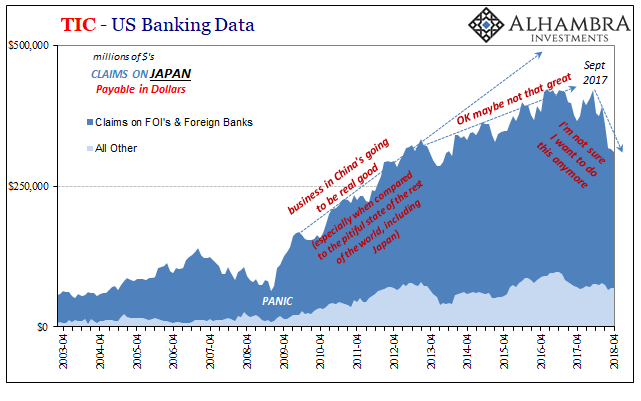

This is true across a whole range of related eurodollar issues. Take one from Japan published only yesterday:

It’s easy to see why Japan has soured on Uncle Sam.

After all, returns on Treasuries have been lousy for years. And the sky-high costs to hedge the dollar’s ups and downs mean Japanese investors can often do better at home — despite the minuscule yields there.

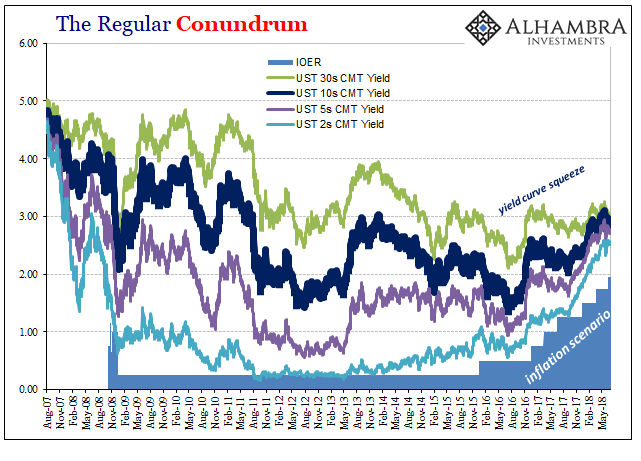

This is another article written to ostensibly warn of the epic BOND ROUT!!!! that has to show up for the narrative to be anything more than rhetoric. We’ll know when the recovery happens, an actual boom, only when the long end of the UST curve confirms it.

So, another mainstream report comes out trying to interpret another money factor backward, attempting to further imply how it is consistent with this supposedly looming rout. On the surface, it seems to line up with repo being related to the Fed and the reasons behind the central bank’s changing policy stance. The Japanese must be dumping UST’s because they know the US is booming and the Fed is increasingly “hawkish” for it.

Except that’s not why Japanese banks are behaving as they have. They are exiting the eurodollar redistribution business because of the heightening liquidity and economic risks. The quote above even refers directly to the former without recognizing it; “the sky-high costs to hedge” is nothing more than the interbank costs associated with funding in a chronic shortage of FX.

Instead of describing a situation that would indicate a huge negative for UST’s especially at the long end, the story ends up reporting factors that are in fact the opposite. These are big positives for them, the nature of the signal that can’t be seen by interpreting them the from the usual mainstream, orthodox perspective. It is really one about rising liquidity risk, which is the big premium that has been embedded in UST’s since before August 2007 (interest rate fallacy).

In that way, these two developments do complement each other perfectly just not at all how they were supposed to. It is only widespread economic and monetary illiteracy that got the Japan story published in the first place because it was presumed consistent with the boom hysteria (more on that later). The appearance of quarter-end repo spikes alongside the more recent actions of Japanese banks are both symptoms of renewal among the same negative eurodollar influences.

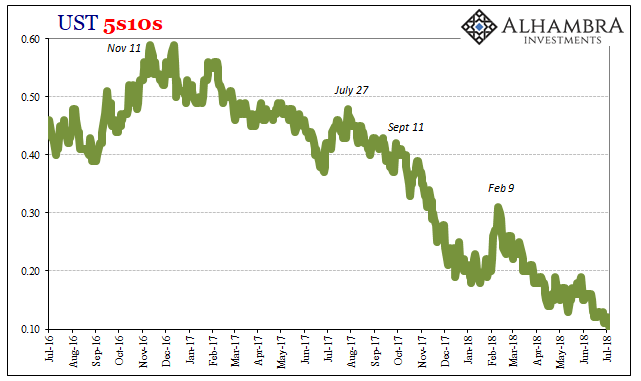

Nothing has changed and that is the problem. There can’t ever be deflationary tendencies, yet there are repeatedly. And the yield curve collapses even more no matter how hawkish central bankers decide they might be.

Stay In Touch