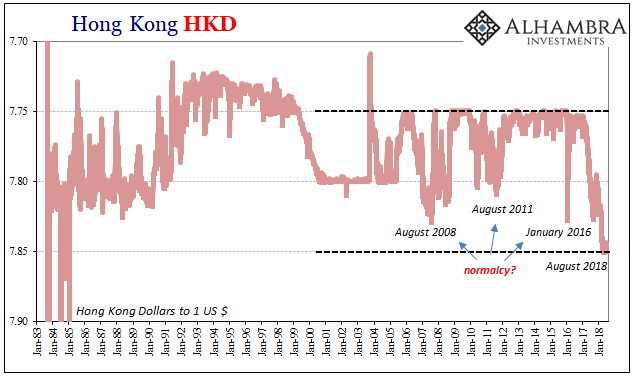

In early March, the CEO of Hong Kong’s Monetary Authority (HKMA) Norman Chan issued a press release claiming among other things his quasi-central bank had more than enough reserves to defend the lower edge of the Hong Kong dollar’s (HKD) monetary band. In trying to settle what was clearly upset markets and not just those in and around Hong Kong, Chan said, basically, this isn’t even something to worry about. HKD is down because the world is getting better!

According to his view, Hong Kong had received massive inflows of, well, currency and other finance in the wake of the 2008-09 panic. It was the safest port in the global storm. Maybe it took about a decade, but other central banks finally got it right and the storm has finally, mercifully passed. Globally synchronized growth, the dominant narrative of 2017, was supposedly behind the trend for HKD in 2018. Safety flows were moving out of Hong Kong’s safety and into recovery dynamics.

How about now?

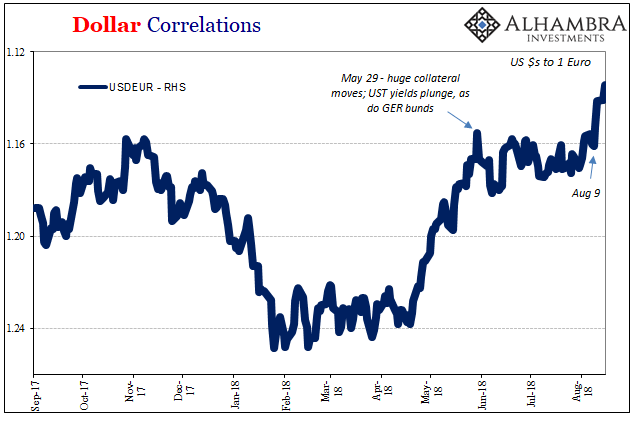

There is a world of difference in the world in August 2018 when compared with even March 2018. In between, there is a whole lot more obvious risk – again. Those parts of the globe that were especially upset during the last “rising dollar” are again being destabilized by the current “rising dollar”, the one (via EUR) that’s on the other side of HKD’s fall.

Thus, it can hardly be said that the reverse of panic flows is still happening. If any of that was in any way true, HKD would be rising along with the US$, not as part of the eurodollar squeeze but as a renewed safety consequence of it.

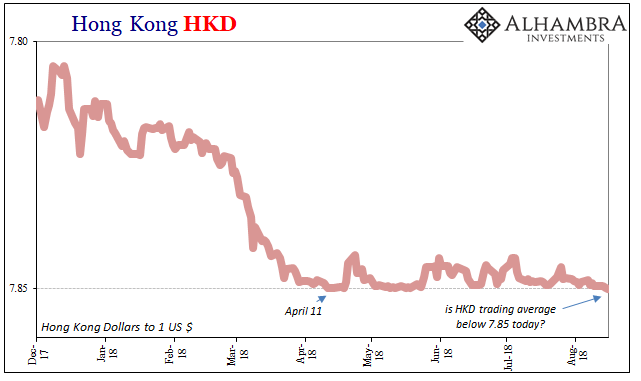

Instead, HKD is dropping, and by falling I mean a possible breach. Several trading screens show it at 7.8502, which would be less than what’s allowed by HKMA. This isn’t the first time since April 11 when the currency met the boundary this is happened, though this is the farthest onto the wrong side I’ve seen it go.

According to other publications such as Hong Kong’s Treasury Markets Association today the closing rate is 7.8499. That’s the closest to 7.85 they’ve published so far (their benchmark spot rate is calculated based on actual transactions conducted within a 30-minute widow surrounding 11 am local time).

We know, of course, Mr. Chan’s contention about what’s behind HKD is bogus. Just look at the history of the exchange value and it’s quite clear that Hong Kong is pressured like everyone else when eurodollar capacity, in all its forms, is squeezed. It is pushed toward the lower end of the range whenever the world is a mess, not getting better. This time, it has been pressed farther than any others; small wonder with China’s “dollar short” very likely incorporate within it this time around.

Rather than the mainstream explanation, HKD perhaps on the other side of 7.85 fits perfectly with what’s going on today, and for the last few days. It sure fits with August. Several of them.

Stay In Touch