In August 2014, then-Federal Reserve Chairman Janet Yellen described the wage dilemma in some detail. She was still relatively new to the job at that time, and there was pressure on her from among the so-called hawks to more aggressively normalize monetary policy. Ben Bernanke had taken the more cautious approach having experienced what both he and Yellen would afterward characterize as “false dawns.”

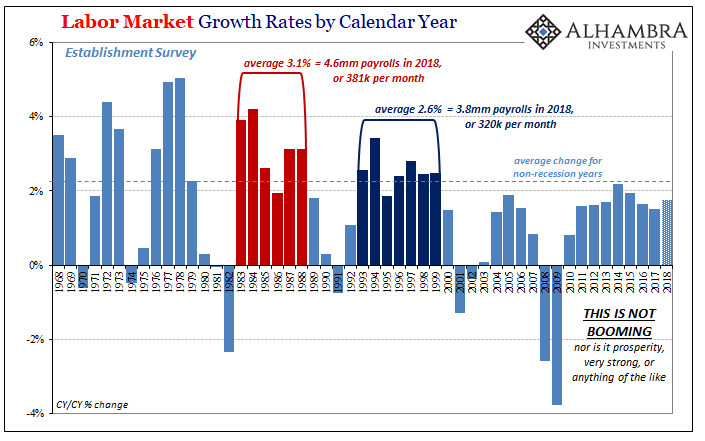

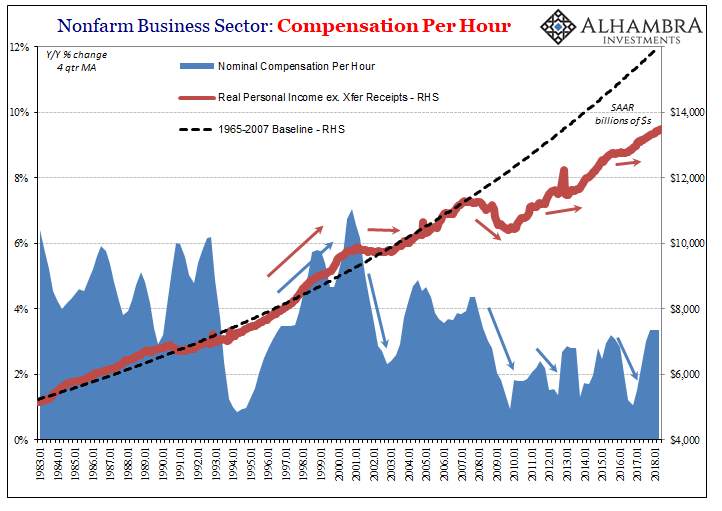

In terms of the tepid wage growth to that point, it didn’t matter that the media was in a frenzy over the “best jobs market in decades.” Labor gains seemed impressive numerically for the Establishment Survey, yes, but even in 2014 they weren’t all that impressive when properly couched in percentage terms (and nothing like the nineties, let alone the eighties).

So, when she went to Jackson Hole that year she played both sides. First, the more obvious reasons for caution:

This pattern of subdued real wage gains suggests that nominal compensation could rise more quickly without exerting any meaningful upward pressure on inflation. And, since wage movements have historically been sensitive to tightness in the labor market, the recent behavior of both nominal and real wages point to weaker labor market conditions than would be indicated by the current unemployment rate. [emphasis added]

This is traditional Phillips Curve stuff. The labor market could improve and accelerate further without generating any wage inflation, and therefore consumer price inflation. To that point, compensation data suggested there was still enormous labor market slack no matter all the emphatic rhetoric.

The balance of risk on the other side, however, was something called “pent-up wage deflation.” The Great Depression was the last declared depression for a reason; American businesses historically at the onset of economic contraction had slashed wages as well as payrolls. This was the epitome of vicious deflation.

They don’t this anymore though many might really, really want to at the worst times – such as in early 2009. These modern “sticky” wages mean that companies have to find other ways to account for costs in contractions, including labor costs. They might not immediately cut wages but they adjust in other ways (if you are interested, here’s the link to the FRBSF paper on “pent-up wage deflation” Yellen cites in her speech; as with most things, it takes what are sound observations and then tries to reverse engineer them to fit within Economics’ self-imposed denial).

These other ways might therefore become a policy consideration if enough recovery were to eventually happen. As Yellen put it:

As a result, wages might rise relatively slowly as the labor market strengthens. If pent-up wage deflation is holding down wage growth, the current very moderate wage growth could be a misleading signal of the degree of remaining slack. Further, wages could begin to rise at a noticeably more rapid pace once pent-up wage deflation has been absorbed.

From what I can tell, this appears to be current Chairman Jerome Powell’s preferred scenario. Ignore the constant wage lethargy, if “pent-up wage deflation” is a real thing at some point wages are just going to explode higher.

As with something like Bigfoot, you can’t prove he doesn’t exist by the lack of evidence for his existence. The myth can therefore easily survive particularly among the True Believers.

What Janet Yellen was saying in 2014, if you take her literally, was that 2015 was likely to be a test of each hypothesis. The labor market appeared to be getting better perhaps quickly and that was compelling in a way, but it demanded corroboration which time would provide, or deny. Either wages were disappointingly showing what they appeared to be showing, or this “pent-up wage deflation” would instead prove a much more pleasing alternative.

One of the major problems with the statistics is that they are contrary to popular belief rife with bias. These are not conscious which is often the charge whenever they might be revealed (X government agency is trying to make Y political party look good, or bad, as the case may be). Orthodox Economics demands either recession or growth. It is a binary assumption that is itself a bias.

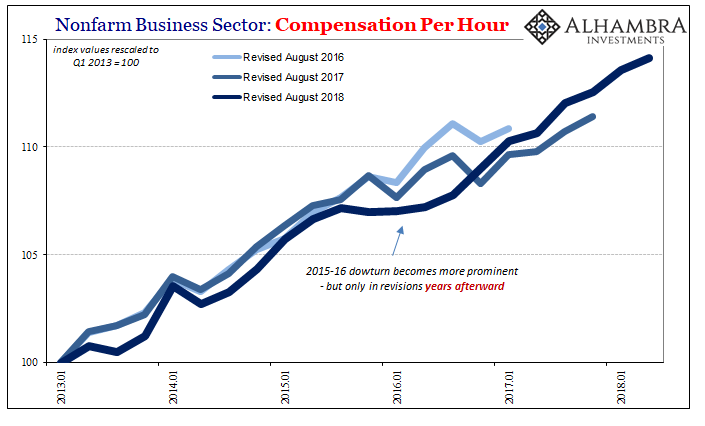

What happens when confronted by actual economic gradation? A situation that maybe acts like a recession, but doesn’t go nearly as far and therefore isn’t one but isn’t growth, either. We know all-too-well that the major statistics have a major problem with these mini-cycle scenarios because of constant serious benchmark revisions to them.

Over time, the 2015-16 downturn specifically has become more and more apparent but only well after the fact. If 2015 was going to be a make or break year for labor market and inflation determinations, where does a serious and now more completely developed (in the data) downturn fit in? It certainly doesn’t with “pent-up wage deflation”, rather it is far more in keeping with constant macro problems depressing key economic functions at key times.

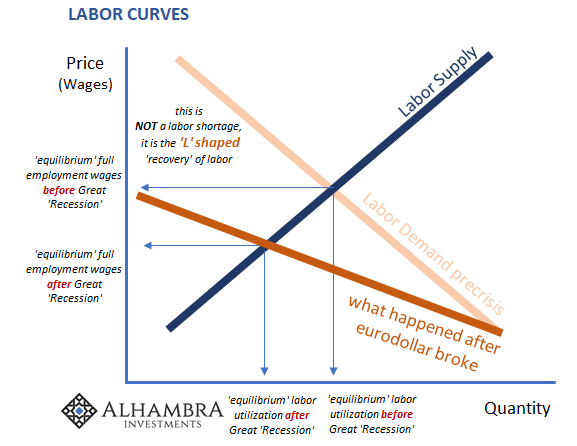

Labor slack isn’t just enormous, there remains the tendency for it to get larger with each non-recession downturn.

I think it helps further explain why the economy never performs like a recovery. Every time it gets loose just enough out from under the eurodollar’s thumb it gets hit with another monetary episode before it can ever really get going. One step forward, two steps back every time; only the mainstream never sees the second backward step because it only comes out through benchmark revisions long after it has been completed.

The addition of another four years after Yellen’s wage question has served to clear up the answer. “Pent-up wage deflation” was simply another mythical creation Economists served up to try to deny clear reality. The economy just can’t be underperforming so badly because Economists at central banks can’t possibly have failed time after time. This is what motivates their constant search for Bigfoot (skills mismatch, Baby Boomer retirement, fentanyl, etc.)

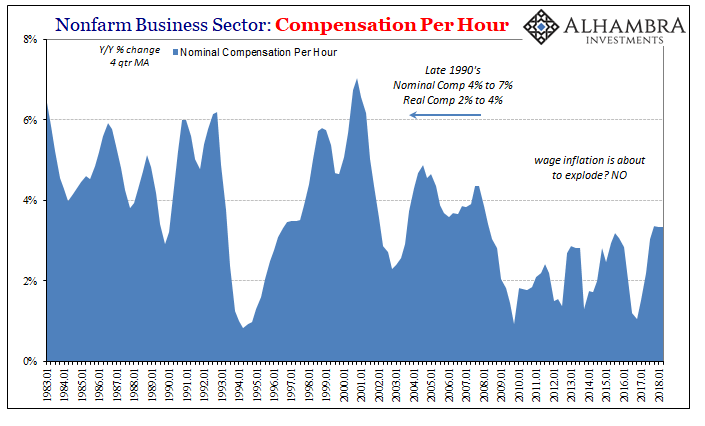

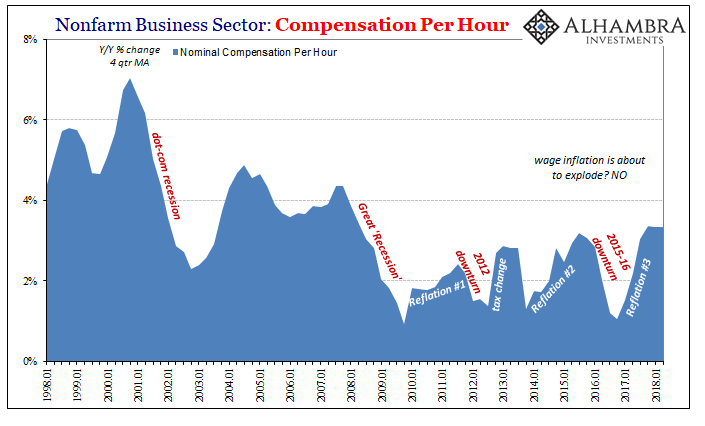

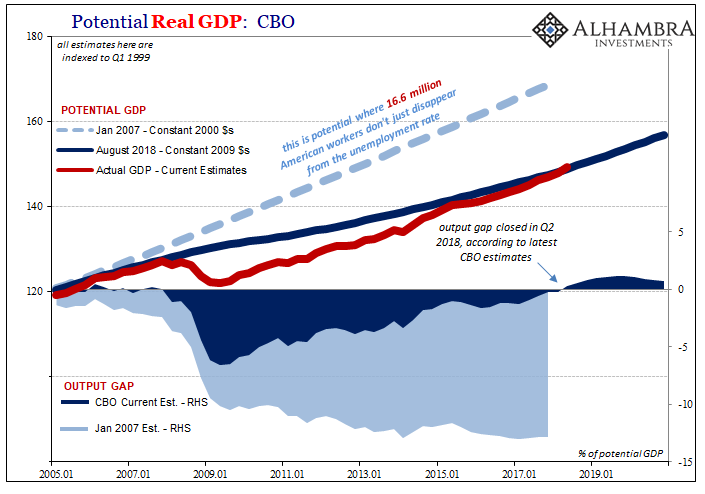

The data is pretty conclusive about all this in terms of labor slack and wages. There is no evidence whatsoever the labor market is tight, let alone held back by some massive, biblical LABOR SHORTAGE!!! The latest estimates from the BLS demonstrate for yet another quarter, now Q2 2018, there’s nothing behind these expectations. There is no boom. Instead, they prove (by length of time) that “something” remains very wrong with the US economy.

What’s holding it back is eurodollars, plain and simple, just not all at once. It’s more difficult to see in realtime because of the overarching bias of some key statistics, but that doesn’t prevent the open-minded from appreciating Bigfoot as nothing more than cute legend.

The true underlying economic condition is exactly what a rational, grounded view of economics (small “e”) declares it to be. There is no great competition for workers because despite all the recent hysteria about some boom, businesses have no desire nor need to pay up for labor. There is no economic growth, at least not what’s consistent with the binary interpretation.

It is the unemployment rate, and for a time the Establishment Survey, that has twisted everyone’s sense of economic sufficiency. Yellen was right. The answers would be found in the labor wage gains. They just aren’t there, and it’s been four years since she set up this test.

Stay In Touch