In the absence of a booming economy, one has been conjured from a select few employment statistics. The catalog, beginning in 2014, consisted of a rapidly falling unemployment rate, the Establishment Survey which dazzled with headline payroll growth supposedly adding up to the “best jobs market in decades”, and the JOLTS series but curiously omitting everything but the Job Openings piece. Over the years since, the middle one has been quietly scratched from the list.

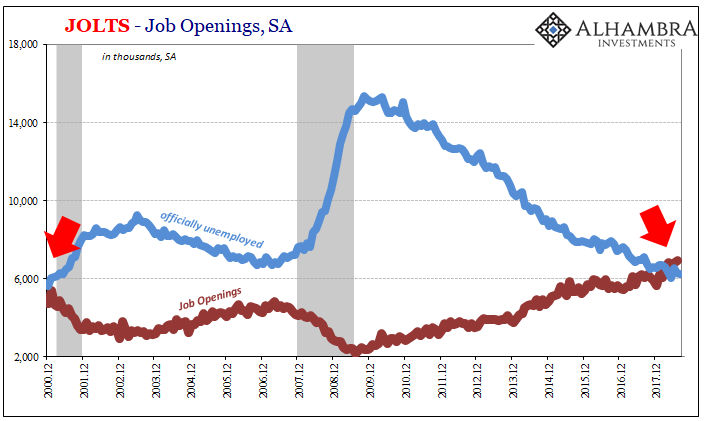

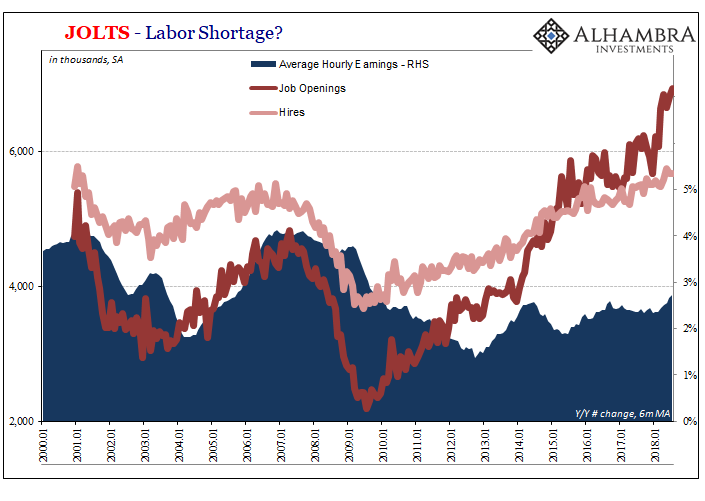

That leaves the unemployment rate which goes lower and lower way past where “full employment” was once thought to begin. And then Job Openings (JO) which go higher and higher well beyond what are supposed to be related data points.

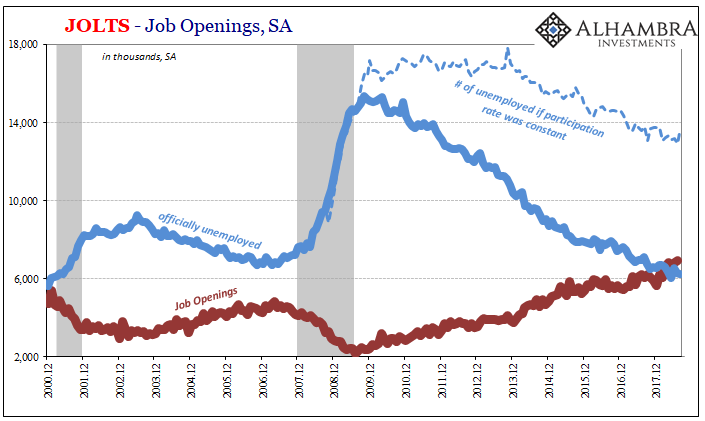

The latest talking point about JO is in relation to the number of unemployed Americans. For the past few months, there have been more job openings, according to the BLS’s definitions for them, than there are unemployed workers, also according to the BLS’s definitions for these. It makes for a terrific soundbite.

So long as you leave it there, the economy can be booming for the first time since the end of the dot-com era. Perhaps it is the best jobs market in decades?

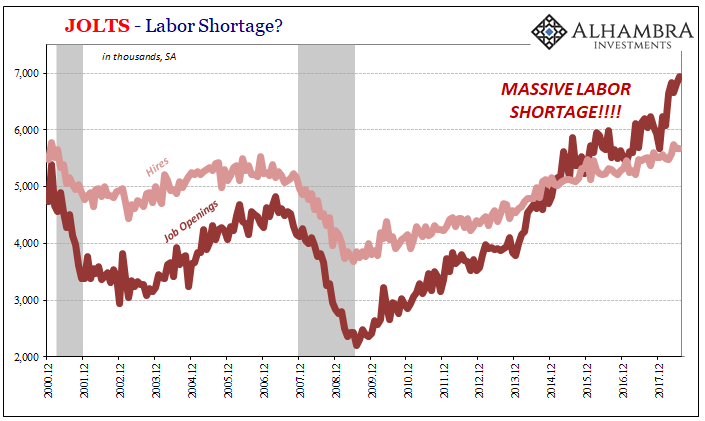

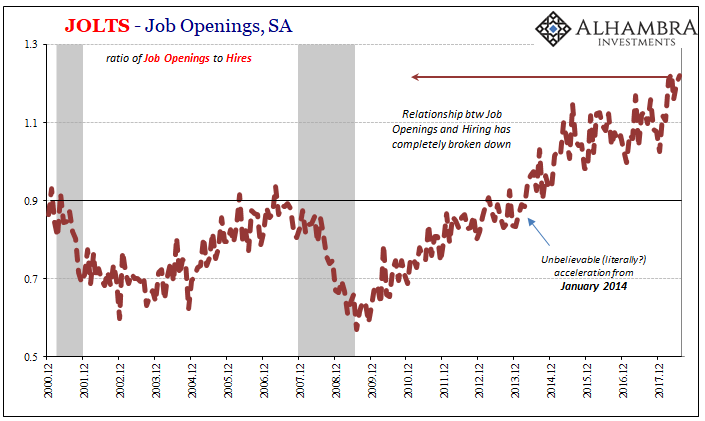

The big problem is that companies are not hiring (HI) at anywhere close to the same level as they advertise for new positions, or to refill those that through the normal course of business (even in a stagnating economy) become available. The difference in just JOLTS between one view of labor demand (JO) and another perspective of the same factor (HI) has become a ridiculous extreme.

It’s been this way now for four years, ever since the data for JO surged in early 2014. While it may have been consistent with the slope of the decline in the unemployment rate, it wasn’t in relation to anything else – including, as we know, the slowdown evident in the Establishment Survey following the near recession in 2015-16. That downturn barely registers in JO.

Which is it?

The answer is really easy. If JO is anywhere close to accurate, then the reason it has exploded higher has little to do with economic growth let alone a booming economy. It can only be one of two things: either the data is flawed, or companies are advertising more for the same number of positions.

Economists want to enter a third possible explanation, which is a big, massive supply problem in terms of labor. They have suggested that Americans are too lazy to go back to school (skills mismatch), too many potential workers are hooked on drugs (opioids, in particular), and many of the same have simply aged past their preference for continued employment (Baby Boomers). The difference between HI and JO is, to add up to a boom, rotten labor.

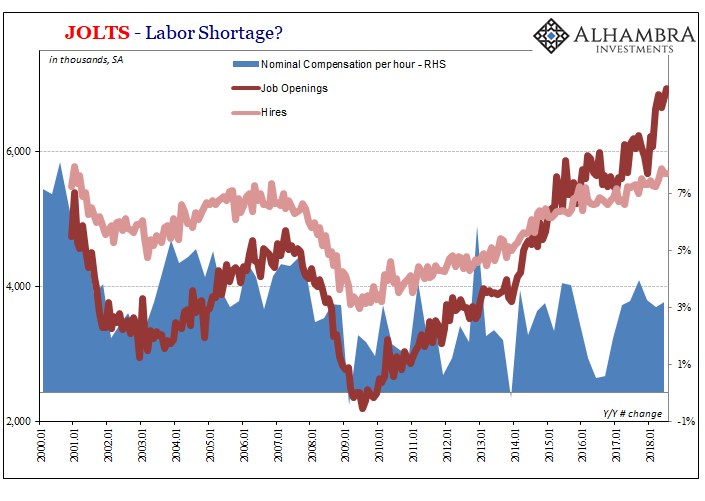

You know where this is all going. If any of that was true, and the labor market especially tight, companies would be paying up for additional labor. They aren’t. It’s just that simple.

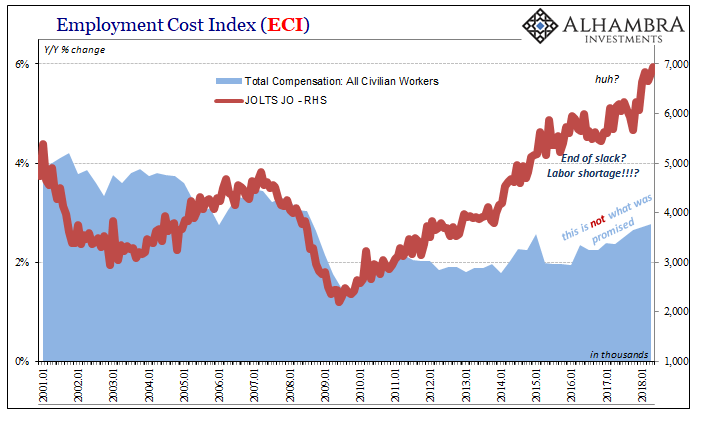

It doesn’t matter which data you use for wages, the shortage is nowhere to be found. What that proves is that HI is probably closer to the truth, meaning far less demand for work than what would realistically constitute a booming economy, than JO which is off in orbit.

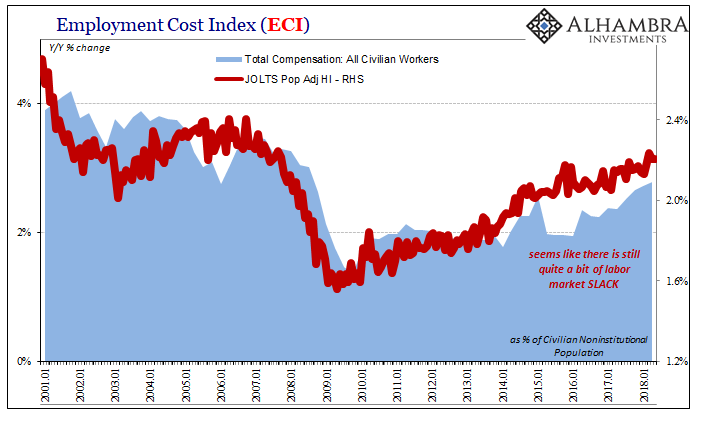

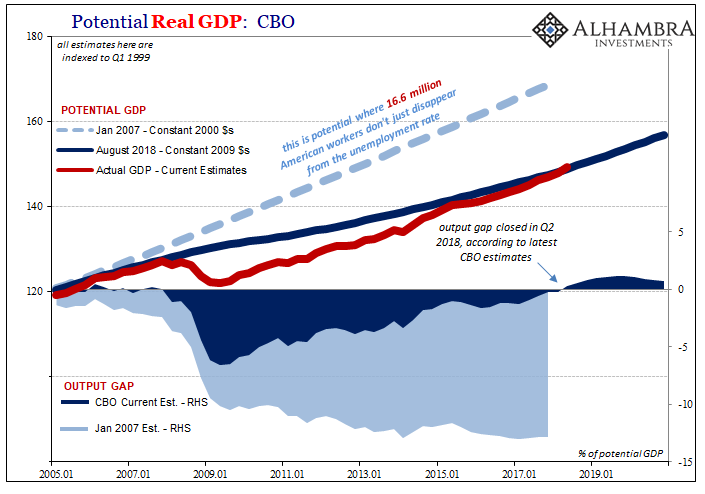

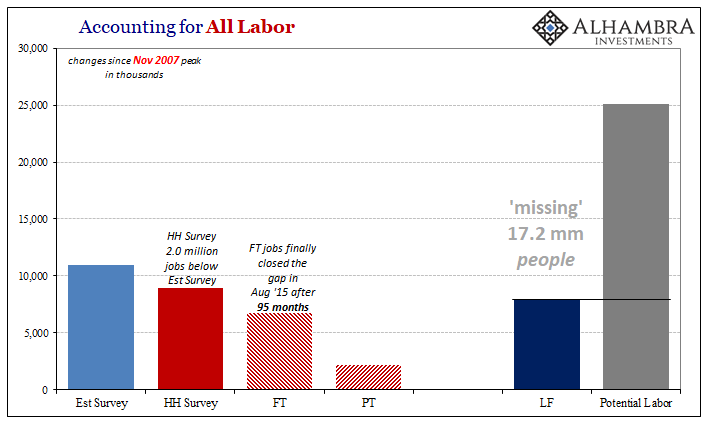

The closest measure to fit all the wage data is when you adjust HI by population. That, of course, brings up the participation problem – a macro factor where the problem in the labor market is not too few workers but too little work. Americans remain on the sidelines out of the official labor force because the economy shrunk in 2008-09 and never came back. Economists have tried to make it seem like recovery by moving the goalposts to a different stadium entirely. They’ve been trying to backwards engineer the appropriateness of these drastically reduced economic standards by clinging to these few uncorroborated BLS data.

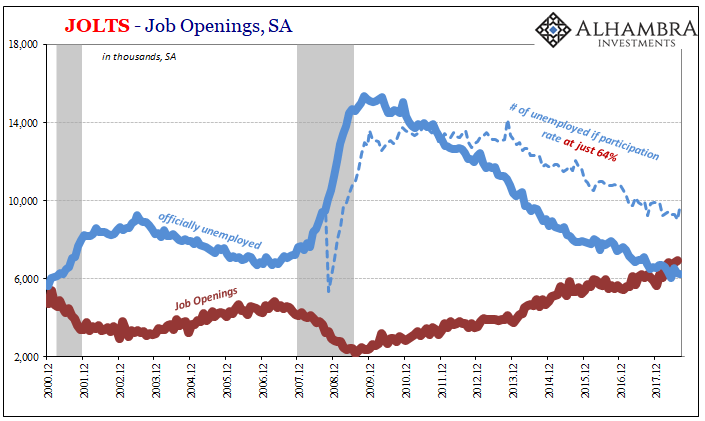

If we return, then, to the big talking point about more job openings than unemployed persons, that’s only true when you purposefully leave off the “missing.” Recalculating the number of those “missing” using either a constant participation rate (from before the Great “Recession”) or even one that has fallen to, say, 64%, either indicates substantial labor market slack especially compared to prior cycles.

That amount of remaining labor slack would be consistent with wage data that, eleven years later, continues to be historically, suspiciously depressed no matter how low the unemployment rate goes, which excludes the “missing” from the denominator, or how high JO can fly for reasons that can’t be explained in macro terms outside of Economists’ collective imagination.

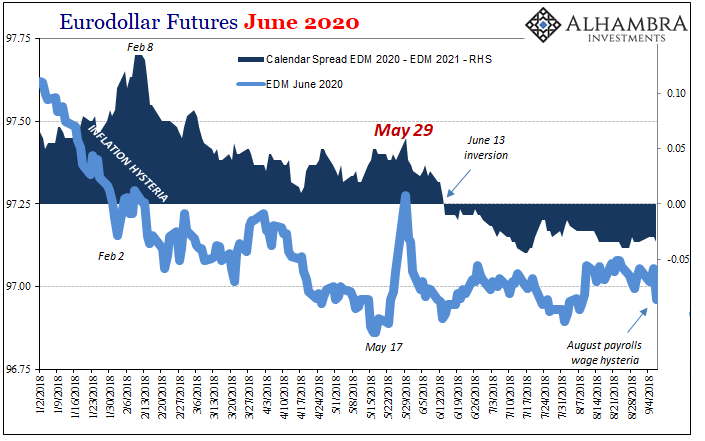

As the 10-year UST yield moves back toward 3% again, perhaps continuing the BOND ROUT!!! that began with last Friday’s payroll report (highest hourly wage growth since 2009), I still don’t think that’s because the bond market at the long end buys where JO is and the boom narrative derived in large part from it. Rather, what’s happening, I believe, is that bonds are adjusting to how Jay Powell inevitably will.

Janet Yellen in 2014 famously put JO on her so-called dashboard for the labor market (she also eventually included the Fed’s own creation, the LMCI, but only until it, like HI, conveyed the wrong signals for too long), so we can reasonably assume Chairman Powell considers this piece of JOLTS for his.

Eurodollar futures, like UST’s, have sold off sharply the last few sessions. That suggests the market expects a little better chance Powell gets a little farther in his “rate hike” intentions. But the eurodollar curve remains inverted in the same 2020-21 range regardless of indicated nominal moves, which also still suggests the market believes there is the nontrivial chance (since May 29) he will have turn around at some point.

Again, markets aren’t buying this boom and wage boom stuff because there is really nothing behind them. They are instead selling off of how they believe Powell will lustily embrace them because he really, really wants to. He can more easily sell an additional fed funds hike with JO where it is, even if the rest of the global economy has become much less synchronized in the face of the dollar.

So, the Fed might go a little farther than what was thought last week, but in the end the likelihood of that meaning an actual economic pickup remains as muted as HI and the wage data.

Stay In Touch