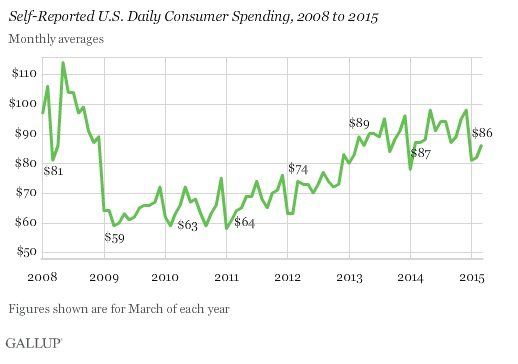

To add depth to the consumer credit version of consumer inclinations in 2015, Gallup’s estimates of daily spending in March came in at $86. That was only $4 greater than February’s $82 which hadn’t rebounded at all from January. In other words, there is “something” wrong with consumers so far in 2015, even as compared to prior years of lethargy. The current figure is slightly below both March 2014 and even March 2013. Without adjusting in any way for actual price changes, the trajectory for consumer spending provided by Gallup is not encouraging.

What we see is that consumers have apparently stopped advancing their spending habits dating back to early 2013. It is unusual that there would no spending increases given that job growth is purportedly very strong, especially of late. Instead, factoring significant price changes over those two years especially in nondiscretionary items, the consumer is clearly trending downward. That, of course, fits well within the parameters of the 2012 slowdown. Essentially, there has been no gain in consumer “demand” going back to that point.

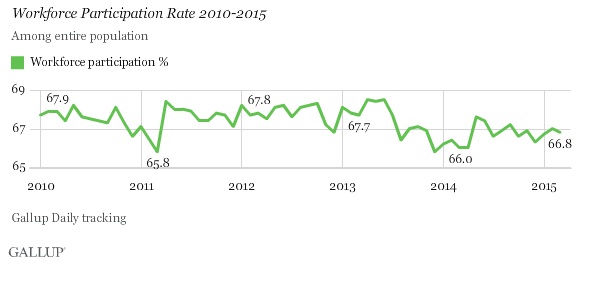

Gallup also provides alternative employment estimates, and it is here that this really gets interesting. Their calculated view on labor participation is different than the BLS, but unlike the BLS and the highly adjusted statistical processes that count for payrolls Gallup’s view on participation aligns very closely with the spending chart shown above.

According to Gallup, the participation rate was largely stable (a deficiency all its own, getting back to the unified or supercycle) until the middle of 2013. That could associate either the 2012 slowdown or even the major taper drama in credit and “dollar” markets from the middle of that year. Whatever the actual case, and it may be some of both, the participation rate has actually decreased rather significantly since then. That would certainly offer a reason as to why consumer spending has remained at least stuck, if not slowly degrading itself.

Of course, Gallup’s inhouse measure of the unemployment rate has fallen pretty much as the BLS’s version, but that again alludes to the major part of the deficiency here. The population is expanding but job opportunities are not, and certainly not in a manner consistent with robust and sustainable growth. So where these two estimates for unemployment agree upon the direction of the unemployment rate itself, at least Gallup is more honest about why that is.

The decline in workforce participation in part reflects demographic changes in the adult population as increasing numbers of baby boomers retire, but also lower rates of participation among those in their prime working years.

As I noted earlier this morning with consumer credit, those in the “prime working years” are not missing but rather statically altering the common view upon how economies work. In other words, it was assumed that spending for the sake of spending would lead to a “pump priming” in which the entire economy would sally forth into desired boomtimes, but instead no such thing has occurred. Instead, at least the fiscal side of redistribution has had the effect of “hiding” a great deal of these labor force “non-participants” within the 21st century version of souplines (though that does a great disservice to those that experienced the Great Depression first hand, as there is no comparison then to the real danger of starvation vs. what is essentially an indebted invitation to a relatively cushy and risk-free existence).

Such stagnation again suggests that any changes in the current trends in the economy are taking place within a larger supercycle that has not yet abated or found its way past lingering imbalances. The problem of that as it relates to the 2015 is that we don’t know how an economy will react if recession occurs, or even another slowdown, with consumers still hole up inside the bunker from the last one.

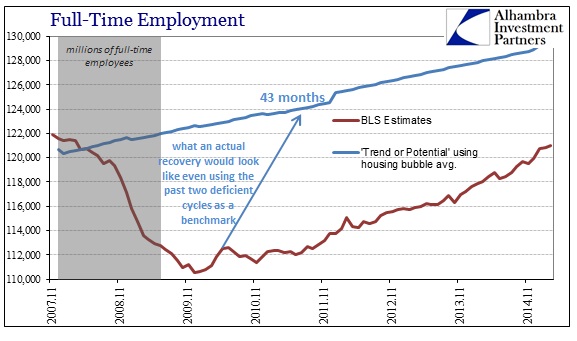

It is that last point that I think Gallup shows very well that other factors and accounts do not: Gallup daily spending has never reclaimed the pre-collapse levels that were common. In that respect, these estimates are at least consistent with one part of the BLS cabinet, namely that there are still 850,000 fewer full-time jobs in March 2015 than November 2007. There is no recovery, thus no separation of “cycles.”

Stay In Touch