If you go back and review the academic literature from the 1960’s up until the 1980’s as it related to monetary policy and recession, you find a rather solid foundation for credit as a means of deconstructing contractionary forces. The interface between expectations and actions had typically occurred within the realm of business credit, whereby deepening pessimism was “passed off” into the real economy as either tightening lending standards or lower credit availability. Monetary policy post-1980 took that foundation as an excuse toward a heavily activist approach which believed that alleviating or softening any credit crunch would be the same as avoiding recession entirely (it obviously wasn’t).

Of course, that was never a safe assumption to begin with and there is enormous distance covering the whole boundaries of finance. But the fact remains, even of 2007-08, that the inception of recession gathers at the point where business credit starts to swiftly fall away. This is a last resort kind of process where businesses will appeal to borrowing even in the face of a slowdown in revenue as they are never quite sure that any slowdown might be just temporary; so it becomes a full-blown dislocation where that appeal amidst the slowdown is no longer viable.

That was always the primary danger between this latest slowing and the others that have come, as an annual ritual, before. The “dollar” breakdown beginning last summer was, at its core, a financial process that threatened more than just asset prices and “market” liquidity. It had the potential to trip up and derail vital flow to actual business needs (rather than the purely financial up to this point).

To that end, there have been some very concerning signals in a lot of different economic accounts that play upon that potential, including some sentiment surveys which I studiously ignore out of pure disdain. However, even sentiment surveys have some use and meaning where they attain an outlier state or denote strongly a potential durable shift, even outright inflection. Leave it to my colleague Joe Calhoun to remind me of that , forwarding the latest and not-well known CMI from the National Association of Credit Managers.

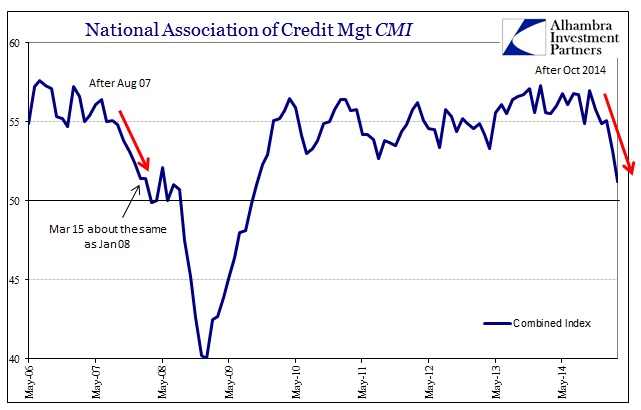

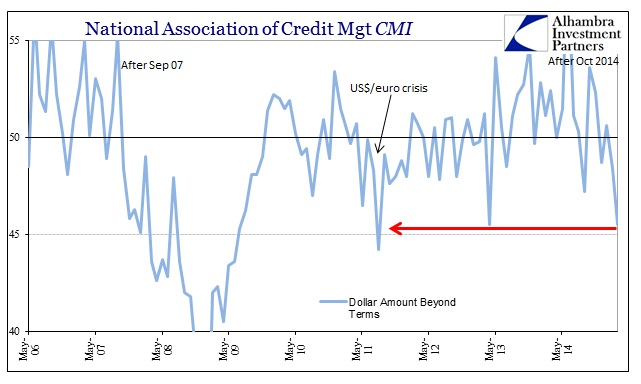

This is exactly the nexus of financial conditions that suggest more than purely financial disruption. The CMI measures (with all the same caveats about sentiment surveys still applicable) credit conditions for businesses in both manufacturing and services, breaking down “favorable factors” and “unfavorable factors.” The former consists of aspects like new credit applications and dollar amount of credit extended, while the latter, which I think is more important at cycle inflections, attempts to systemically quantify parameters like the rejection of credit applications (tightening conditions), accounts placed for collection (tightening abilities to pay) and dollar amount beyond terms (overextended financial position).

The March release of the CMI was absolutely atrocious, particularly among the “unfavorable factors.” From the release itself:

We now know that the readings of last month were not a fluke or some temporary aberration that could be marked off as something related to the weather. There is quite obviously some serious financial stress manifesting in the data and this does not bode well for the growth of the economy going forward. These readings are as low as they have been since the recession started and to see everything start to get back on track would take a substantial reversal at this stage. The data from the CMI is not the only place where this distress is showing up, but thus far, it may be the most profound.

The March reading was not quite in “contraction” territory, but that was entirely made up of “favorable factors” not deteriorating as much as “unfavorable.” Still, the index value was the lowest in the “recovery” period and equates to about January 2008 in the prior “cycle.” What makes this CMI somewhat compelling is its stability of measure, thus that increases the likelihood that an actual shift in the measure is picking up an actual change in the economy (which is where most sentiment surveys go “wrong”).

The March reading was not quite in “contraction” territory, but that was entirely made up of “favorable factors” not deteriorating as much as “unfavorable.” Still, the index value was the lowest in the “recovery” period and equates to about January 2008 in the prior “cycle.” What makes this CMI somewhat compelling is its stability of measure, thus that increases the likelihood that an actual shift in the measure is picking up an actual change in the economy (which is where most sentiment surveys go “wrong”).

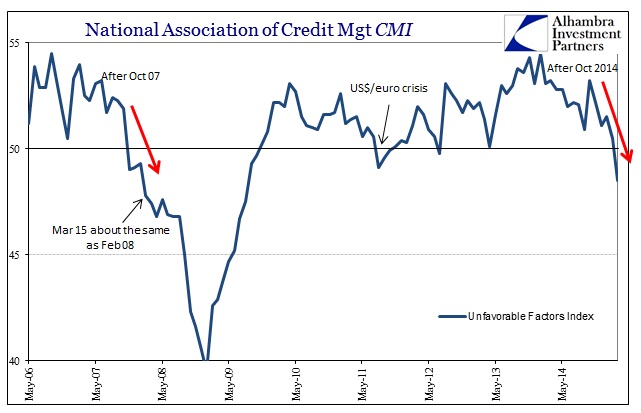

As in 2007-08, it is the “unfavorables” that shift first and worst:

The index has tumbled since October 2014 (a financially-relevant month) all the way to 48.5 which marks the lowest point since 2009, even “besting” the “dollar” eruption in August 2011 (which saw the S&P 500 drop almost 20% in a matter of about two weeks). That is the same level as February 2008 but on an even steeper decline.

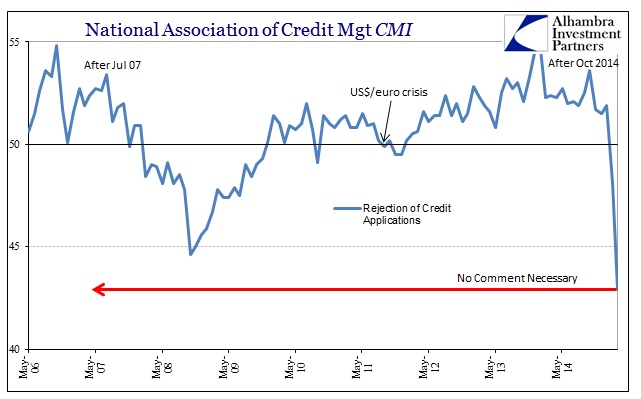

Inside the “unfavorables”, the rejection of credit applications stands out as either totally out of line with real world possibilities or a signal that March got much worse than anyone expects (and not just orthodox economists who never imagine anything could be bad under ZIRP or QE). I honestly don’t know what to make of this except to say that next month will be interesting if it continues or even only bounces back partially.

While that looks like a one-month collapse in the chart above, it is actually spread out between February and March; January was all the way up at 51.9, and then February fell to 48.1 and March simply failed to 42.9. If those numbers are even close to an accurate proxy, then businesses found the credit door slammed shut in a manner that isn’t within our experience.

One other “unfavorable” subcomponent suggests that any huge surge in credit rejections is not solely as a matter of businesses being overextended (which would actually be a positive condition if businesses were rapidly expanding and maxing out while doing so), at least not to the same degree. That would tend to offer that this is both a factor of existing credit “demand” conditions as well as something very much awry in the willingness of financial intermediaries to offer (either lending standards went up dramatically in the past two months or liquidity is really starting to bite actual credit rather than the gambling-type we have seen in prior outbreaks; or both of those).

Despite my personal disregard for sentiment surveys, there is a great deal here that is potentially affirming toward a huge turn in 2015 particularly as compared to even last year’s “snow.” In many ways, this CMI is actually worse than others as it is a much more forward-looking indication about what business might be able to do in the coming months. If that is a proper interpretation, look out ahead.

Stay In Touch