It is hard to take any one-month change as anything more than usual variation when it is so far out of alignment with everything else. Some economists are cheering the fact that retail sales rose for the first time in four months, and that it was the biggest monthly gain in a year, but both of those interpretations obscure that going from really, really bad to really bad isn’t progress. Further, even in a recession, there will be bounces and variability in the state of the decline from one month to the next – even recession progresses awkwardly.

The Wall Street Journal actually reports probably the fairest assessment, acknowledging at least the negative as consumers are not behaving as every orthodox economist was vocally adamant about the energy “windfall.”

U.S. retail sales rose for the first time in four months in March, but the gain wasn’t enough to offset weaker spending during the winter months as consumers continued to largely pocket savings from cheaper gasoline prices.

Sales at retailers and restaurants increased 0.9% last month to a seasonally adjusted $441.4 billion, the Commerce Department said Tuesday. That was the biggest monthly gain in a year, but was weaker than economists expected. Economists surveyed by The Wall Street Journal had expected total sales would rise 1.1% in March.

By all accounts, consumer spending in March continued the downward trend that appeared late last year – and that is a big problem. The fact that March’s figures were slightly better than February actually counts for nothing good, and instead tends to confirm the “wrong” direction is more than weather or “transitory.” In every category, the “growth” is just ugly:

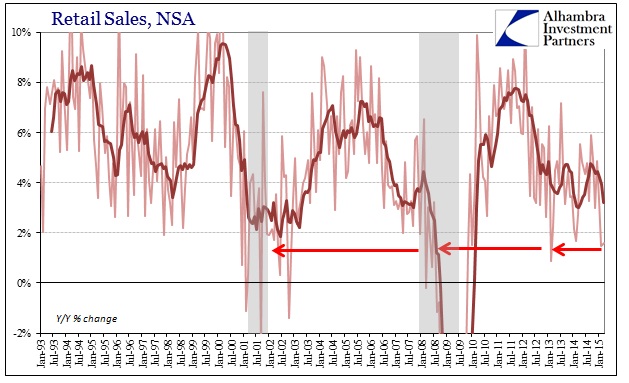

Both February and March saw total retail sales, including autos, grow at less than 2% nominally. Those are rates of expansion that you see in mild recession, and the fact that it was repeated in consecutive months reduces the probability of statistical explanation. To that end, removing auto and food sales shows that “demand” has shrunk in consecutive months for the first time since 2009; and by a fairly alarming amount.

March was among the worst sales results this century (and really going back to the inception of the data series in 1992) across every retail sales arrangement.

The aggregation of the continuation in auto sales only has the effect of marginally improving the standing in recent months. Instead of February and March being among the 20 worst months of the millennia (so far), overall retail sales in 2015 are in the bottom 30. In other words, despite all the rhetoric about “aggregate demand” and spending for the sake of spending, the debt-based intrusion and injection into the auto sector has done very little toward sparking wider and more sustainable activity anywhere else. About all that auto sales are doing is keeping consumer spending slightly more ambiguous about a growing recessionary presence.

That last point is made amply clear enough, with or without autos, in the cumulative sales per quarter. Presented below as rolling 3-month totals, the first quarter of 2015 has been, by far, worse than everything except the collapse phase of the Great Recession – meaning that 2015 so far is growing slower than at every quarterly point in the dot-com recession and the first part of the Great Recession.

Again, that means, as the Journal alludes to, that there is far more than just a one-time aberration at work here. Every series shows a significant decline in growth dating back to October 2014, with an amplification of the downside in either December or January. This is far more nefarious and lingering than the “unexpected” snow and winter of last year, and certainly a greater downside risk that is implied by that.

The more this negative state carries on the more likely that even autos and the rest of “demand” begins to follow lower (if it hasn’t already started in businesses), leaving nothing left to support even minimal gains. I asked of February’s figures last month if “we” can finally admit there is a serious economic problem here, and March has brought even economists closer to facing up to that.

“This outcome confounds all the standard consumer-spending models,” J.P. Morgan chief U.S. economist Michael Feroli said in a note to clients. “Job gains, wealth gains, low gas prices and very high consumer sentiment would all point to solid consumer spending increases.”

There is nothing in this report that can be classified anywhere near “good”, and the best that can be said is that it is slightly “less bad” than the prior month. At this stage, with job growth supposedly plentiful, “bad” shouldn’t be anywhere in sight let alone a now-regular occurrence.

Taken together with so many other indications, so far lasting even into March there is quite a lot that suggests 2015 is very different than either 2014 or 2013. That had been expected, with all that 5% GDP and the “best payroll expansion since the 1990’s”, but this is in the opposite manner as that narrative. It would submit that those statistics were/are at the least mis-calibrated, as are the dominant theories and interpretations about them. There is, again, not even the slightest hint of a booming economy, including autos, and more than a little that portends gathering recessionary pressure. The longer this lingers the greater the probability of that coming out.

Stay In Touch