With the lunacy of “payroll Friday” on full display, it isn’t much of a surprise to get overwhelmed by commentary that totally upends what investing used to be. There once was a mythical relationship that spanned and nurtured between stocks and the real economy. The former was representative about what to expect in the latter, and the latter benefited from that closer relationship. Over the decades of the eurodollar system advance and interest rate targeting and general central bank activism, the relationship flipped, flopped and may no longer generally apply.

Recognizing that isn’t especially insightful in 2015, but that is just further confirmation for how far (or low) economic conditions have been bastardized by the single-minded purpose of central banks toward nothing but debt and indebted finance. To wit:

“Probably best scenario in which the market was hoping for growth but not (so strong) that the Fed needs to hike in June,” said Ryan Larson, head of U.S. equity management at RBC Global Asset Management (U.S.).

With even Janet Yellen (JANET YELLEN!) publicly “shaming” stock markets that she herself had a great hand in supersizing, common sense and basic logic would dictate, demand, that the US go through the most spectacular growth period in history. Tepid growth won’t do from here, as record highs and historically stretched valuations don’t turn more “normal” through unstable growth; it’s either a full-blown boom or the more historically-conforming and greatly unsettling way of reverting to the mean.

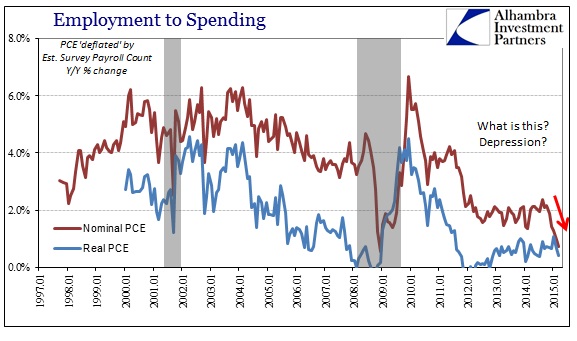

In this particular case, even the Establishment Survey will no longer due. It’s more recent stumbles are starting to suggest that last year was, in fact, nothing but a statistical mirage. There is already the high degree of incongruity poking through as retreating productivity, but there is still no transition from these assumed jobs into wages and then spending (all that “demand” monetarism has been targeting, conspicuously without success, for almost eight years now). At some point, even S&P 500 companies will need revenue growth if only to supplement leveraged stock repurchases.

Despite strong job creation data for April, wage numbers are still weak and point to an economy that is still wobbling, Mesirow Financial chief economist Diane Swonk said Friday.

Average hourly earnings rose 2.2 percent from a year ago, although only by 3 cents to $24.87 from March, the Labor Department said Friday.

“The porridge is still too cool from my perspective and certainly from the Fed’s perspective and that’s why you are not going to see a June rate hike,” she said on CNBC’s “Squawk on the Street.”

The contradiction at the heart of that romantic monetary scenario should be more obvious, but the conventions of orthodox interpretations prevent observation from being observation. Economists are still, somehow, talking about “slack” in the economy when last year was supposed to have erased it. It seems clear that these conventional notions about “slack” no longer hold to the meaning of the actual word.

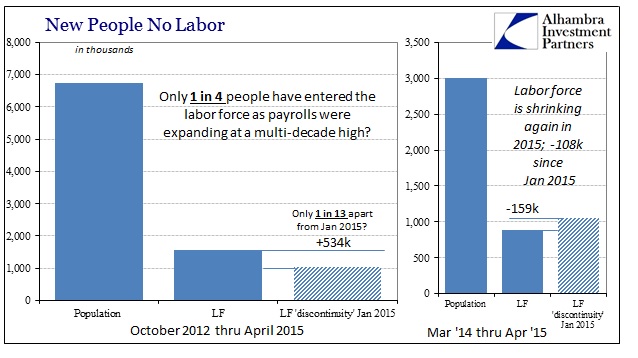

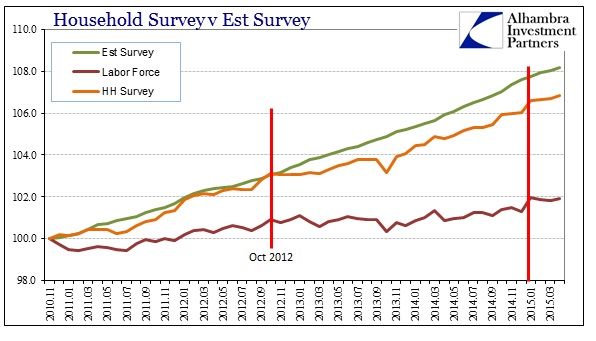

Such “strong job creation” came with only a tepid increase in the labor force, which has continued to shrink in 2015. Apart from that massive discontinuity in January (+1.05 million), the labor force has declined for the entire time that job creation has been reported at multi-decade highs.

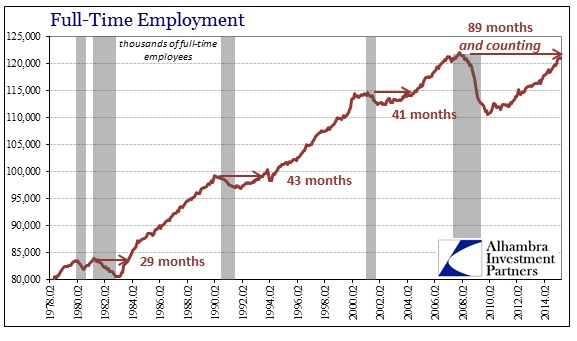

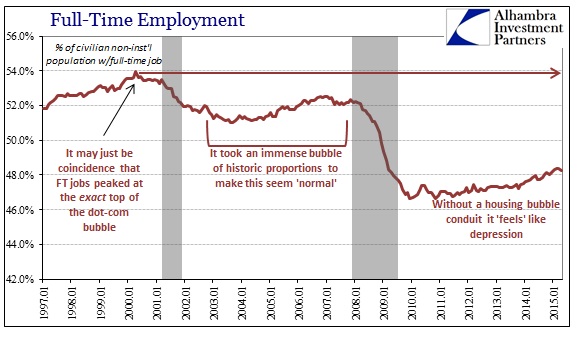

Even for April, the questions abound as to what exactly businesses were doing. While the Household Survey rose much less than the Establishment Survey, the count of full-time jobs, the major deficiency in all of this, subtracted by 252k though supposedly offset by a gain of 437k in part-time positions. While neither of those figures are near accurate enough, the persistence of the full-time “problem” over this entire time explains almost everything about the economy outside the orthodox perceptions (and why that perception never seems realistic).

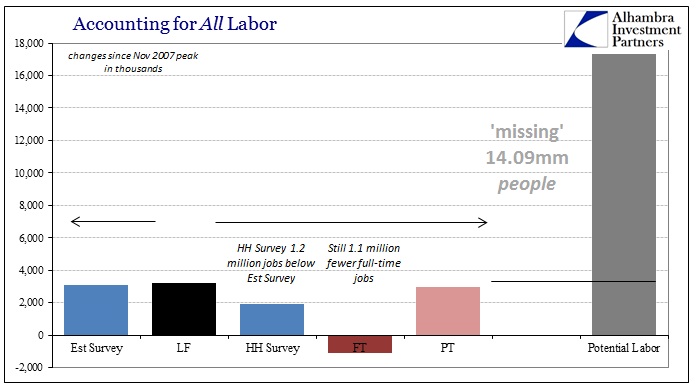

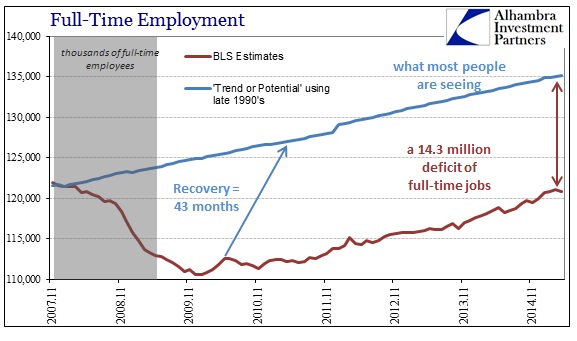

Measuring this “recovery” peak-to-peak, as is proper, the total of full-time positions moved further away from the November 2007 prior cycle end/start. That leaves this “recovery” with 1.1 million fewer full-time jobs without even accounting for the 17+ million that have come of working age during those seven and a half years.

Stocks are at record highs and 14+ million people have fallen off the face of the employment statistics altogether, and economists are saying that tepid growth is “just right?” There is no way to reconcile those economic realities without consigning logic to rationalization. To justify record stock prices as they are requires those lost 14 million to rapidly become absorbed in actual job creation of an actual recovery rather than this pretend version we have been having, especially of late.

Even the vaunted Establishment Survey has seen a slight bend in its otherwise straight-line march in 2015; along with the HH Survey and, again, the LF. Weakness has been apparent throughout this piece of the “cycle”, but as with so many other indications it seems as if there has been at least another downward pull in economic gravity.

That would suggest even trend-cycle overenthusiasm can no longer offset the growing “slump.” The Establishment Survey does not actually measure the count of payrolls in the US economy, though that is exactly how it is taken, especially the adjusted figures that have been taken as recovery gospel. The BLS itself describes what it does do:

The Bureau of Labor Statistics (BLS) adjusts the data to offset the seasonal effects to show non-seasonal changes: for example, women’s participation in the labor force; or a general decline in the number of employees, a possible indication of a downturn in the economy. [emphasis added]

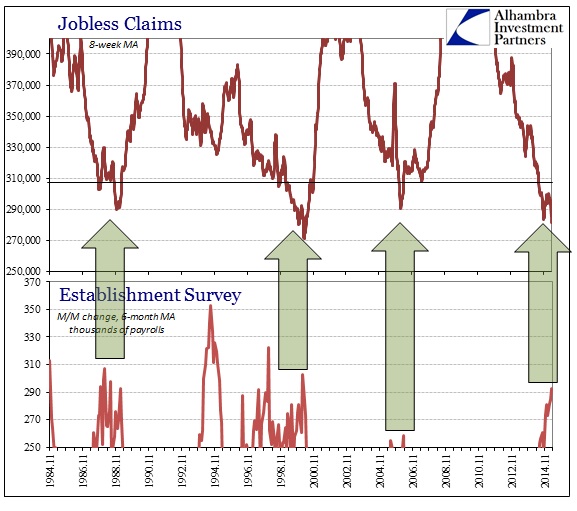

That last part highlighted above is trend-cycle variability analysis, but it doesn’t just pertain to the recession part of the cycle. It could just as easily be the BLS over-estimating an upturn, one that is based on a shaky correlation with other economic accounts that have turned over in the post-crisis era. I still think that jobless claims are being used to describe just such an upturn, and the BLS is applying an upward variability through its trend-cycle “seasonal” component that over-estimates the level of gains in the Establishment Survey in particular.

If that is the case, then the actual figures for jobs in 2015 are much worse than described by these latest “strong job creation” numbers that are just perfect enough to allay some fear but keep Janet Yellen from doing something bubble crazy. That would likely mean that jobs were contracting in March, where the downward-revised 85k gain might be all statistical anomaly (and then some). And April might be that much less reassuring away from the Goldilocks bubble.

As it is, there is just nothing to suggest a cyclical upswing in economic fortunes, and certainly not in anything as vital as labor expansion. The incongruity simply stands out, but “nobody” wants to admit it because everything is invested (literally, in some cases) upon nothing ever going wrong. That is not a recovery, or even an economy; it is the continued rationalizations of bubbles and authoritative, activist policies that will not accept anything other than financialism. The entire recovery idea, especially in these payroll pieces, is entirely dependent upon factors that don’t even hold internal consistency.

The rise of the stock market, in particular, in relation to ZIRP/QE has been predicated all about the future, regardless of whether the future always seems to stay there. In other words, it is enough, apparently as these economists describe, that the idea of future growth better than now can sustain the bubbles. What is lurking here is the especially unpalatable recognition that the divergence between future growth expectations and the fact that we are living much, much closer to that future is no longer just the unspoken downside beyond the 14 million.

Stay In Touch