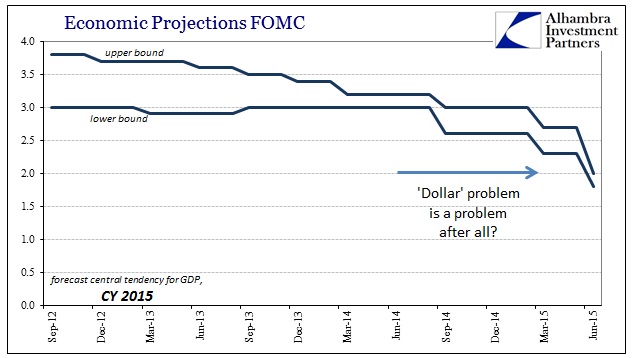

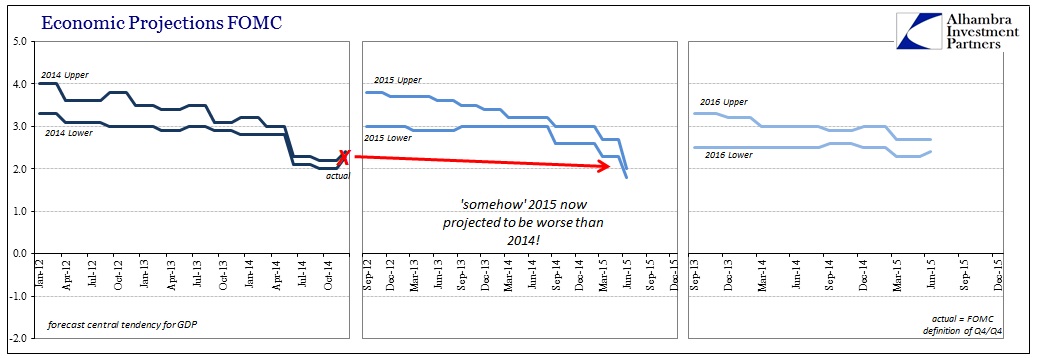

I am more convinced than ever that the FOMC is simply trying to scare a recovery into existence. The June update to the Fed’s models for central economic tendencies were, in a word, atrocious. The economy was marked down in almost every facet, and not by a little. The upper boundary on the central tendency for GDP was dropped by 0.7%, all the way to just 2% from 2.7% at the March update. That means, given the current thinking which somehow includes an economy strong enough to consider ending ZIRP (from an orthodox perspective), this year is going to be worse than last year.

Somehow out of all that word salad statement, we are to assume that the Fed is even more convinced that the economy has only gotten better if only because it got worse?

Rational expectations is a fickle master, creating all sorts of nonsense and circular logic that passes for coherent association and discipline. It’s no longer the first quarter and potential “seasonal” problems with the data, the FOMC and its academic arm just acknowledged that the “slump” has gained so far as to engulf at least the entire first half of 2015; a time period that was never supposed to be even in question given all the protestations that came out of last year (5% GDP and all that).

From December:

The solid growth could clear the path for the Federal Reserve to increase interest rates in 2015. While there is some trepidation about the first interest rate hike in nearly a decade, it would signal that the U.S. economy in [SIC] actually strong enough to take off the training wheels.

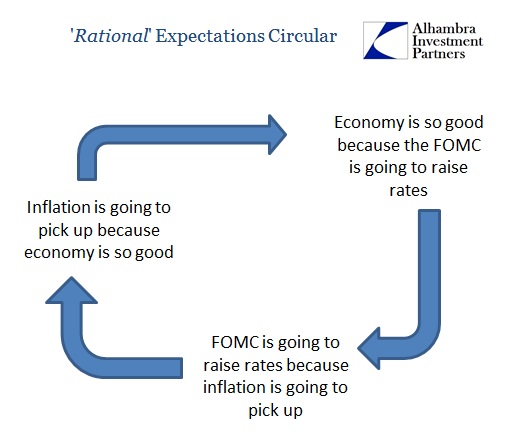

I think that is the entire point, right down to the rational expectations root. The Fed is going to raise rates (or, in actuality, make you think it wants to so bad that you think they actually might) in order to signal a strong economy, in order to get people acting like a strong economy, in order to create a strong economy.

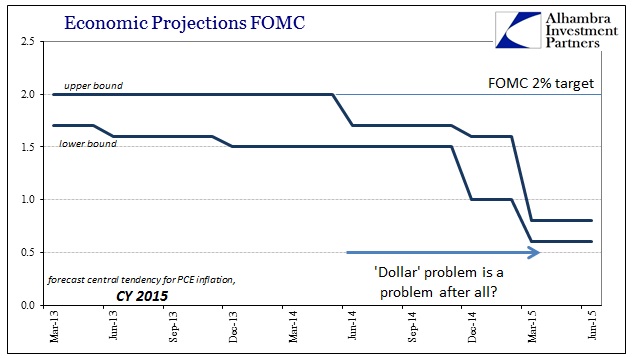

By all consistency with orthodox understanding, the FOMC in its projections just gave itself far more room not to “tighten.” Their inflation projections are now the opposite of what they were saying just a few months ago when low oil prices and a “strong dollar” were thought to be actually strong. Low inflation, close to disinflation in the orthodox textbook, is no longer viewed as “transitory.” The new forecast features, as it always does, a pickup next year but not reaching the 2% target on the PCE deflator until 2017.

As late as June last year, these same economic models were expecting “inflation” at or near the target limit for this year. The fact that the “central tendency” now forecasts less than half would, under any other circumstances, be leading to the exact opposite interpretation of monetary objectives. Also from December:

A U.S. economy that suddenly looks healthy—50 straight months of job gains, best quarter of growth in 11 years—is falling short in a key area.

It isn’t luring back many of the millions who dropped out of the labor market during the down times. That failing nags at many economists.

Federal Reserve Chairwoman Janet Yellen monitors the declining share of Americans working or looking for work as a measure of slack in the job market. She has cited the low labor-force participation rate, as the measure is formally known, to justify the Fed’s long easy-money quest to stimulate the economy and boost wages.

That shortcoming should have at least produced some healthy skepticism about the jobs numbers to begin with, especially since they aren’t joined by anything else – even GDP has shown that any economic “anomaly” in this cycle is to high side. By both of the Fed’s dual mandates, then, the rules it dictates to itself, there is absolutely no reason to expect a rate hike. Neither inflation nor a comprehensive view of labor argue for it. The only way in which to prefigure a change in monetary stance is a last ditch effort with which to, again, assert rational expectations doctrine that is increasingly irrational if not totally unhinged.

Whenever I get to discussing “rational expectations theory” the typical response I get is one mostly of disbelief, as in whatever and wherever the theory is applied seems somehow to offend basic common sense and intuitive sensibilities. I don’t disagree at all, as I am not one to subscribe to the theory only observing how it fits within the paradigm of monetary economics – you don’t have to agree with it but you better understand it so you can better analyze why the Fed does what it does.

The reason “rational expectations” grates so much upon basic observations is that it is a symptom of orthodox economics’ dominating tendency to make reality fit its models. In other words, “rational expectations” is nothing more than a mathematical variable in a set of equations designed to generate a “generalized equilibrium.” Yet another way of thinking about it is that the math is so narrowly defined and construed “rational expectations” is the means solely by which the equations are solvable without disqualifying infinities.

Since the math works under these assumptions, economists have set out to define their view of the real world to match the math, which is why it often sounds, essentially, ludicrous. Among those “fitted” properties is market efficiency. Rational expectations essentially forces markets to be perfectly efficient to keep the paradigm logically consistent

That is the essential doctrine here, namely that if the Fed can get markets to act like there is a recovery (now or later doesn’t actually matter; it could be based on unicorn suppositions for all the theory counts) hence there is a recovery because markets are never wrong under efficient market hypothesis. Thus the dots – even though the dots in June are working against the whole idea (having been adjusted more than a little toward the con case). The FOMC is issuing commands about the vital credit market factor of interest rate dynamics, no matter how much so far the credit markets fail to follow.

At one of these previous and ridiculous Fed meetings I wrote that there is an inverse proportionality at play, namely the further the economy strays from the intended baseline the more vociferously orthodox economists and policymakers (redundant) would protest otherwise. Everything about this FOMC meeting suggests that there is nothing to suggest a recovery; and in fact the economy in 2015 was just reduced to something worse than last year’s deficient pace despite the fact that every FOMC member up to and including Janet Yellen spent months and months last year and a good part of this year telling everyone that was completely impossible. Rather than admit the mistake, they harden toward the mistaken assumptions.

In 2008, at the outset of the Great Recession, the confusion in the policy meetings was at least somewhat genuine – they really had no idea and were just making it up; hope really was a strategy. Somewhere between then and now, monetarism changed. Maybe that was due to the persistent and obvious failures to actually deliver what was promised (instead, having to constantly reduce standards and grope for even the slightest tangible evidence that there was some good if small effect outside of dangerous asset price imbalances). There was always a command element to increasing activism on the part of central banks, all the way back to Alan Greenspan and the first shift to interest rate targeting in the 1980’s, but it was more implicit; almost a friendly suggestion that at least attempted to maintain the illusory idea that it was all free markets and capitalism. No more.

In June 2015, the commands of the central planners are almost openly mocking common sense. George Orwell wrote in Animal Farm,

No one believes more firmly than Comrade Napoleon that all animals are equal. He would be only too happy to let you make your decisions for yourselves. But sometimes you might make the wrong decisions, comrades, and then where should we be?

Where would we be indeed.

Stay In Touch