By the behavior of the Chinese yuan itself, given the financial size here, we can readily assume that any “dollar” problem that is clearly causing the PBOC’s actions are sizable. Currencies throughout Asia are being roiled not unlike 1997 and oil prices sunk to a new “recovery” low. While that all suggests far away turmoil relevant only to those foreign shores, there are many domestic and internal eurodollar problems that leave little doubt about unification and singularity. As I wrote this morning, there is only one currency war and that is the “dollar” as it implodes onto itself.

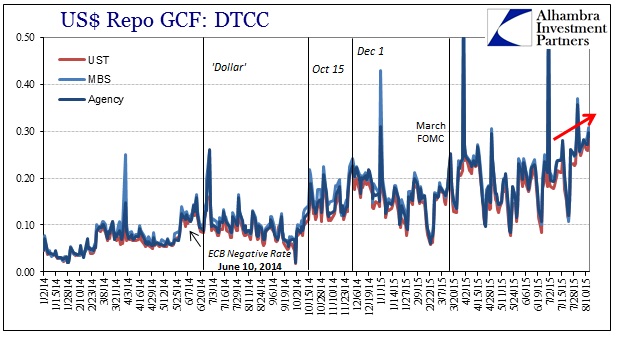

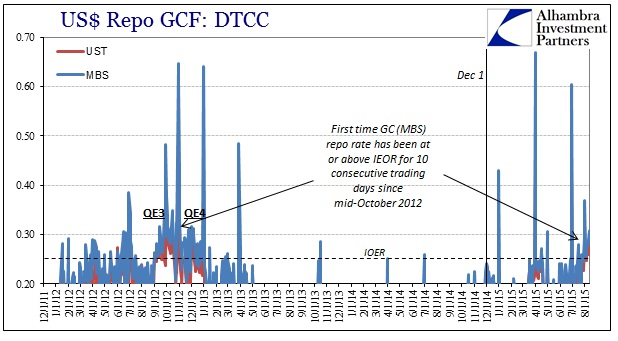

The spread of financial irregularity, including stumped and deviating central banks (the list only grows, PBOC the latest casualty), signals the decay that began on August 9, 2007, as it has accelerated since last year. Internal interbank rates have risen, especially lately, which is central to all this “dollar” turmoil. Repo rates surged in the past two weeks, and while the GC rate paused yesterday (MBS down only from 30.7 bps to 30.1 bps), it remains at a noticeably elevated station.

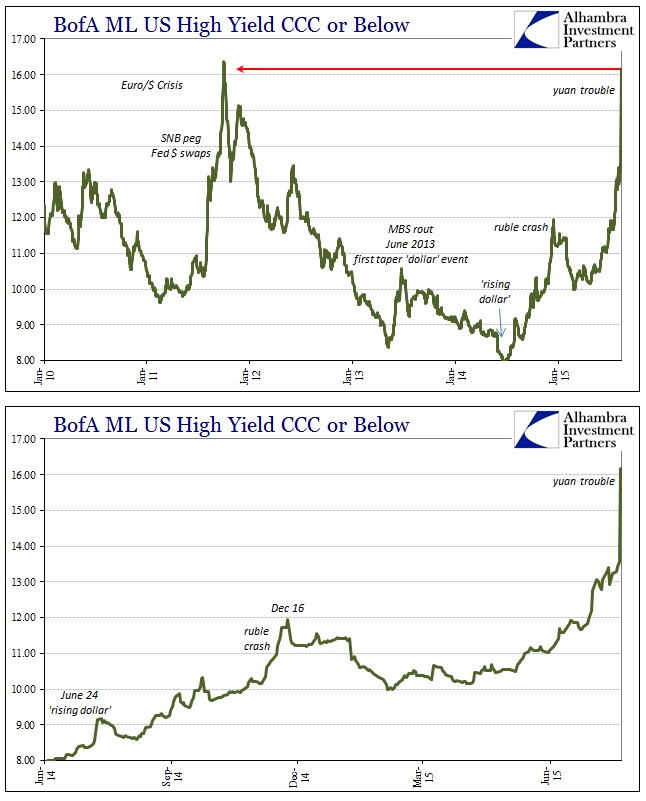

With all that in mind, Jason Fraser of Ceredex Value Advisors alerted me to greater and certainly related turmoil in the less visible high yield spaces. The Bank of America/Merrill Lynch High Yield CCC Yield got absolutely slammed yesterday, rising from 13.58% to 16.18%! That would suggest, as all listed above, that there has been inordinate and tremendous “dollar” pressure not in foreign, irrelevant locales but creeping into the contours of the domestic and internal framework. While that may be energy, as Jason points out, it cannot all be energy.

The surge there far surpassed the 2013 summer meltdown and actually equals the 2011 crisis crash.

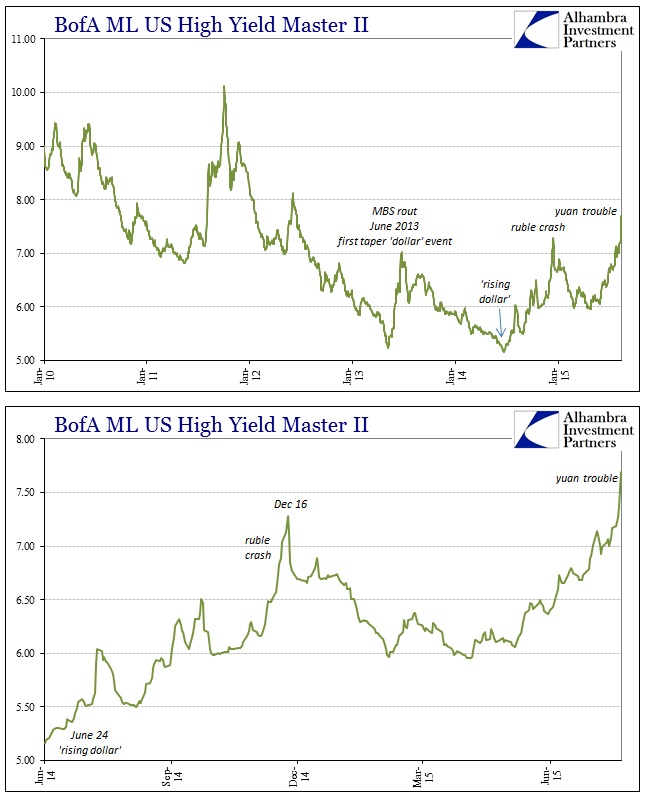

In fact, other junk indicators were similarly taken out in a manner that we have seen before. The Bank of America/Merrill Lynch Master II yield was far less dramatic but still indicating a serious liquidity event in that risky space. As both yield indices make plain, the last time prices were so slammed was early to mid-December – right when the ruble was crashing and the franc/dollar problem was testing the Swiss National Bank’s last resolve.

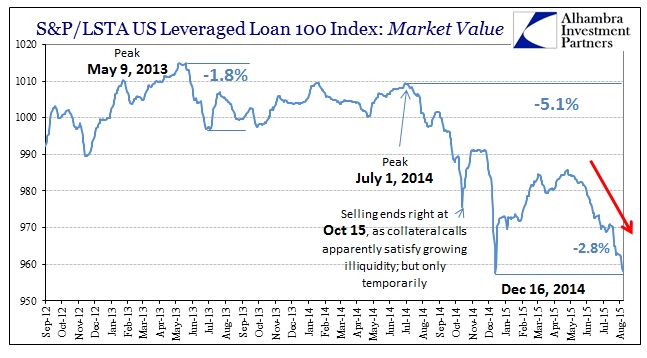

December 16 also marked the low point in the S&P LSTA Leveraged Loan 100 Index. When last we left that part of the junk/risk market, it was selling off and only a few ticks above that December low. S&P has not updated its figures for the index since August 10, curiously going dark during all of this “dollar” turmoil. I emailed them directly for clarification, and the response I got was, “Just a lag in getting the data.”

I have no specific reason for doubting the sincerity of that reply and explanation, though I can’t help but note that it is awful curious that they would be having such pricing problems when the rest of their similarly situated class within the corporate bubble is as churning and possibly illiquid as the yuan. I cannot recall a similar lag in updating the index, but, again, I have no specific inside knowledge on their internal workings.

The cumulative assessment of all these factors, great as they are in their individuality, is that the global financial system just endured this week another “dollar” run. We can say with some reasonable assurance there was one in early December, as well as one centered on October 15. They seem to be increasing in intensity and now reach, penetrating deeper into the bowels of the “dollar” system as well as taking down central banks with each successive wave.

As I wrote, again, this morning:

The higher currency fix signals that whatever great “dollar” run hit the China funding markets this week may have passed – even if only temporarily. In short, the actions of the PBOC, seen in light of what was a convertibility mini-crisis, a “run” of sorts, make sense where the yuan fix as some kind of “stimulus” in devaluation does not (or is at least far too inconsistent to be explanatory). The PBOC held the yuan steady to a near plateau for five months hoping for cessation of “dollar” pressure, but, like a coiled spring, it only intensified until there was no holding back anymore.

It will be interesting once S&P updates the leveraged loan index to see how much effect and maybe devastation was experienced there during this run. For now, it seems today as if the acuteness has abated and calm has been restored.

That does not mean, however, that all this is over; far from it. These tremors are warnings that the “dollar” system’s decay is reaching critical points. The mainstream will tender that this is really no big deal, just a tantrum of spoiled markets unwilling to easily treat the coming end of ZIRP and accommodation; that is simply and flat out false. There is a systemic liquidity problem that is and has been fatal, exposed to a greater degree by the continued withdrawal of eurodollar bank participation – the real “printing press.”

In a credit-based monetary system neither the economy nor its ultra-heavy financial component can move forward without ever-growing financialism; dark leverage and all that. There has been a continuous withdrawal dating back to, again, August 2007, but met with amplifications first in 2011, again in the middle of 2013 and then last year. This is not policy but a total systemic reset, as “money dealing” activities have never been settled this entire time. The dealer network simply withdrew starting in August 2007 with central bank balance sheets taking up the slack, belatedly as usual which is why there was a panic and crash. Dealers are again removing what little presence they have left but central banks seem totally unaware that that is the case, and that there is really nothing left for “money” intermediation upon that and their withdrawal.

I wrote back in May upon this very topic, as some very good and smart people, Perry Mehrling and Zoltan Pozsar, were attempting to gameplan the coming monetary shift. My view hasn’t changed, namely that the transition will not be a transition at all, but a potentially awaiting systemic decapitation:

I personally find way too much complacency in blindly believing that going from B to C will be only a minor inconvenience. It would be dangerous even under the circumstances where the system shifted from the dealers to the Fed and back to the dealers, with an infinite series of potential dangers even there. But to undertake a total and complete money market reformation from dealers to the Fed to money funds? There are no tests or history with which to suggest this is even doable under current intentions. Poszar and Mehrling’s contributions more than suggest that difficulty, but I think that still understates whether or not we ever get that far.

This latest “dollar” episode has continued to bear that out. How much further will it go before central banks wake up and see that their fantasy of a recovery and “resilient” financial system was a now-eight year old lie? That is, of course, a rhetorical question as they will not act until all is over. That is the problem, because this hollowed-out global “dollar” is supporting, badly, the main bubble, so the penetration into the corporate space is a highly unwelcome development (though welcome in the long run sense of actual and helpful balance) as this remains awaiting resolution upon increasingly unstable circumstances:

Stay In Touch