We have been talking about a global “dollar” run for the better part of two weeks, and at least a major “dollar” disruption looming going back three months. To say that any of the latest chaos is “unexpected” is intentionally obtuse, but it has already happened. As it is, I think we can expect FRBNY and the Treasury to issue a report in six months that says this morning’s widespread disruption was limited to just 8 minutes of computers surfing too much colocation or something; the last they will ever admit is that they have disastrously failed exactly where they have been proclaiming “inarguable” success ever since taper.

Janet Yellen’s favorite word has been “resilient” because from where policymakers sit asset bubbles can do that – but only for so long. Herb Stein was absolutely right that something that can’t go on forever just won’t. The “dollar” has been a major problem, as the eurodollar/wholesale system, for more than eight years but with a serious reiteration since last June. It was the repo market that first sounded the warning, as once more failures were “unexpectedly” (for a resilient market) outlandish. Though fails, at least, have been less of an obvious figure in the gaining disorder more recenlty, the sad state of affairs has to proclaim, contra Treasury and the Fed, it hasn’t been the same since.

More recently, the pace of the “dollar” run has accelerated remarkably. That has now caught up stocks as this morning taken yet another disastrous turn. All the usual suspects within the “dollar’s” orbit have been plied to new levels of warning or devaluation – save two. I think those now “exceptions” may be the most important part of the past week.

First, the usual:

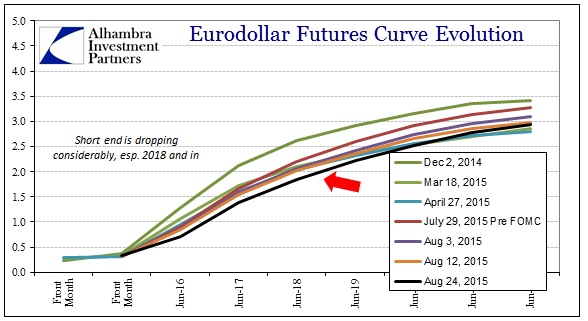

Though repo GC rates continue to decline, money dealing rates in general are showing highly, highly bearish. Eurodollar futures have been bid quite heavily Friday and this morning so far, with the curve now at its flattest appearance (in the all-important “money” end) of this overarching trend. The June 2018 contract, for example, was bid up in price to above 98.14 which is a new record high. The same goes for the June 2017 contract which, at a new high of 98.62 is actually down from 98.70 this morning, up from 98.35 just five days ago.

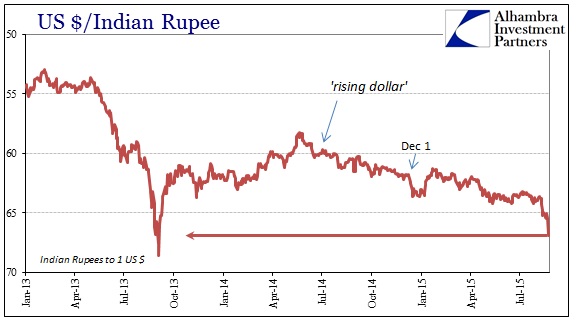

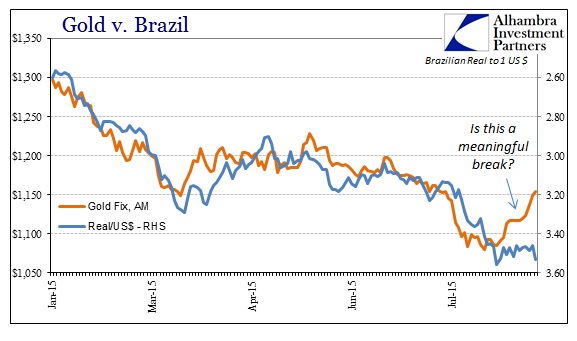

With such an illiquid backdrop, it isn’t surprising to see the ruble at a new low below 70 to the dollar, which is quite below the past crisis points erasing whatever the Central Bank of Russia wished to convey. The rupee is also dropping quickly and the real, having never really moved higher, also at a new low.

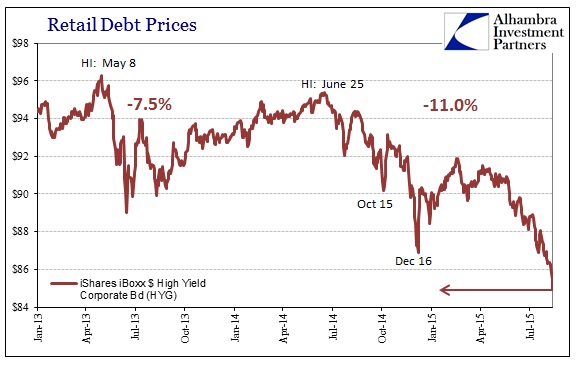

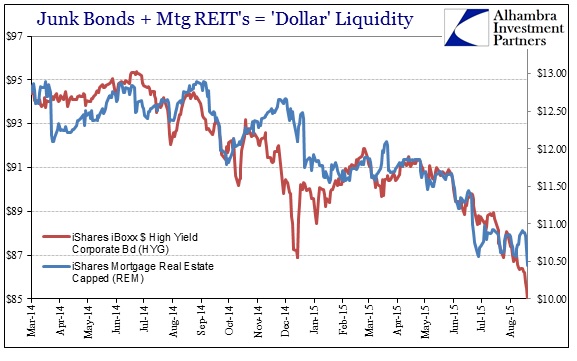

Junk bonds and liquidity indications are also getting sold, with the retail versions or proxies of those at, of course, new lows.

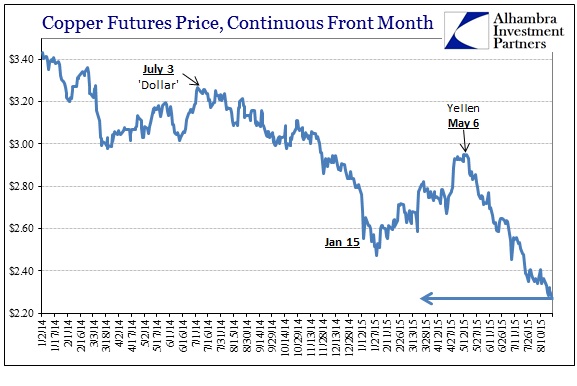

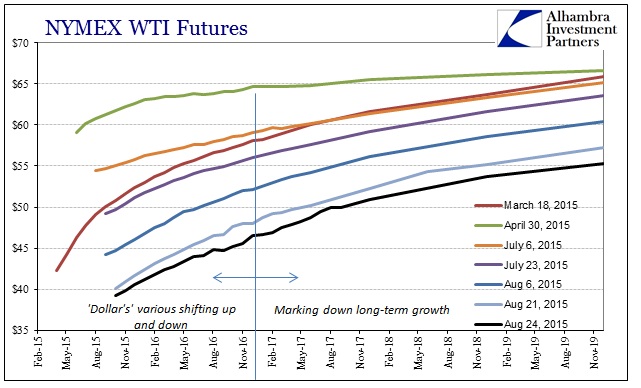

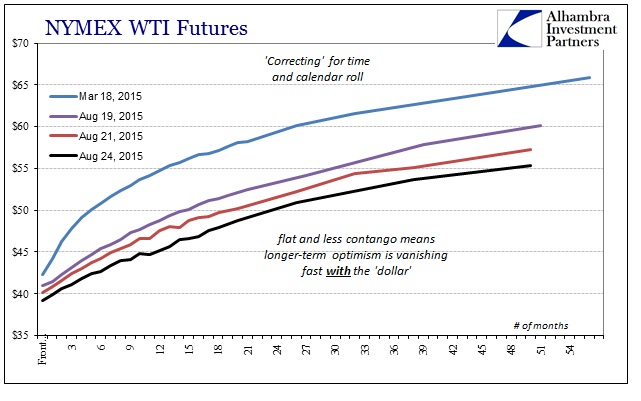

With the “dollar” under such broad strain, major commodities are being sold. Copper for September delivery was sold down to as low as $2.209 this morning, and remains at what would be a new low of $2.245. The WTI curve is, as usual, pummeled all across maturities as, again, the “dollar” has clearly “won” the issue of setting future expectations. The acceleration recently is just extraordinary especially at the back end of the curve which has essentially drained all the remaining optimism from the oil complex.

Clearly, then, the “dollar” is in a widespread run in the intermediate term and especially the past week or so. As I mentioned above, two other “dollar” proxies have moved opposite as you would expect under such financial illiquidity. The first, gold, I suggested last week that it might be the beginning, finally, of the fear bid. This morning, gold was up yet again at $1,153.50 for the AM fix, which is itself noteworthy because that was the worst of the illiquidity. Gold managed to sneak by all that and even was bid further into the PM fix, $1,166.50, which is the highest since July 3 and the start of this “dollar” run.

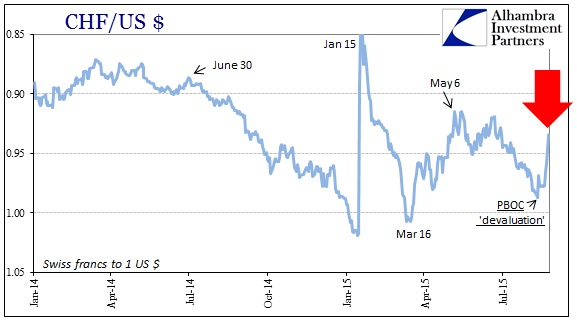

Gold is no longer alone, however, as the Swiss franc has joined it in the “opposite” direction. The Swiss are highly exposed to any such “dollar” illiquidity as January 15 demonstrated beyond all doubts (at least to those that understand wholesale dynamics) and yet in the past week the franc has not devalued once more as it had up until the Chinese and PBOC were broken. In other words, the franc was dropping back toward parity yet again like every other “dollar”-touched currency until August 11. Since then, the franc has totally reversed, jumping from nearly 0.99 to about .9345 this morning.

Given the franc’s history and reputation, despite its recent massacre, that can only be a safety bid. Like gold, then, it would seem that we may have moved beyond straight illiquidity into something far, far worse since central bank inspiration and their trivializing all downsides were the only market props. It is one thing to basically play down October 15 as just 12 minutes of haywire computers, but as these same signals repeat, intensify and expand that becomes increasingly unhelpful even to those that desperately want to believe the fantasy – in no small fact because all these events are essentially breakouts of that same, unalleviated financial erosion. So it is these two reverse “dollar” trades that are perhaps the most important developments into this clearly ongoing “dollar” run.

Stay In Touch