Part 1 can be found here

Long before Bear Stearns, there was Countrywide and a glimpse into the yawning abyss. But there was also Northern Rock, a UK bank, and a series of tremors and earthquakes rumbling across Germany. It was an entirely surreal period, as the once-mighty German system ground to a spectacular halt on, of all things, US subprime real estate “products.” At least that is the mainstream version, though, like most everything else, there is far more to it.

By February 2008, state-owned bank KfW had bailed out IKB Deutsche Industriebank which only led to an eventual “rescue” for KfW along with several others:

The list of casualties from the US subprime crisis is long and keeps getting longer. Financial institutions around the world have announced massive write-offs due to the credit crunch, with German banks such as WestLB and Sachsen LB being particularly hard hit by their exposure to obscure subprime-related investment vehicles.

All that led, after Lehman, to a full German state embrace of bailouts, massive in its size and attempted reach. Like TARP,

The €480 billion ($672 billion) package was approved by the government, whipped through the upper and lower houses of the German parliament and enacted — all in the space of five days.

Also like TARP, it didn’t work. No matter the size, Germany’s second largest bank, Commerzbank, was accepting a government bailout by January 8, 2009. The Berlin federal government took a 25% stake in the bank at the same time Deutsche Bank, the wholesale giant, was rumored to be looking at the option; at least as far as participation in the bailout umbrella, especially what would have been the favorable (to Deutsche) development of a single, huge “bad bank”. Along with remorseless UK bank troubles and nationalizations, these moves kicked off that last leg of the panic – all foretold by wholesale irregularities that continued in late 2008 such as the sudden and confusing appearance of negative swap spreads despite all the global and massive “rescues”. Traditional remedies, even in the size and reach of the post-Lehman global environment, were just no match for wholesale dynamics.

From the perspective of orthodox economics and monetary economics, none of this made sense nor has it cleared up any in the seven years since. From the perspective of wholesale finance, it makes perfect sense which is why reliance on central banks for rescues and solutions is dubious in multi-dimensional fashion.

At issue is, and remains, the “dollar.” The fact that Germany’s banking system ground to an emergency halt on US real estate structured finance proves, without ambiguity, the long ago death of the dollar and the emergence and domination of the “dollar.” As noted in Part 1, central banks operated under the self-guided delusion of the dollar while the “dollar” burned its way unalleviated and undeterred through the whole global economy. It was such a massive financial conflagration that we still are living its effects and with greater intensity of late.

While most convention still dwells on “toxic assets” and duplicitous lending and underwriting standards for the eventual panic, those are but symptoms of the causative transformation. The true nature of where all this came from, and where we are going, was captured in 1979 in a nondescript FRBNY magazine article that I quoted in that Part 1. I will reproduce it here as the risk of redundancy is overwhelmed by the necessary emphasis for ongoing clarity:

It has long been recognized that a shift of deposits from a domestic banking system to the corresponding Euromarket (say from the United States to the Euro-dollar market) usually results in a net increase in bank liabilities worldwide. This occurs because reserves held against domestic bank liabilities are not diminished by such a transaction, and there are no reserve requirements on Eurodeposits. Hence, existing reserves support the same amount of domestic liabilities as before the transaction. However, new Euromarket liabilities have been created, and world credit availability has been expanded.

To some critics this observation is true but irrelevant, so long as the monetary authorities seek to reach their ultimate economic objectives by influencing the money supply that best represents money used in transactions (usually M1). On this reasoning, Euromarket expansion does not create money, because all Eurocurrency liabilities are time deposits although frequently of very short maturity. Thus, they must be treated exclusively as investments. They can serve the store of value function of money but cannot act as a medium of exchange.

The true nature of the panic in 2008 is captured in that second paragraph as set up by the argument of the first. For the past four decades, central banks have been operating on the assumptions embedded within that second concept; that eurodollars, the “dollar”, are not money or at least fully so. Because they operate offshore in only bank balance sheet existence they require not just an accounting deviation but a transformational step to turn those “dollar” assets into usable currency. From a central bank perspective, then, eurodollars can be irrelevant since it would be far more efficient and effective to simply focus on currency only beyond that step.

This much sounds simply plausible, as what is appreciated widely of banking is the money multiplication process whereby deposit liabilities are the central focus; and thus the primary source of fulfilling all the roles of money including and especially medium of exchange. Quite simply, you cannot take a eurodollar into the grocery store and expect to emerge with the fruits of commerce (apart from the fact you can’t really describe the exact form of a eurodollar). Orthodox economics demands that transformation of a eurodollar in whatever practice into a local deposit liability in order to meet that monetary need. And so the Fed might ignore the eurodollar market in order to meet its obligations which are self-limited to the lower tiers of the “M’s.”

But is all that actually true? Are eurodollars mutually exclusive of full monetary agency?

The continual “synod” of German banking, as global banking, starting August 9, 2007, answers against both by changing the nature of the whole discussion. From the very start, eurodollars have been complete money in at least the realm of global trade. Once the Bretton Woods system was finally dismantled in 1971 (it had begun the process almost fifteen years before that) eurodollars became every bit of full monetary equivalent for global exchange. A Brazilian company wishing to import Saudi oil in the 1970’s required neither gold nor physical Federal Reserve Notes to do so; they simply opened a credit line with a eurodollar bank (the very process described in the first paragraph of the 1979 passage quoted above) and oil arrived as scheduled. That would be the very textbook example of full monetary function even if the manner in which the eurodollar liability at the eurodollar bank supporting that new “dollar” loan is in great dispute and complexity.

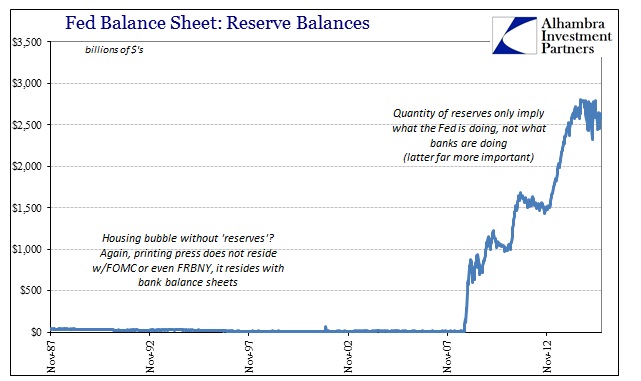

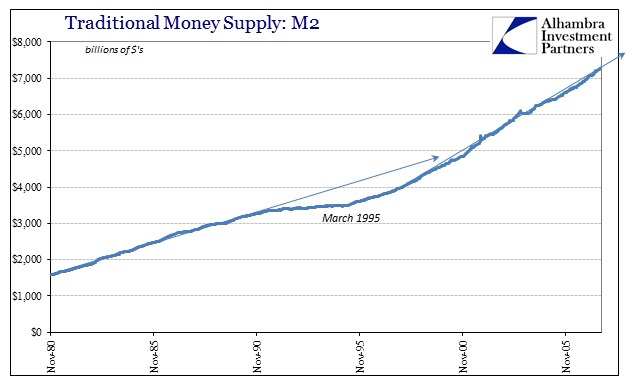

The domestic equivalent is no less conclusive if but a few steps further removed. If you go looking for the housing and dot-com bubbles in “high powered money” of bank reserves and deposits, you only catch a fleeting glimpse in the latter. The Fed’s direct influence is nowhere to be found, but you do see a noticeable uptick in M2 right at (when else?) early 1995.

From the Fed’s basic perspective, there are no bubbles in M2 because they have monetary causation reversed. For orthodox economics, under largely money multiplier-type assumptions, banks make deposits as they make loans therefore the two are tied together which is what allows the Fed its control mechanism even under the more dubious interest rate targeting scheme. In the wholesale system, however, assets get created as do liabilities that are often (mostly) nowhere near deposits. The use of a deposit account only shows up when those wholesale liabilities and assets are eventually aroused into traditional usage.

To follow the process of wholesale money creation is quite dizzying, but very simple in that end arrangement. I don’t want to deviate too much into the opacity of “money creation”, but you can get a very good sense of it by recounting how structured finance, particularly in mortgage “products”, actually works. I wrote the following in May 2014 to demonstrate the instability and general upset and destabilization of money markets at that time as I saw it:

The slight rise in mortgage rates last year unleashed a collapse in mortgage lending – the pipeline dried up. To say it was unanticipated by the “market”, especially policymakers, is an understatement (yet again). So when the Open Market Desk went about setting its policy-related purchases, it was buying ahead of that collapse, setting up what looked like a liquidity event. Because the pipeline was ultimately much lower upon settlement than at first believed, there was far less supply available to the market for liquidity.

There is actually even more nuance to consider. For some MBS issues, particularly those of benchmarks, the pipeline/gross issuance problem can be reduced because there is a large reservoir of loans that can be delivered into existing TBA positions should issuance conditions become unstable. That would mean pricing in those benchmarks would see little disruption or volatility. For those production coupons without deep pools, an issuance disruption would likely lead to premiums and stratification of pricing – fragmentation.

But the Open Market Desk has the ability to adjust its pace and program based on implied conditions in TBA. If it senses a tightening of supply/issuance relative to settlement, they can, according to Treasury Market Practices Group Best Practices, sell dollar rolls. While that sounds like a circularized stack of Federal Reserve Notes with a rubber band wrapped tightly around, a dollar roll is just another (why not) derivative contract. Selling dollar rolls effectively postpones settlement of any expected deliveries into the production coupon security.

These dollar rolls function much like the securities lending program out of the SOMA portfolio. In rough terms, as the Open Market Desk takes these securities out of the “market” through its “purchase” operations, it has the ability to open a valve and allow them to flow back in. This is, however, by no means a perfect substitute, as you might imagine. That is an important concept.

Peering into the sausage-making of MBS securities finds no deposit liabilities (in the general sense) but a whole array of wholesale liabilities including and especially various forms and scatterings of dark leverage. From underwriting and warehousing to GSE stamping, this system works in the same manner with and without the Fed’s QE interruptive flows. The deposit in one of the M’s only shows up when the asset is converted for actual economic use; almost everything else in between is just ledgered wholesale liabilities, which is why I often describe the wholesale “dollar” as chained liabilities – though with the extremely important caveat, as I wrote about last week, that there is no beginning or end to the chains.

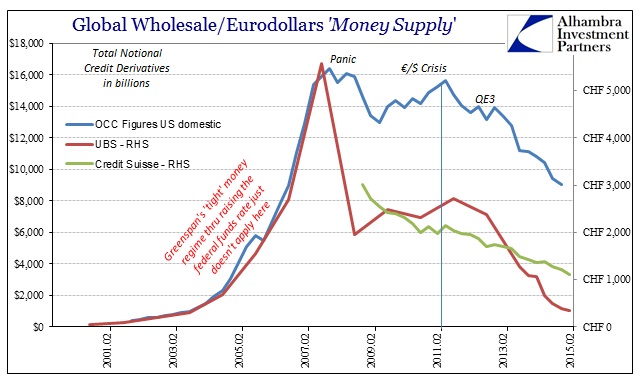

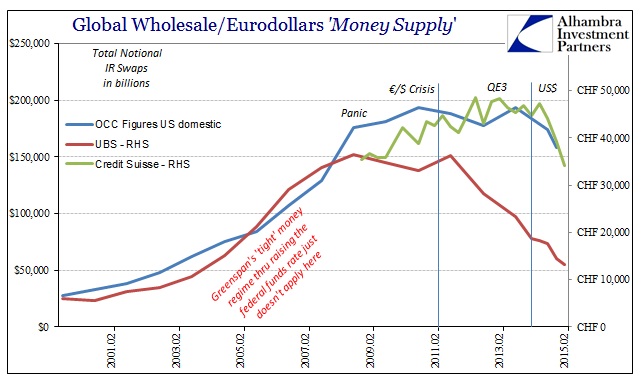

Thus, deposit accounting and traditional money sits at the end of the wholesale process as a byproduct of its profound inefficiency (in real economic terms). The Fed viewed a stable money supply growth without appreciating the huge monetary growth in the eurodollar works behind it. That is why we can see nothing of the asset bubbles starting in 1995 in M2 but yet, as the BIS tallied, foreign bank’s foreign claims (US$ wholesale debt assets, primarily) would at the same time rise from $10 trillion to $34 trillion. And we know the support of that huge expansion (which is greater than implied by those BIS figures, since they only cover European banks or just one segment of the eurodollar whole) from even the anecdotal reviews of dark leverage through gross notionals of derivatives. M2 growth was stable, which comforted the Fed and global central banks, but dark leverage was just bursting and in different forms:

In short, Greenspan and then Bernanke were attempting soft central planning by only observing the end of the huge and encompassing process, and therefore believing that it was quite successful even after the dot-com collapse (which was, in this context, a warning along these lines). Instead, the disparity between the wholesale explosion and relatively benign pace of M2 only signified just how dangerously inefficient the system was in economic terms, let alone as asset price inflation of bubble proportions. That is why, to them, “global savings glut” seems to apply and why the FOMC so spectacularly failed to identify and move against the geographic irregularity of the “dollar” starting August 9, 2007 (fragmentation of eurodollars in London as LIBOR moved higher while federal funds moved lower).

What I just described may not make eurodollars completely fulfilling of all monetary mechanics in narrow practice, but what becomes clear, and what is truly fascinating, is that such a distinction appears no longer so meaningful or even relevant. The reason money evolved to incorporate all its given functions was that it was and had a center; a physical quantity to be at least converted in traditional finance. Wholesale finance has no center; it just is. Such pliability and flexibility is both frightening and freely imaginative all at the same time, a multi-layered structure that delivers ordered and tiered monetary properties at each derivative level (for example, collateral acting like currency) yet influencing and connecting at each along the way in dynamic fashion.

It is as if money behind money even though there isn’t any actual and true money in any of it (which is why they system could evolve in this manner). The eurodollar system financially supports (and denies) economic money as it is in the current global paradigm and that applies to not just what is available for spending and actual commerce but also asset prices globally. The chains of liabilities act free from, mostly, central bank influence except in the perceptions of that influence upon profit considerations of these bank balance sheet functions.

The tragedy of that 1979 warning, as that is what it was, essentially, is lack of imagination in favor of the alluring (from the view of any prospective central planner) illusion of control. To see the financial world so opened up by the possibilities contained within wholesale elements as they related (and not) to traditional monetary mechanics would be too infinite for a “discipline” counting on nothing more than regressions (a static world). There is much to admire about wholesale potential, at least if it had held to true and benevolent purposes. There is little to admire in how it developed quite against the market nature of money in its absence because there is nothing to admire in how central bank control became all that mattered to the detailed exclusion of actual control itself.

Stay In Touch