The focus on China as if their problems were only Chinese is highly misplaced, though you can understand the appeal of the excuse. This sentiment was expressed over and over today (just as it was in August):

Do we all live in China now? Investors could be excused for thinking that, given that arcane indicators such as a Chinese manufacturing index and the value of the Chinese yuan are inducing nauseating drops in the U.S. stock market. And the surprise halt to trading in the latest Chinese session, a mere 30 minutes after markets opened, has thrown U.S. and European markets into a tailspin.

Last we checked, however, the Dow Jones and S&P 500 indexes were composed of U.S. companies that might do some business in China, but still earn the vast majority of their revenue elsewhere. And elsewhere, economic fundamentals are looking way better than the gloomy start to this year’s trading would suggest.

This is one of those forest and trees moments that get caught up on the surface of anachronistic thinking. Even if all that were true, the fact that China is an export economy having trouble finding any sustained and sufficient demand for its industrial capacity is a direct reflection upon global “demand”; which still includes the same business climate that US companies derive their revenue and earnings from.

But it never really is so much about business today as it is risks for business tomorrow. In raw terms, if Chinese firms and its economy can so struggle in this environment it stands to reason to at least contemplate why that might be – and how that might directly reflect on domestic considerations. Further, as noted earlier, risk perceptions have changed as the FOMC is no longer given blanket faith to declare whatever sky color they wish. Stocks really haven’t had much success, overall, in a year and a half; a pause that itself should register as complimentary to the Chinese struggles.

The S&P 500 is down just over 7 percent from its May high, but the average stock in the larger S&P 1500 was down 24 percent from its high as of yesterday’s close, according to new research from Bespoke Investment Group. A bear market is defined as a decline of 20 percent or more, meaning the average stock has already reached that threshold.

As Bespoke points out, the pain in stocks is not just energy-related shares. Small caps are among the hardest hit (the average stock** in the S&P 600 small cap is down an astounding 28% from its high!) as well as consumer discretionary stocks; the very sorts of economically-sensitive issues that should be leading the market if this was just China as China. Instead, they suggest China is, again, finding difficulty in no small part because of intensifying US struggles. That much has been obvious from trade figures which declare in no uncertain terms the great and ongoing lack of US “demand.”

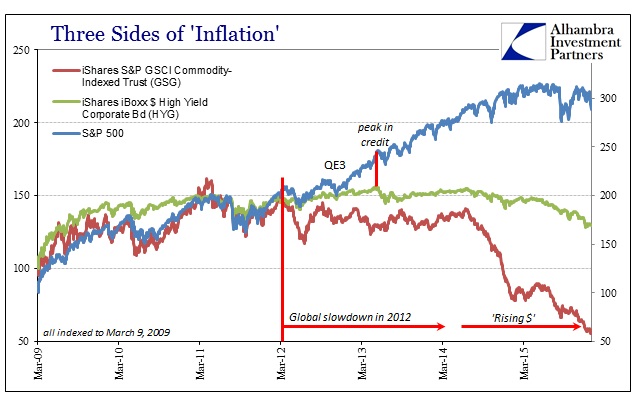

From that visible contradiction, the entire risk paradigm is shifting more so than it already has. Commodities and “money” more broadly are winning the argument, so to speak, having declared long ago greater downside risks. Now that those are becoming rapidly the actual baseline, even for stocks, what is taking place in China is the connected realignment of monetary condition in that frightening direction. Stocks are finding more downside volatility because stock investors are being forced to recognize in truly comprehensive fashion that there is an actual and sizable downside.

This is increasingly taking on the proportions of a global reset. As such, the “dollar” stands right in the middle of it as both messenger and agent. You cannot separate China from the whole as China isn’t really the problem but rather the most visible symptom of it. If there were a full recovery as the FOMC claims in moving against the possibility of overheating, financial firms would be at the front of that greedily taking up the mantle of raw financial opportunity. They did so in times past, usually in direct relation to the QE’s – and were only burned for their trouble. There is no recovery opportunity, which is why they have been retreating in “money” in really precipitous fashion.

It is the very mechanism of discounting. The fact that stocks may also be participating is a very important indication of how much that has penetrated into broad and systemic perceptions. China matters, but not so much just for China. The US may look lackluster (to some, a narrowing minority) by comparison to the direction of China’s economy, but that really doesn’t tell us as much about tomorrow as is repeatedly claimed. A chronically ill economy is highly susceptible not to catching fire and taking off, but rather to converging with all the very real disasters already spreading globally – the risk that money markets are increasingly discounting and carrying out. Financial markets are obviously more and more worried that memories of lackluster will be all that there was of the QE-driven cycle.

**CORRECTION, an earlier version incorrectly stated that the S&P 600 was down 28% from its high. The average stock in the S&P 600 is down 28%.

Stay In Touch