Central bankers have impeccable usually PhD level credentials from all the right places. Because of that, it is simply assumed that they are the preeminent experts of how any economy works. In reality, however, the term stamped on each of their doctoral degrees is highly misleading. Though it may say economics, it was really and truly nothing more than a rigorous training in statistics and regressions.

The word “economics” itself is derived from the Greek; Latin oeconomia from Greek oikonomia, meaning “household management.” It wasn’t until the 17th century that more cumulative study was made turning the aggregate decisions of households into the national product of centralized understanding; political economy. Thus, there has always been a natural tension between what happens of and for the individual and what might be the consequences of individual choice for the whole. That prospective divide turned into active national policy in the Great Depression when economists blamed individuals taking individual action for social economic breakdown (a form of socialism).

To “cure” the “disease” of individual choice, it was first proposed remedies to rescale the balance of power in money. Gold was outlawed, thus treating money financially instead of in its proper custodial arrangement. The reasoning for doing so was straightforward; individuals who were rightfully concerned and even fearful of the Great Collapse after 1929 were “hoarding” money that could have been used to stop the collapse, or at least attenuate its damage. If the socialized economy were to be realized, then individual emotion must be reduced in its reach such that the enlightened few could prevent the worst consequences (if not, as they claim from time to time, such as the late 1990’s, create positively utopian trends to begin with).

For that activated Platonic ideal to become real, it places a great deal of power and responsibility in the hands of a very few. That is true not just in Lord Acton’s phrase of human frailty, but also inasmuch as said humans must possess enough understanding of the subject matter from the start.

Faced with disappointing growth after years of ultra-low interest rates, Federal Reserve Chair Janet Yellen and her peers who met this weekend in Jackson Hole, Wyoming, re-affirmed their belief in power of monetary policy to stop economies from slipping into deflation.

That is the proper description of the typical central banker mindset, all framed around “deflation” as derived from study of the Great Depression. It is a simple mantra; prevent deflation, create economy. Almost everything every central bank does flows from that singular purpose. And yet, here we are.

Since economics is almost entirely a discipline of math, it leaves behind some of the common sense views that would check unquestioned deference to correlations alone. Perhaps the most obvious of such differences was the housing bubble of the mid-2000’s. Again, by nothing other than common sense, following so close to the dot-com collapse, there was no need for any Ivy League training to sense that something was very wrong at that time. Most people didn’t explicitly act despite the nagging warning because it was assumed Alan Greenspan knew what he was doing; and further that when Alan Greenspan knew what he was doing such knowledge translated into the proper, utopian economic format.

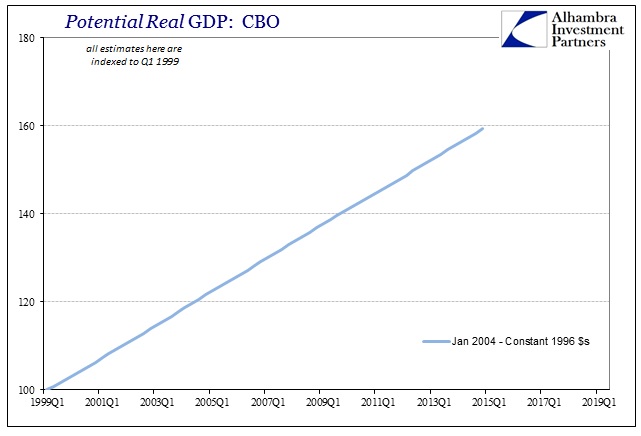

The economic studies of that time were unconvinced that anything at all might be amiss. The numbers and statistics just didn’t believe it was anything more than a temporary or “transitory” aberration that monetary policy in the “right” amount would eventually cure. The CBO estimates for “potential” real GDP in January 2004, for example, show absolutely nothing interesting about the economy of that period; and thus it was expected that nothing interesting would result.

What happens when all monetary policy, and indeed economic understanding in this “elite” sense, is based on such math? Economists and policymakers were operating then under assumptions that were broadly false; meaning in ways both big and small. In what is missing from the economic narrative of the post-2008 period is just how much the math has changed to become closer to oikonomia despite the fact that central banks are endowed with all the power they ever wanted.

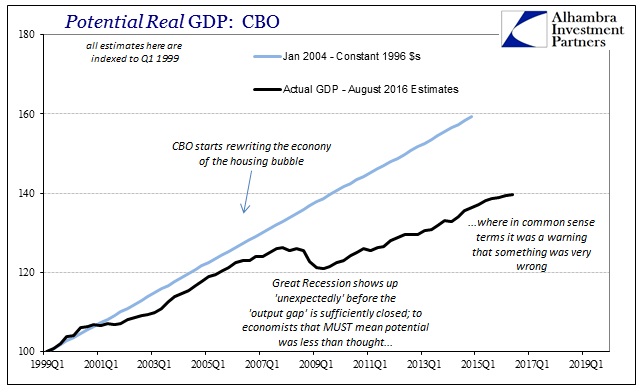

What you see immediately above are the consequences of the Great Recession appearing before the post-dot com recovery could be fulfilled as 2004 estimates of potential projected. In other words, the weak recovery after the 2001 recession was much more than economists thought, including Alan Greenspan and Ben Bernanke in both their tenures. But because they didn’t think this was even possible, and all the correlations and regressions they ran and used said so, they dismissed all the warnings of everything from monetary behavior to just plain asset bubbles (globally).

The consequences should not be understated because all monetary policy, including all the “rules” by which it is and is supposed to be judged, is being constructed and activated under all the wrong assumptions. Therefore, even assuming that central banks could actually achieve what they claim to be able to achieve, they never would have in the middle 2000’s because they were using all the wrong settings, from potential on down (meaning the all-important “output gap”).

That is an enormous problem that indicates fundamentally unsound principles guiding the conduct of central banking before, during, and after the Great Recession. What good is it to be handed enormous monetary power if you are unable to figure out much at all about the environment in which that power will be used? And if it takes a decade to finally write the script about what happened so many years ago, then such incapability is itself disqualifying.

Despite these glaring mistakes, this enormous gap in operation and theory, nothing was ever done about it. To this day, it continues without much discussion in and to the public about serious misconduct. A good part of the reason there hasn’t been any accounting of this deficiency is the idea of central bank power to begin with. Since monetary policy is believed most helpful when perceived nearly invincible, then monetary policymakers can never admit mistakes. It is a recipe not for success but self-reinforcing failure (not to mention the political bubble of Lord Acton’s axiom).

Beyond that, monetary policy has avoided this topic because it isn’t yet settled; the economy and all the math that is struggling to understand it from the socialized perspective is still being rewritten from the housing bubble forward to the present day.

A recession is a temporary deviation from trend or potential. If the potential of the economy is itself encumbered by whatever “unknown” factors, then any downturn associated with it cannot be a recession. What you see above is the math of orthodox economics that proves the Great Recession wasn’t one while simultaneously suggesting the dot-com recession might not have been either; in fact, it shows that this depression appears to have started long before 2008 if only gently to begin with. From that view, the Great Recession wasn’t a new cycle but an amplification of everything that financial imbalances and common sense warned about.

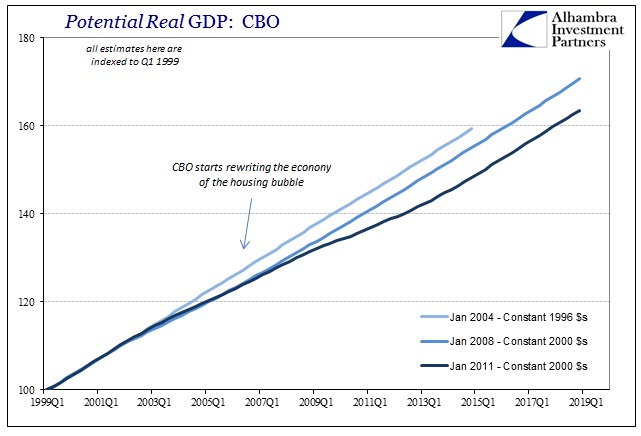

And we still have no idea just how far down this bottom might be. The CBO, as the Fed and any other orthodox institution, still hasn’t calculated where this will all end – because it hasn’t. In the August 2015 update to real GDP potential, the CBO actually upgraded ever so slightly its trajectory from the January 2015 set reflecting the ideas of “full employment” and final liftoff including, finally, inflation (the frame of reference for all of this in orthodox terms). Though it wasn’t anything like what potential was supposed to be especially as compared to the January 2004 math, it was at least thought an end to the almost constant downgrades to it.

Unlike the rhetoric still coming out of the Fed, however, potential in the most recent calculations was revised down yet again this year, and rather sharply especially for the coming years. In other words, Janet Yellen is still trying to conduct monetary policy where she has no idea what the output gap is or might be.

All these charts don’t really do justice to just how badly the economy has performed, and by extension central bankers. These gaps in “potential” from one estimate to the next are simply enormous; in many ways beyond comprehension. In reality, in oikonomia, there is only one gap that matters:

The Great Recession was not a recession as even these orthodox templates demonstrate. Further, the fact that the CBO had to rewrite the housing bubble period adds further evidence to the primary common sense economic suspicion about the whole of the 21st century. Economists have been quick to dismiss any complaints about the economy but now their own mathematical parameters show that those complaints had it right all along – as instead it has been economists who have been wrong the whole time.

If the people were too emotional and unsophisticated to know what was good for them, the primary “lesson” of the 1930’s, what should we conclude when it is shown in none other than orthodox math that the people have been right all along in the 21st century and it is economists who have depended far more upon emotion to maintain a system that works for nobody (except central bankers and economists)? Economists were correct that the “jobless recovery” phenomenon was wrong, but wrong in why they were correct. These cycles are increasingly “jobless” but they were never recoveries to begin with because they were never cycles.

In common sense terms, what the CBO figures show, without ambiguity, is that for nearly all of this millennium the US economy has been shrinking. This is supposed to be impossible, but because it has occurred only slowly (outside of late 2008/early 2009) it has given the mainstream of orthodox economics plausible deniability. The position of denial is, however, no longer so plausible as enough time has passed and enough updated math gathered. It is also relatively clear in the sense of timing; ever since Alan Greenspan was believed the maestro, more has gone wrong (and, again, to an incomprehensible degree) than even the smallest single thing right.

Despite the fact that it is all right here in the orthodox math, there is nary a word from any of them about it. Any truly scientific endeavor would be overflowing with articles, discussions, and mainstream debate about what went wrong because there is only evidence that it has all gone wrong. Nothing would be off limits to scrutiny because that is what is called for in assessing failure on this scale. Instead, the most we get from policymakers and economists are private conclaves discussing maybe how policy could have been a bit more effective. Thus, as I wrote last week:

There is a world waiting to be rebuilt and a growing realization from even the most recalcitrant orthodoxists, those stubborn elite who denied all this for decades, that such a job is going to get done. We are moving past “if” and toward “when.” They are not interested in litigating past liability, only ensuring that they have a voice in that outcome. That should never happen; they had their chance, squandered it, and proved themselves unfit for the huge task ahead that was left by nothing more than Baron Acton’s axiom about power corrupting. A republican democracy needs no such people in positions of influence. They couldn’t be trusted to do what was right, and now we are left still to tally the costs of such blatant immorality.

The CBO has performed a valuable service all still within the orthodox terms of mainstream economics. By providing us with the inarguable math of the morally unfit, there is no clearer evidence that they really don’t know what they are doing.

Stay In Touch