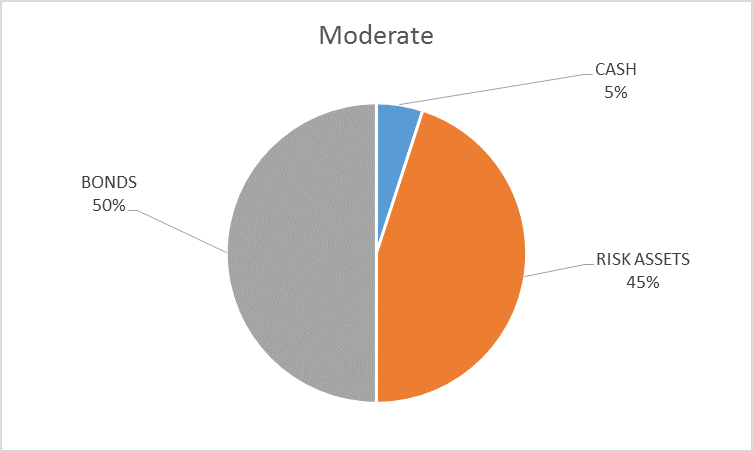

As with last month, I delayed this update a few days to see if we might gain some clarity that would warrant some change in our allocation. Alas, no such clarity has emerged and so, as it has been since August, the risk budget remains unchanged this month. Indeed, as last month, the entire portfolio is unchanged. For the moderate risk investor, the allocation between bonds, risk assets and cash remains at 50/45/5. While the yield curve did steepen ever so slightly, it was for the wrong reason and not enough to justify a change in any case. Credit spreads continued to narrow but narrowing spreads were already factored into our current allocation. Earnings have improved somewhat and we may even see a slight rise in S&P 500 earnings this quarter, but we are far from any valuation that would warrant buying US stocks. Momentum has shifted on shorter time frames around various asset classes but long term momentum measures haven’t changed.

It was tempting to move to a more conservative stance in advance of the election but there is no way to predict the outcome or the market reaction. Some of the economic data released over the last month could be construed as improving or maybe not getting worse is a better way to put it but the big picture hasn’t changed materially. The Chicago Fed National Activity Index (a very broad measure of economic activity) improved but is still below 0 and the 3 month moving average continues to worsen. GDP was better than expected but primarily due to items that won’t repeat – a surge in soybean exports and an inventory build in the face of already high inventories. Consumer Sentiment/Confidence eroded significantly on the month, probably a reflection of election anxieties. Frankly, the biggest news over the last month has been the change in inflation expectations but we anticipated that months ago and reduced the duration of our bond portfolio. In short, while there were some potentially significant changes if short term trends become long term ones, that hasn’t happened yet and so I won’t make any changes.

Indicator Review

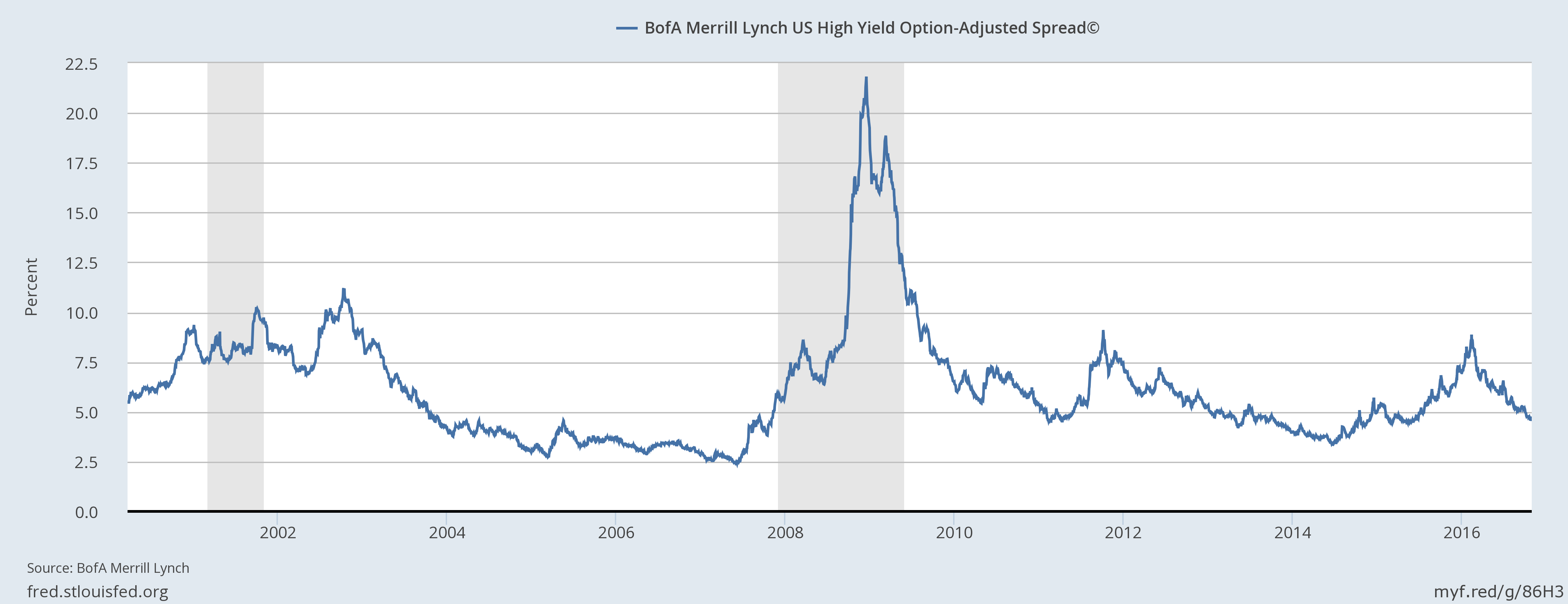

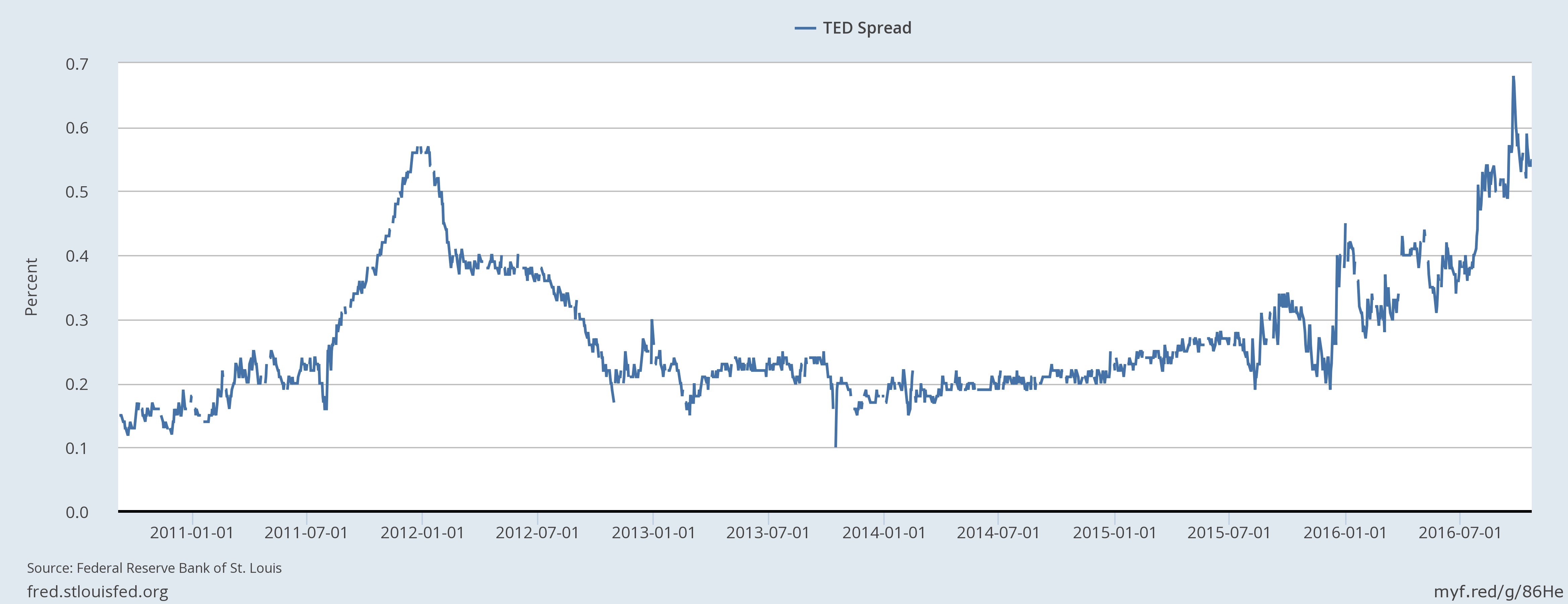

- Credit Spreads: High yield credit spreads narrowed by 42 basis points since the last update a pretty significant move. Spreads are still, though, above the lows for this cycle set back in 2014 and well above the lows of the last cycle. The narrowing has been driven by the rise in oil prices, relief that the fracking bust wasn’t bigger. With commodities now showing positive momentum, one wonders if the eventual widening of spreads into recession will come from some other quarter. Or will spreads just continue to narrow toward the lows of the last two cycles? Could be and that would likely provide some positive feedback to economic growth. Meanwhile, the TED spread continues to worry us, at its widest since 2011 and trending in the wrong direction.

- Valuations: Earnings season is well underway and operating earnings will probably rise year over year this quarter. How much of that is real and how much a function of CFO magic is hard to say. The rise though is likely to be in the low single digits – current estimates are for a 2.5% rise over last year – so valuations will not be impacted significantly. Meanwhile, international markets continue to offer cheaper valuations, with EM still cheap even after the recent run-up.

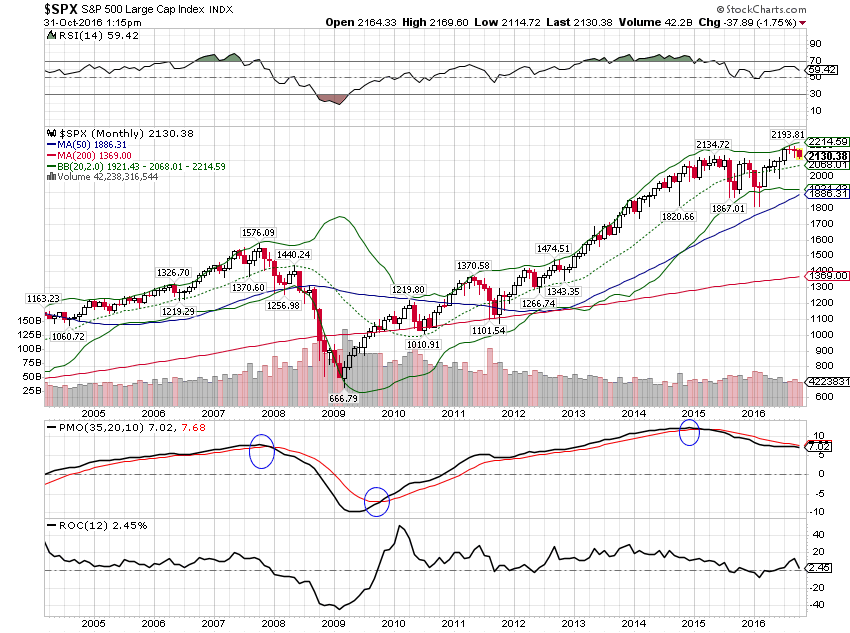

- Momentum: While short and intermediate term momentum is shifting – as it always does – for a variety of asset classes, long term momentum has not changed. For the S&P 500, all measures of momentum are negative, as they were last month, even though we have yet to see any significant sell-off.

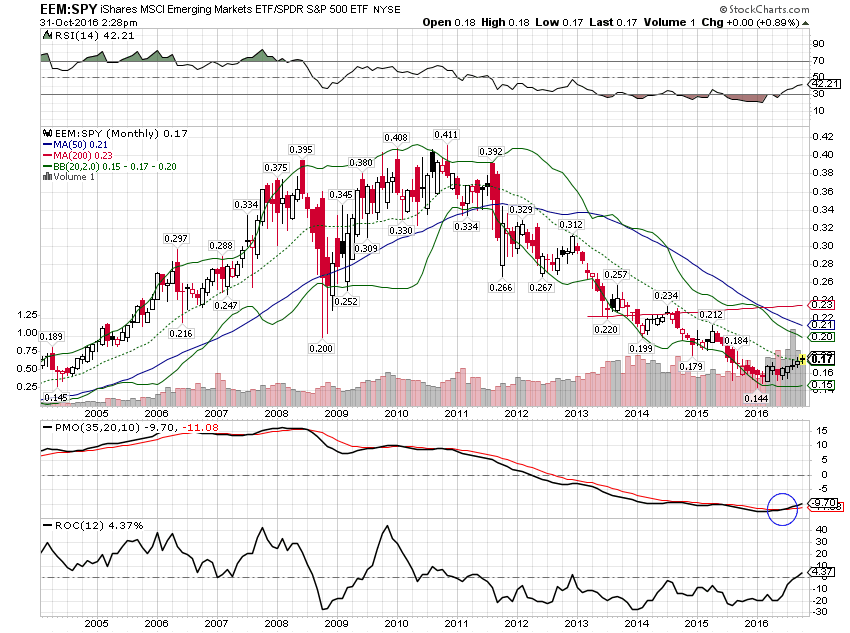

Long term momentum still favors EM equities over the S&P 500:

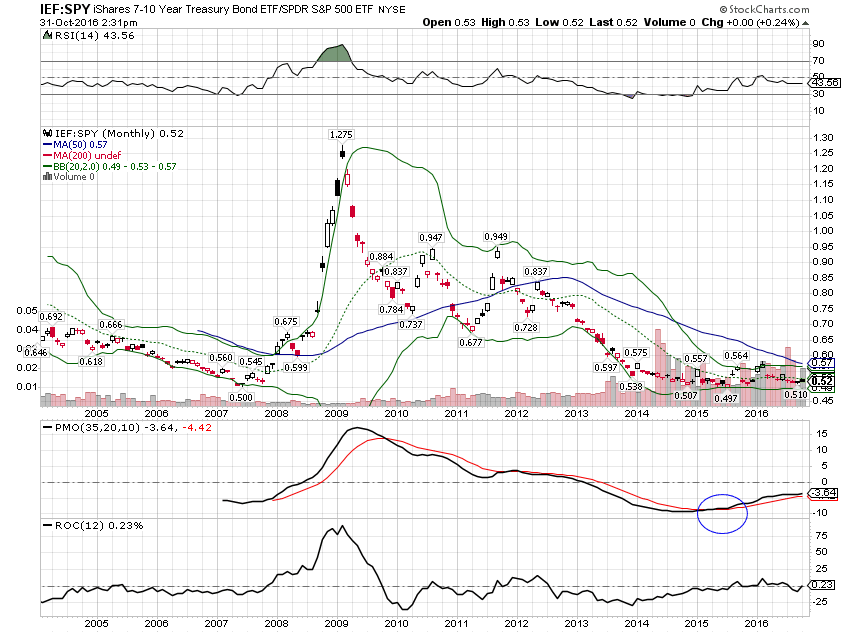

And Treasuries over S&P 500:

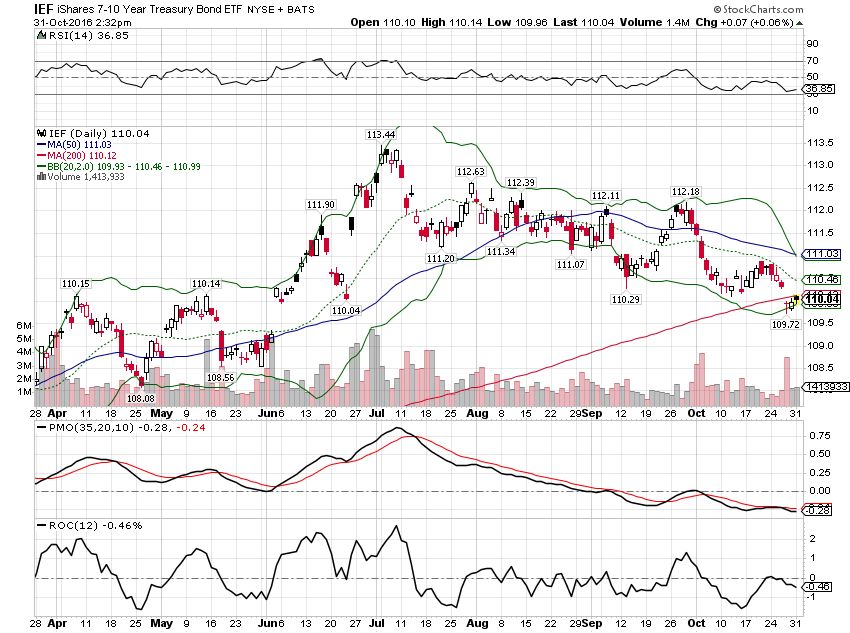

And yes, short term momentum has left the building for intermediate term Treasuries:

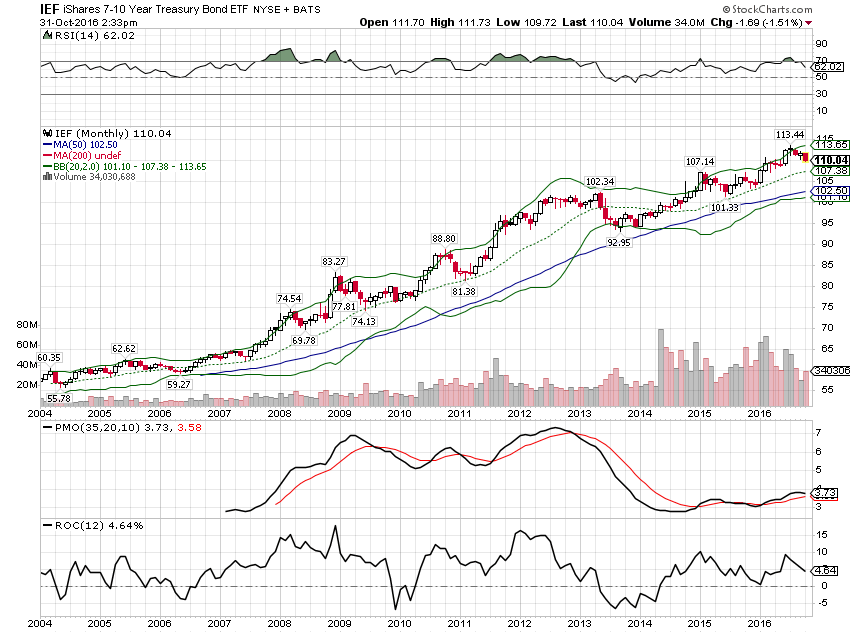

But it is only a blip in the long term bull market:

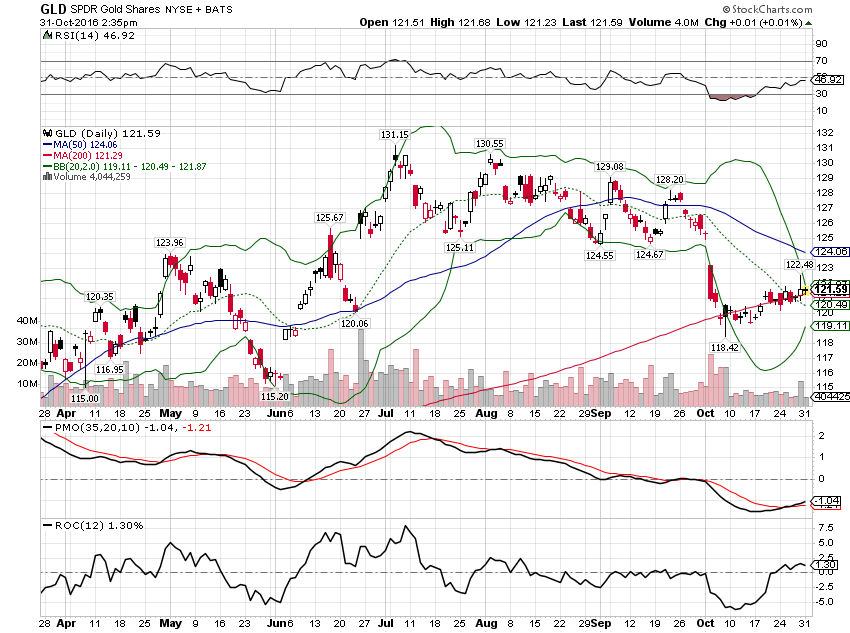

Gold has had a correction but short term momentum is trying to turn higher:

And, again, long term momentum is still positive:

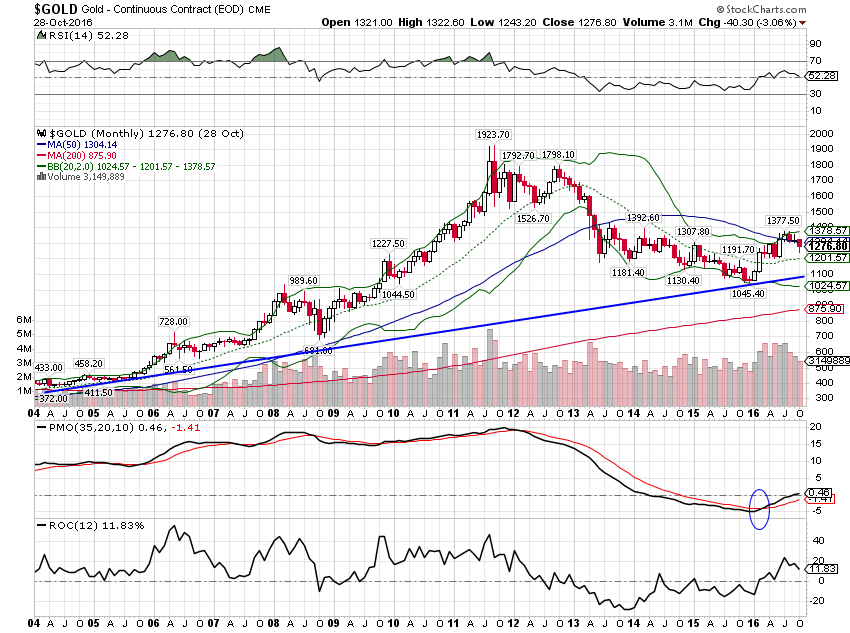

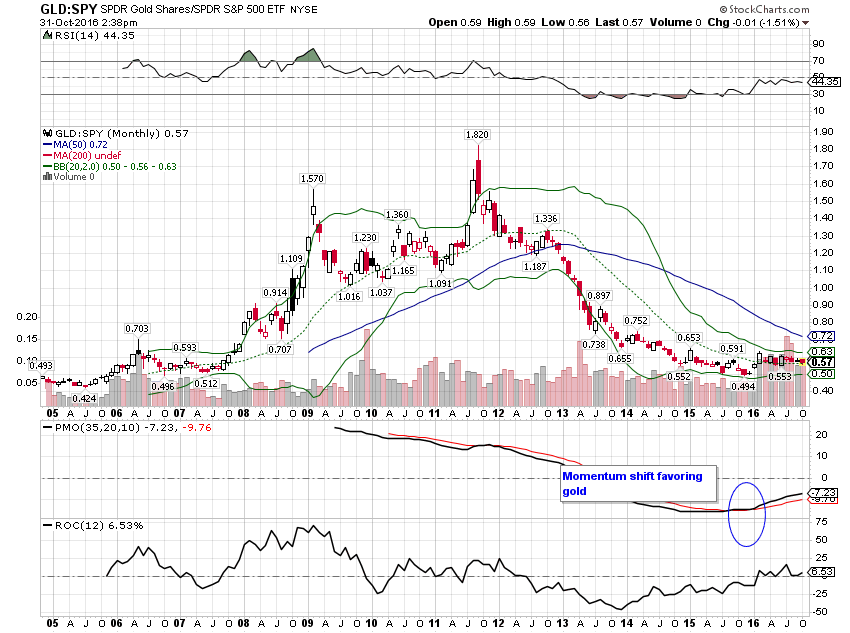

Long term momentum still favors gold over stocks as well:

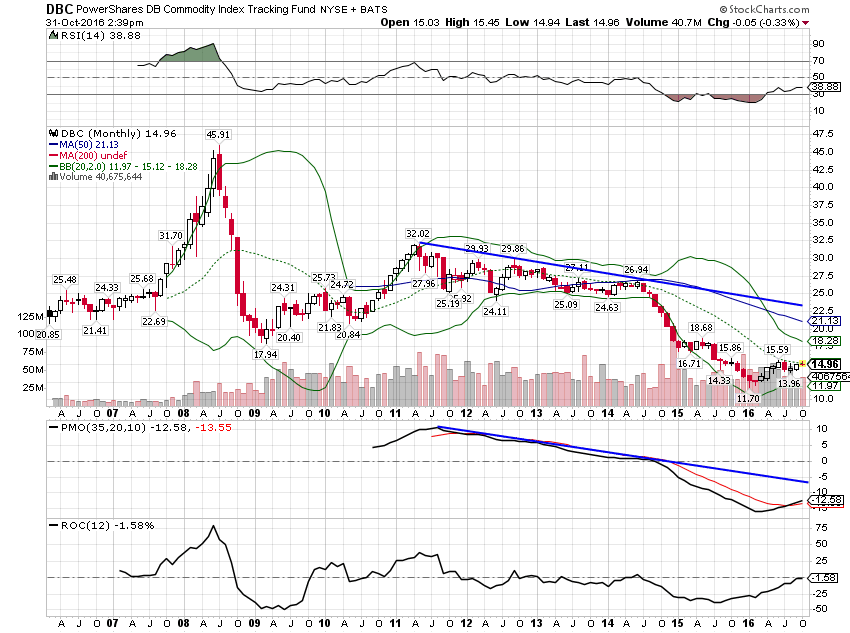

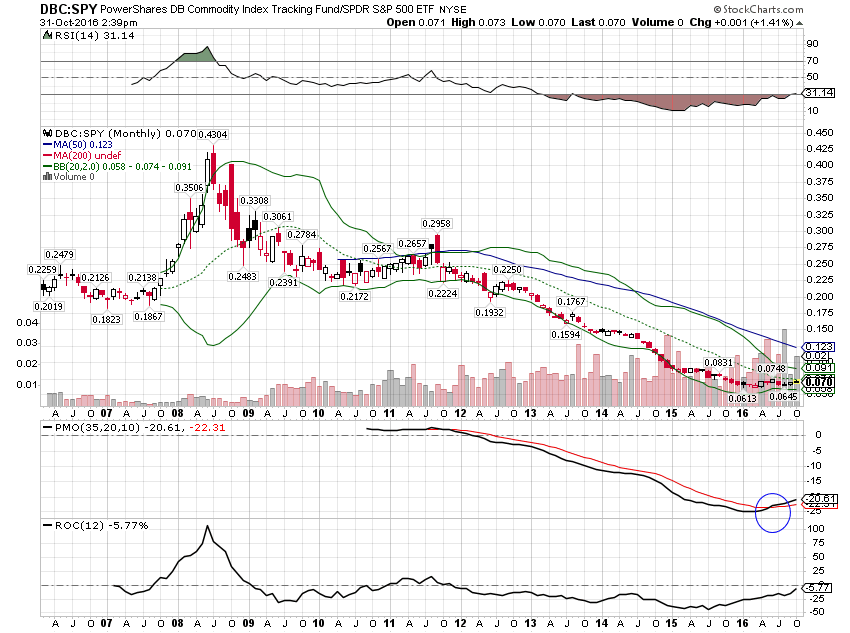

Commodities have corrected a little but momentum points to more gains:

And long term momentum has turned up versus stocks as well:

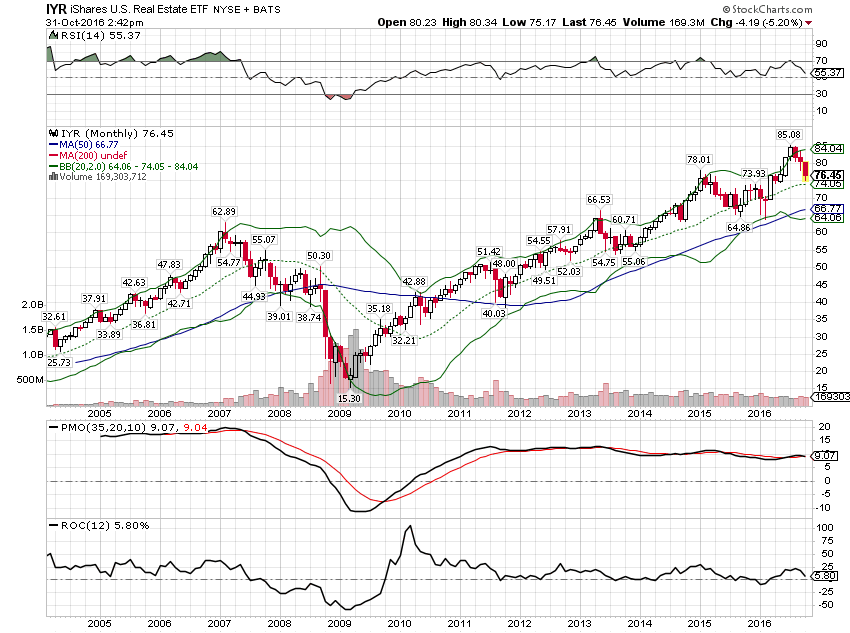

The back up in bond yields has hit REITs but the long term trend is still pretty clear:

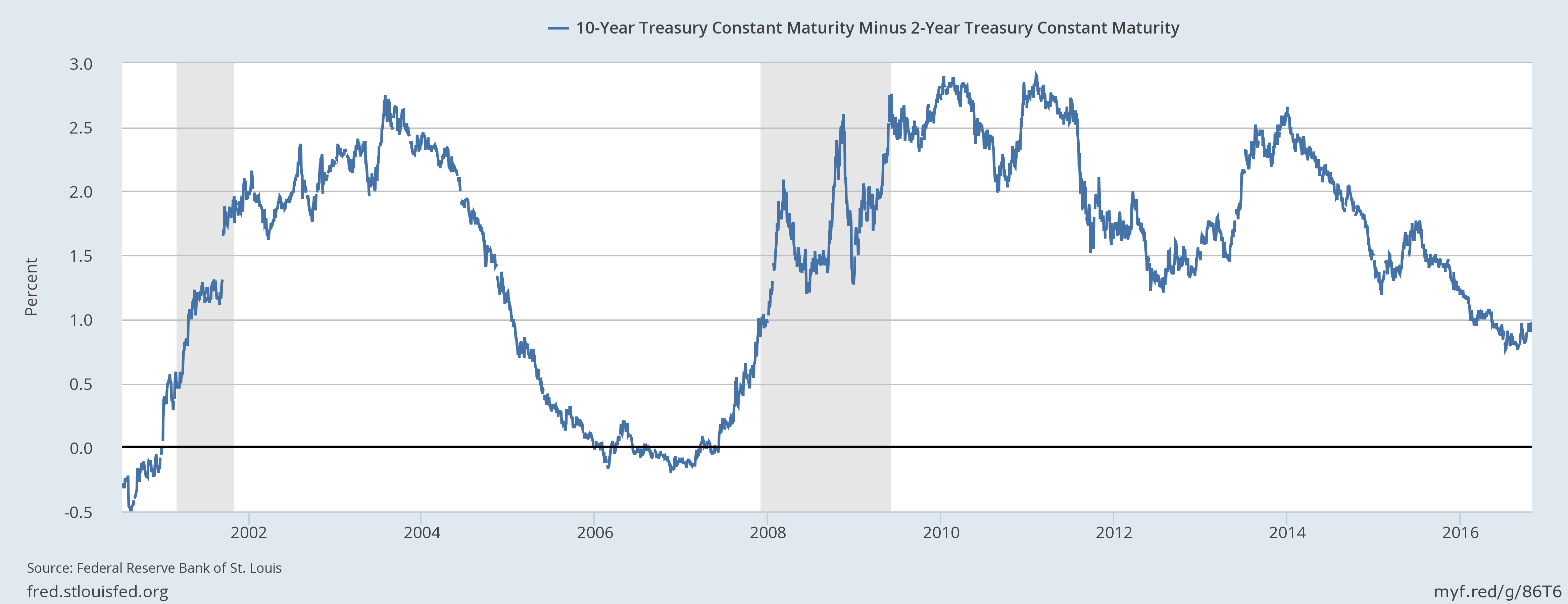

- Yield Curve: The most interesting moves over the last couple of months have been in the bond markets and yield curves. The 10/2 curve steepened by 15 basis points since the last update:

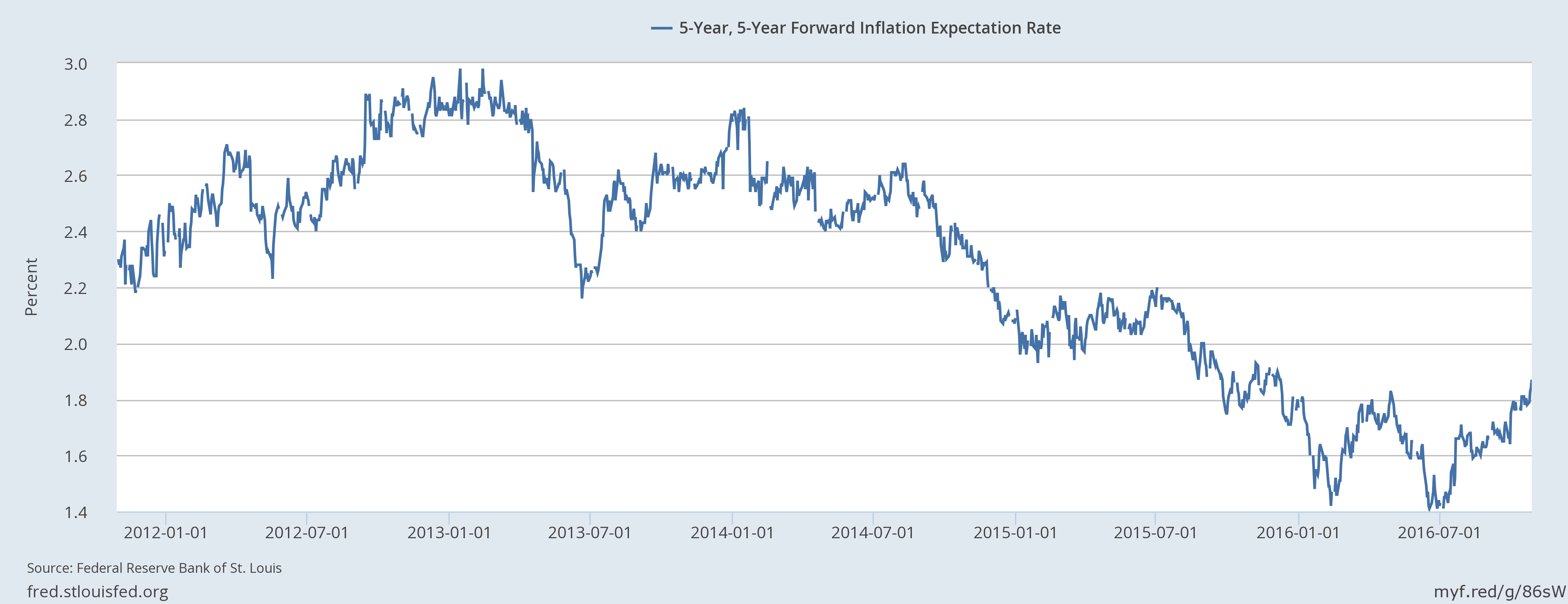

Normally we associate a steepening with improved growth expectations but in this case, it seems the rise in rates and the steepening of the yield curve is all about inflation expectations:

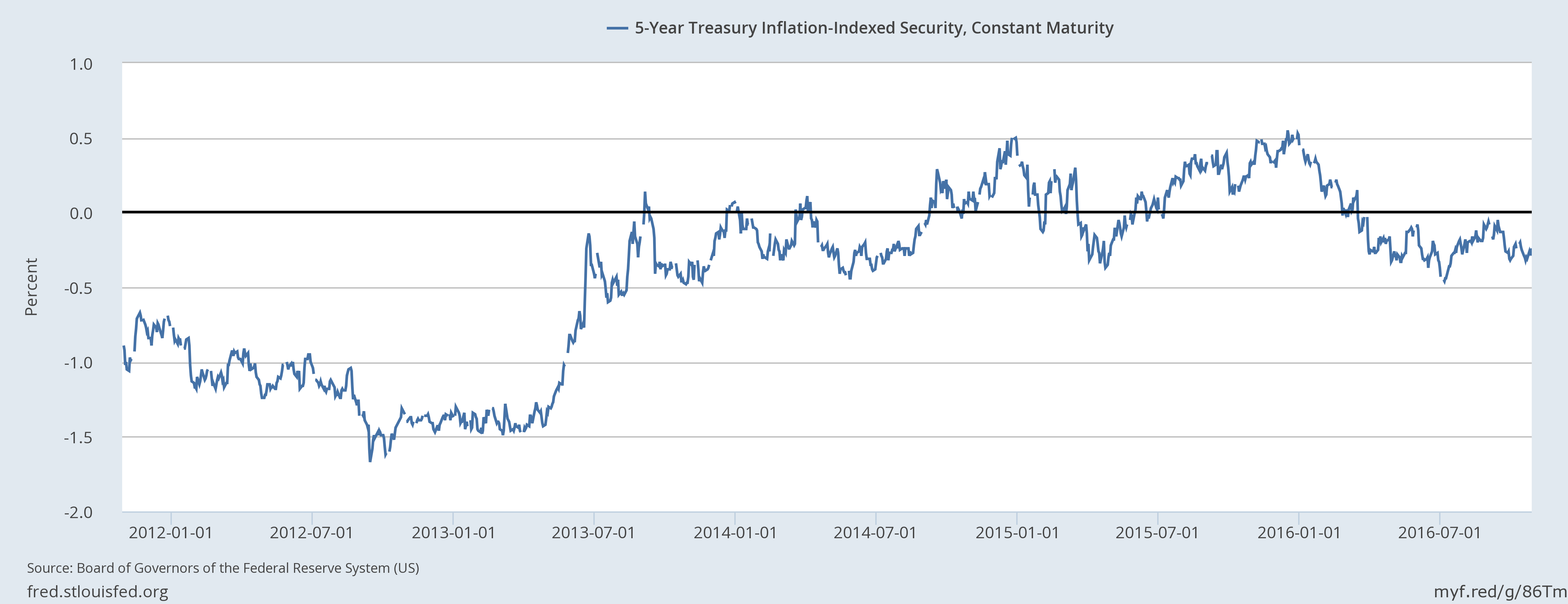

Real yields, an indication of real growth expectations, have barely budged and remain negative out to nearly 10 years:

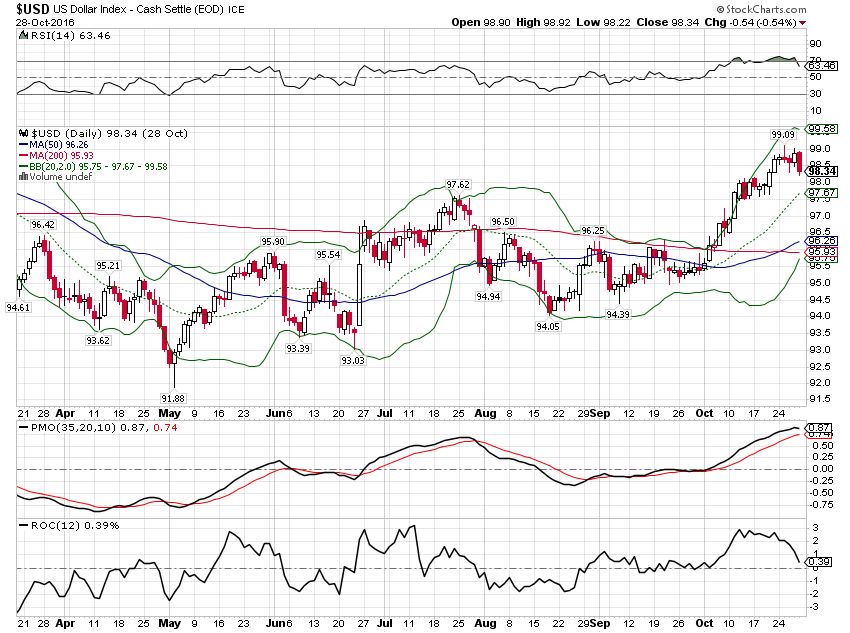

At least as interesting is that this rise in inflation expectations has come in the face of a recent rise in the dollar:

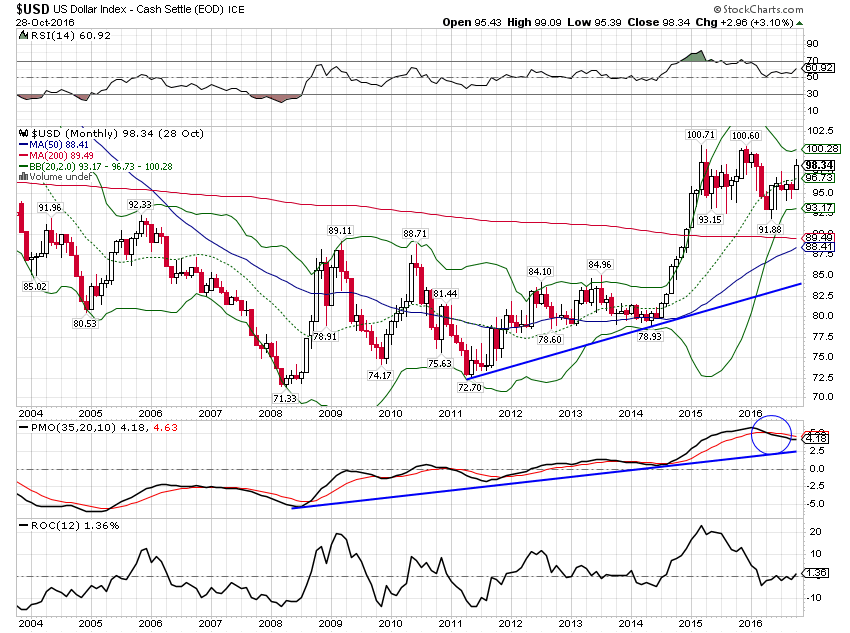

Long term momentum for the dollar is still pointing lower though:

Stay focused on the long term trend and momentum changes. It is easy to get sidetracked by short term changes that don’t mean much in the longer term context.

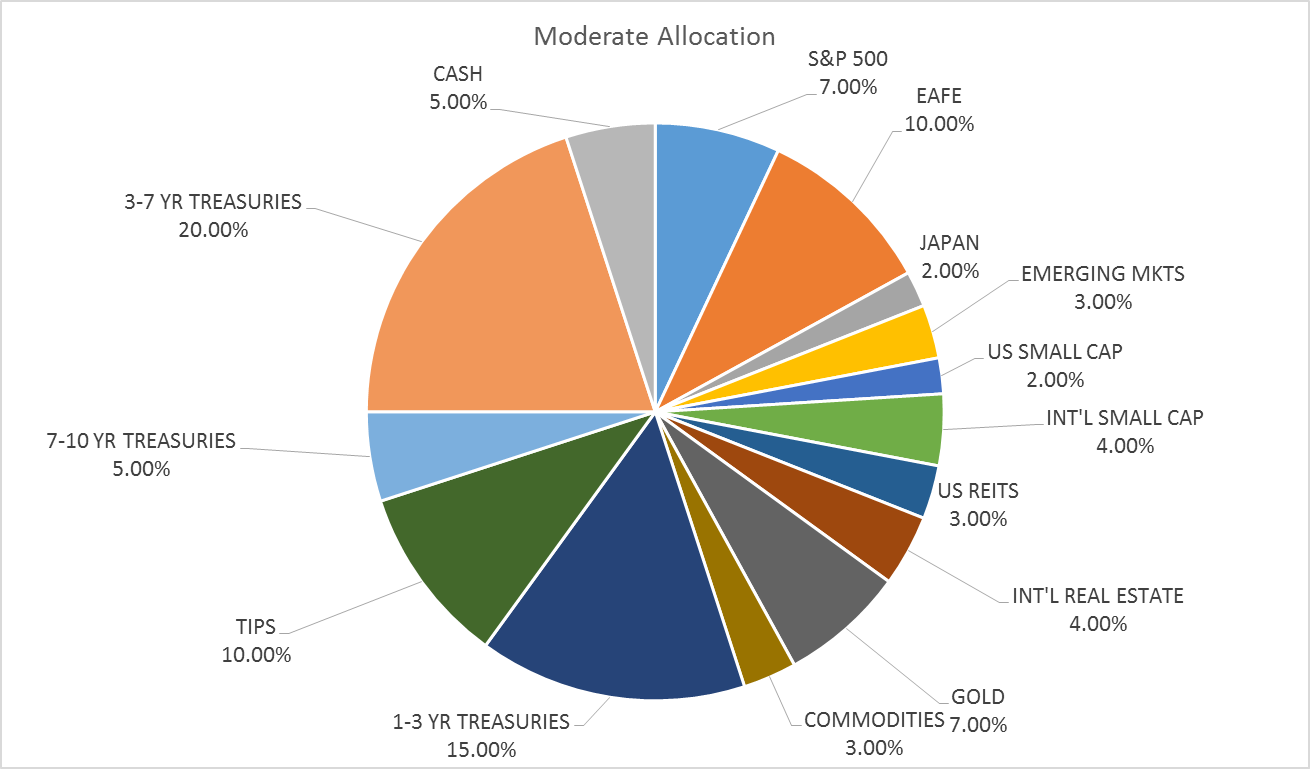

The Moderate Portfolio has not changed:

FOR INFORMATION ABOUT OTHER RISK BASED ASSET ALLOCATIONS OR ANY OF OUR OTHER TACTICAL MODELS, PLEASE CONTACT JOE CALHOUN AT JYC3@ALHAMBRAPARTNERS.COM OR 786-249-3773. YOU CAN ALSO BOOK AN APPOINTMENT USING OUR CONTACT FORM.

CLICK HERE TO SIGN UP FOR OUR FREE WEEKLY E-NEWSLETTER.

“Wealth preservation and accumulation through thoughtful investing.”

This material has been distributed for informational purposes only. It is the opinion of the author and should not be considered as investment advice or a recommendation of any particular security, strategy, or investment product. Investments involve risk and you can lose money. Past investing and economic performance is not indicative of future performance. Alhambra Investment Partners, LLC expressly disclaims all liability in respect to actions taken based on all of the information in this writing. If an investor does not understand the risks associated with certain securities, he/she should seek the advice of an independent adviser.

Stay In Touch