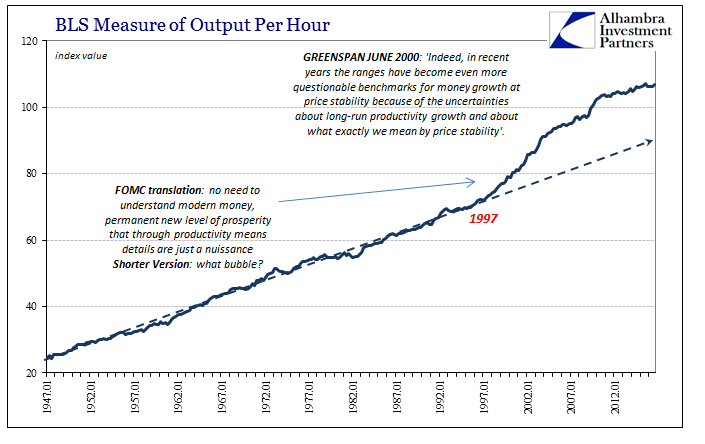

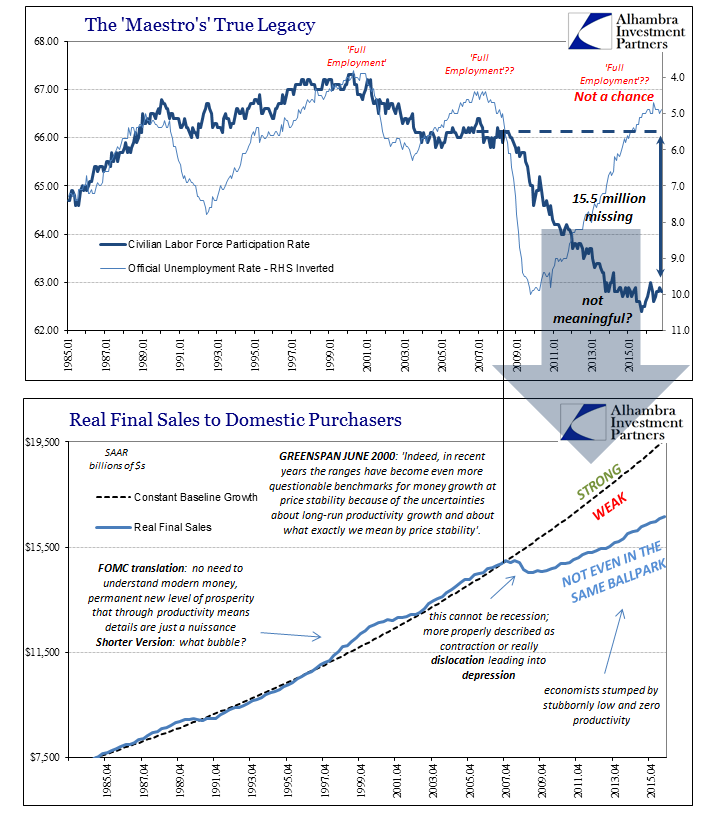

Throughout the 1990’s, calculated productivity in the US skyrocketed in what was taken then as a sign of monetary and economic genius, the “maestro” as it was. By the incomplete measures we have, that certainly seemed to be a plausible case. Starting in 1997, the BLS’s first measure for economic productivity, output per hour, surged. The consequence of that productivity jump was as real in monetary policy terms as it may have been for US businesses (and workers). As Alan Greenspan said in June 2000:

Indeed, in recent years the ranges have become even more questionable benchmarks for money growth at price stability because of the uncertainties about long-run productivity growth and about what exactly we mean by price stability.

An economy with a higher proclivity for innovation and such gain would be able to tolerate higher money growth without affecting inflation. The problem was really as Greenspan had said before in that very same discussion, namely that the Fed no longer knew what money growth was because they could no longer even define money. Their “solution” was to just accept that productivity was, in fact, a long-run, dependable change for the good and thus they wouldn’t need to fret about money growth especially when they could reliably target the federal funds rate to control it all (at what were deemed sufficient margins).

It was, obviously, a huge mistake because money does matter, the dot-com bubble perfectly illustrating why and why it would continue to. This is not to say that there wasn’t actual productivity progress in the 1990’s, as there clearly was. The arrival of the internet and the telecom revolution surely had large effects on the US and global economies, but they also radically altered banking which would have monetary consequences for a credit-based global currency system. The trouble was sorting the one from the other (after recognizing the money problem first, of course). Was the telecom revolution a permanent contribution to the economic baseline? Or was it more eurodollars than connecting computers?

The BLS data argues for the latter. If the internet contributed to the boost in productivity it didn’t continue to do so for long into the 2000’s; and if it was more so the eurodollar’s surge, then we know why the tendency for productivity in the 2010’s has been almost zero. In both cases, Greenspan was wrong but he and the rest of them (orthodox economists) wouldn’t even consider that they were wrong until more recently. As I have pointed out before, on the cusp of the Great “Recession” in May 2007 it was Janet Yellen arguing for the conventional opinion that productivity was only temporarily low in the 2000’s and that when it came back the Fed could count on a very much needed positive boost again:

But the hypothesis that the recent decline in productivity growth is mainly structural does not seem to me to square well with the broad range of available evidence. Recall that in the 1990s there was a whole constellation of evidence—including a booming stock market, robust consumption, and rapid business investment—that was consistent with a hypothesis of a lasting increase in the rate of productivity growth. In contrast, over the past year or so, business investment in equipment has been very sluggish and more so than seems warranted by the deceleration in business output.

But while measured productivity was low in the last decade, despite Yellen’s “whole constellation of evidence” that the 1990’s were the real deal it has only been worse on this side of the eurodollar bust.

In fact, the numbers are so skewed that it highly suggests something wrong with them. Most people react viscerally when you question the veracity of widely-accepted statistics; they were, after all, put together by the best and brightest and kept a safe distance from anything that would introduce bias. And that is mostly true, but only up to a certain point. In the case of productivity, the point at which the questions start to really bite is much lower than for other figures. The reason for that is simple; it isn’t an actual estimate, but a plugline difference between two separate measures.

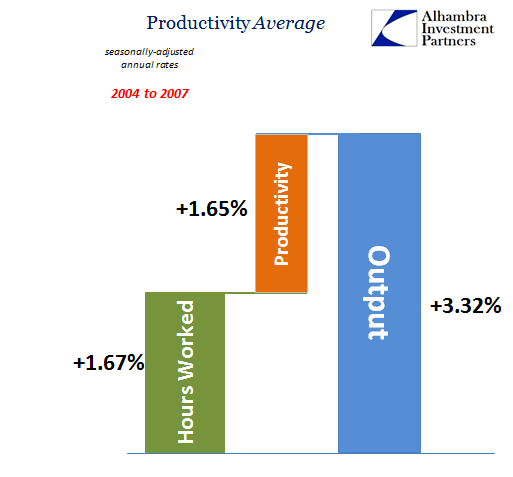

The BEA tallies output, really private output, a majority subset of GDP, while the BLS estimates total hours worked. The difference between them is output per hour, voila, productivity. This is what these variables looked like in the “low productivity” growth period of the housing bubble:

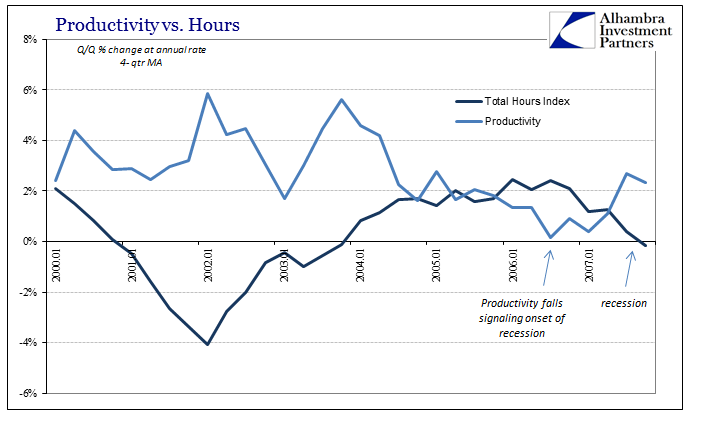

The level of output was slightly less than historical experience, as was total hours worked (“jobless recovery” and all), leaving the middle of productivity only marginally less than the 1990’s as a whole. Average productivity from 1993 through 2000 was just about 2%, with total average output a more conforming 4.38%. From 1997 through 2000, productivity averaged a blistering 3%, that which to Greenpan’s Fed encouraged only great recklessness in the form of continuing monetary ignorance. Regardless of the specific levels, what you see above is what you would expect to see; economic growth that is derived from a decent mix of both increased labor utilization as well as the greater efficiency of that labor.

The economy of the past few years is totally unlike that, especially under the “rising dollar” where the BLS continues to suggest robust labor gains that translated into highly positive monthly payroll changes. As a result, because GDP has tailed off, productivity is pushed to very low levels and often negative. As shown above, you don’t find a robust hiring environment where productivity is so low and negative; in fact, you typically find the very opposite, recession.

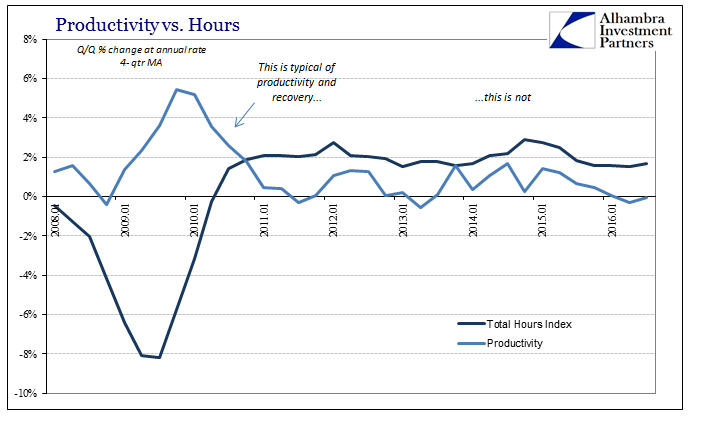

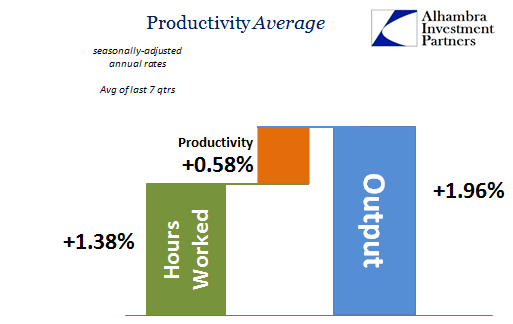

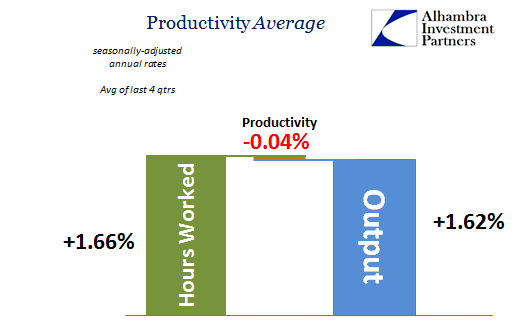

Over the past seven quarters, those that fully encompass the arrival of “full employment”, output has been unusually low, less than 2%, while total hours have grown at a rate actually less than the middle 2000’s (best jobs market in decades?). That leaves productivity at just 0.58%. In just the past four quarters, including the latest quarter, Q3, productivity is slightly negative.

The reason for that is again the BLS; output is lower in the past four quarters than in those four plus the prior three (clear deceleration). But the BLS estimates that more work has been done at a faster rate in the last four than the last seven. Lower output but higher hours can only mean negative productivity by the nature of its ad hoc construction. That doesn’t necessarily meant that productivity in the real sense is negative, only that the number developed as the proxy for it is.

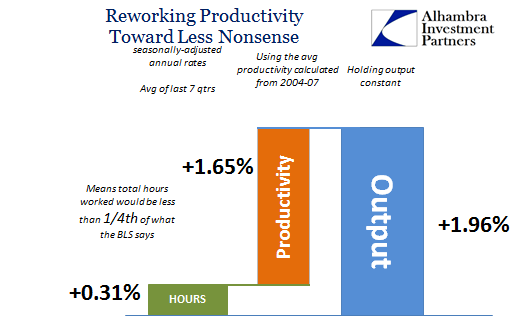

This discrepancy can work both ways; if we assume that productivity was still low, as low as it was in the middle 2000’s, but more like then, the labor growth almost disappears.

The BLS says the labor market seems healthy if still significantly slower than 2014, while the BEA estimates suggest that can’t really be the case. The overall economic statistics especially those for consumer income and spending would seem to agree with the BEA.

In the end, it may not matter much beyond perception, though in this world that matters a great deal. Getting people very excited about the economic prospects of “full employment” and the “best jobs market in decades” was a huge mistake, one that economists and Fed officials already regret. They did much to discredit them (and themselves) by overhyping what are flawed figures in the first place, but those that have also produced irreconcilable divergences.

All of that starts with the fact that there hasn’t been any real growth, in economy as well as labor, since the Great “Recession” started because it never was a recession to begin with. It is and has been in many ways the shadow echo of the eurodollar boom of the 1990’s; as the economy was so boosted then by shadow money, it has been “robbed” of similar mechanics since August 2007. It isn’t just economists who still view the world as if it could be 1997 all over again; these statistics were made for that world, meaning it isn’t surprising they lead to these contradictions because, like the unemployment rate, they were meant for very different circumstances. Whether it is productivity or labor growth that is off, they both end up meaning largely the same thing – there was no recession in 2008.

This economic growth just ain’t big enough for the two of them.

Stay In Touch