Like it or not, this is where we have been all along and a great many people are just now catching up. No matter what Janet Yellen says about the economy, she is talking out the side of her mouth. Internally, the recovery is gone, and it is never coming back. Externally, we have sub-5% unemployment so we all should be so happy, especially with, in her view, stable prices.

To their credit, many prominent economists aren’t so enthusiastic about those prospects. Among them are Larry Summers, Paul Krugman, and Brad DeLong, all who recognize that “something” just isn’t right and therefore “something” else should be done about it. Thus, the real economic debate over the coming years (unfortunately) will take shape around those two facets. Having wasted nearly a decade on purely central bank solutions that were never going to work, the real discoveries can now possibly take place.

The problem is as I wrote yesterday, where in a rush to do anything and everything “different” the Trump administration might actually spoil the process. De-regulation and income tax cuts, as well as the repeal of Obamacare, are all very good things that sorely need to be addressed; but they didn’t cause this depression and thus won’t get us out of it. And you can bet that none of Summers, Krugman, or DeLong will be in favor of those options, so if they all fail to restore economic growth, as I believe they will if left in isolation, then that will severely diminish those ideas for perhaps a generation or more. That would be a fatal mistake, especially since for the first time in many generations people outside of Economics are receptive to “new” ideas (that are only new because they have been out of practice and actively discouraged for so long).

Krugman actually described our predicament very well all the way back in 1999. Observing the Japanese fall into these very same conditions (it’s always the Japanese first because their lost decade then has become our lost decade now), he wrote at MIT:

Now you could argue that the experience of the Depression and after provides just such evidence. Many economists thought that with the end of World War II spending the United States would revert to Depression-type conditions; a whole school of thought, the “secular stagnation” hypothesis, was built around that idea. In fact, once jolted out of depression, the U.S. did not fall back.

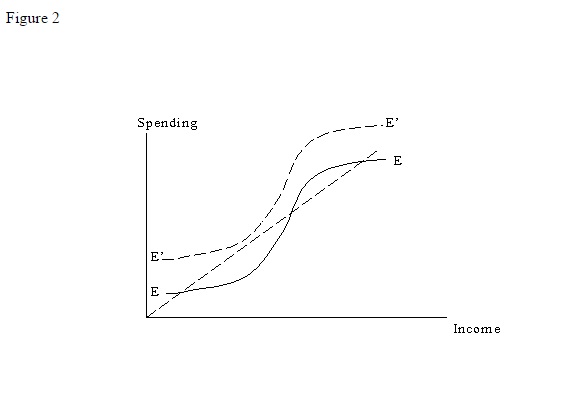

This has led many economists to believe that World War II was the answer to “secular stagnation” the first. In orthodox parlance, Krugman describes it as an S-curve with multiple equilibria, being careful to pronounce such analysis as dangerous because such a model would be, “a device that can justify practically any policy.” Even still, that is exactly how not just the US economy but the world economy acted in the 1940’s.

Thus, the secret would be to identify the event or cause by which the global economy was jolted and to use it as a matter of policy today. For Krugman, he of fake alien invasion fantasies, it was the government spending over WWII that did the trick. Therefore, governments in the 2010’s should be doing something similar in terms of size and depth, as well as sustaining those efforts for as long as it takes. This is why he embraced the idea of the ARRA as well as Abenomics, as both in their respective times seemed to be of sufficient size and duration so as to perform this “shock” into the higher order equilibria.

Not so fast, claimed Larry Summers. Writing in November 2015 when secular stagnation really started to catch on as QE-love faded fast, Summers points to the major flaw:

Paul studies an economy in liquidity trap that will, by deus ex machina, be lifted out at some point in the future. He makes the point that if you assume sufficiently inflationary policy after this point, you can drive ex ante real rates down enough to stimulate the economy even before the deus ex machina moment.

This is true and an important insight. But it seems to elide the main issue. Where is the deus ex machina? Where is the can opener? The essence of the secular stagnation and hysteresis ideas that I have been pushing is that there is no assurance that capitalist economies, when plunged into downturn, will over any interval revert to what had been normal. Understanding this phenomenon and responding to it seems the central challenge for macroeconomics in this era.

And so one of the primary routes of investigation over the past year or so has to been to further identify that deus ex machina without seeing it as such; “government spending” is far too general to be a useful guide. Some have proposed that the central bank should instead target a higher inflation rate, even 4% rather than 2%, but as much as that might satisfy some orthodox requirements economists are still left with “how would that work?” especially as central banking is on the wane for good reason.

The common theme for all these, and others that I have left out, is for some official agency, be it government or central bank, to be highly and hugely disruptive. All these “solutions” now finally and properly looking at the problem (depression) are based around the “shock.” The WWII thesis was of similar construction and belief, that disruption can be a positive force if only because of an existing negative mindset.

That, however, is not how this works. It is such a dark take on a capitalist economy, that once one falls down economists so often believe it will never get back up again without their assistance. And in the case of falling down, it never seems to occur that the cause of that fall was already some other disruption, so that further disruption might not actually be a good idea. Instead, greater disturbance might itself be the very cause of the dark mindset that economists attribute now to this supposed dark side of capitalism; or, as Krugman’s 1999 book was titled, in part, Depression Economics.

They are using a twisted sense of humanity and commercial liberty to justify why an economy needs to be further disturbed even if there is or can be no general agreement as to what or why that is. Summers was absolutely correct, as what they are all searching for is a deus ex machina, a derisive term from literature that smacks an author for lack of originality or insight. Thus is the state of Economics.

From a more positive view of capitalism, actual capitalism practiced without the heavy influence of especially central banks seeking to control prices and now markets, disruption is always a negative imposition. The primary goal of any policy is to seek out and assure stability. There were no redeeming qualities about WWII (the war itself, not our victory in it) let alone any that might be economic in nature. You can’t get ahead by destroying so much, no matter how shocking the process or the depression before it.

Instead, it would be more consistent that the global economy was positively “shocked” not by the spending actions to take out global conflagration but the re-imposition at long last of (more) honest monetary conditions. Bretton Woods took place in 1944, but will always be ignored by economists like Krugman and Summers because honest money is anathema to Economists who wish to be able to disrupt at their whim. Equating and soundly defining global monetary terms, for however brief (just 16 years), is a legitimate candidate for explaining in Krugman’s S-curve how the global economy skipped from the hugely costly equilibrium in depression to the utterly positive robust growth equilibrium that brought us, in good part, the Baby Boomers.

Is it really a mystery as to why an economy that is repeatedly intruded upon with some of the worst negative factors just won’t grow? Why any rational human would believe that a positive and sustained growth period could be created by “shocking” levels of negativity is itself a legitimate question. If you despise sound money because it would deny your place in the political order, WWII, in twisted fashion, looks really good as an alternate explanation.

Because of that, economists and Economists alike will never be able to find a “shock” big enough with which to push the US economy to that second equilibrim; they proceed under false assumptions and now others are doing it again (Trump “stimulus”). The greatest of these is beyond stable money to what constitutes money itself. As I wrote on the topic of secular stagnation in June last year:

Contrary to the core assertion of this view of secular stagnation, there was indeed another innovative revolution that altered the entire world trajectory; only it was far more nefarious and misunderstood by economists, in particular, who had decided, while this revolution was occurring, they had learned everything worth knowing. One of the few great ironies of secular stagnation that is somehow comforting if still also infuriating is that the eurodollar standard, the world’s true reserve currency this last half century or so, will likely end before anyone even knows it was there. That includes all the world’s monetary experts.

More harmful than all the world’s monetary policy disruptions (more so on expectations than in actual money), all of increasing sizes and doses, has been the far larger and more relevant “dollar” impositions. Stop the “dollar” and there will no longer be any need for intentional disruptions of further negative factors (either more inflation or the utter waste of government spending). Business can go back to the business of business, as it is supposed to be, rather than being concerned about the “rising dollar”, the falling dollar, or whatever else some economist might think up to fill in as a deus ex machina in the absence of monetary competence.

Stay In Touch